The 70th anniversary of the People’s Republic of China is a useful time to reflect on the development lessons of its remarkable rise from a poor country to an upper-middle-income economy. Success has eluded many other countries, including many who just a few decades ago seemed better positioned to do what China has done. This has led to a vigorous debate on whether there is a specific Chinese model, distinct from the development orthodoxy. For a sample and summaries of the discussions, see this book, this article, and this commentary. In fact, as I outline in this blog, China fits the development orthodoxy rather well. In doing so, I am taking up a train of thought that I first developed as a graduate student more than 25 years ago in a project comparing China’s reform experiences with those of Eastern Europe.

To make this point, I focus on four big development theories. This is not an exhaustive list, but it is representative of the most important ideas on the dynamics of economic growth.

Harrod-Domar, Solow-Swan, Lewis, and Lucas-Romer Models

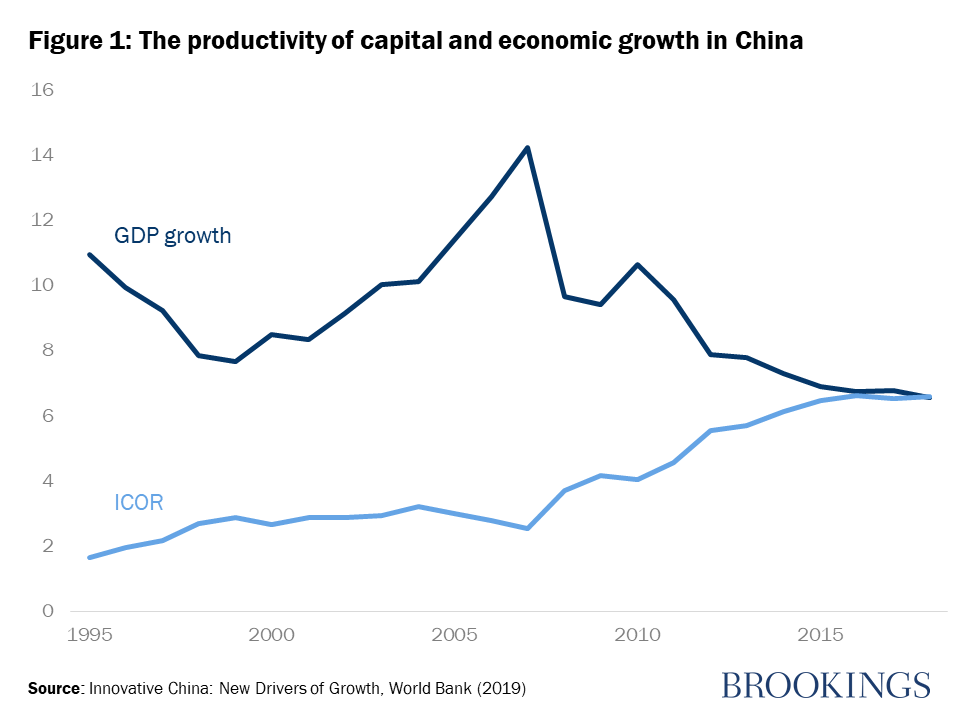

The first, from Roy F. Harrod and Evsey Domar, posits that a country’s growth rate depends on the productivity of capital and the rate of investment, which in turn is largely determined by the domestic savings rate. During the early stages of development, the productivity of capital is expected to be high because there are huge unfulfilled investment needs, and the limiting factor is thus the availability of savings to finance investment. China’s development bears this out spectacularly. High domestic savings and high productivity of capital both contributed to China’s rapid growth after 1978. Recently, however, the productivity of capital has begun to decline and with it China’s growth rate (Figure 1). Investment-led growth alone is no longer an option.

The second theory is the growth model by Robert Solow and Trevor Swan, which introduces labor (or in its augmented form, human capital) as an input into the aggregate production process. Investments in human capital have been shown to account for around two-thirds of the differences in per capita incomes across countries. Again, China fits this model rather well. Its human capital stock at the start of the reform process in 1978 was already high, which helped China’s take off when the major distortions of the Mao era were removed. The World Bank’s first study on the Chinese economy published in 1983 noted: “Despite slow growth of the average level of consumption, China’s most remarkable achievement has been to make low-income groups far better off in terms of basic needs than their counterparts in most other poor countries.”

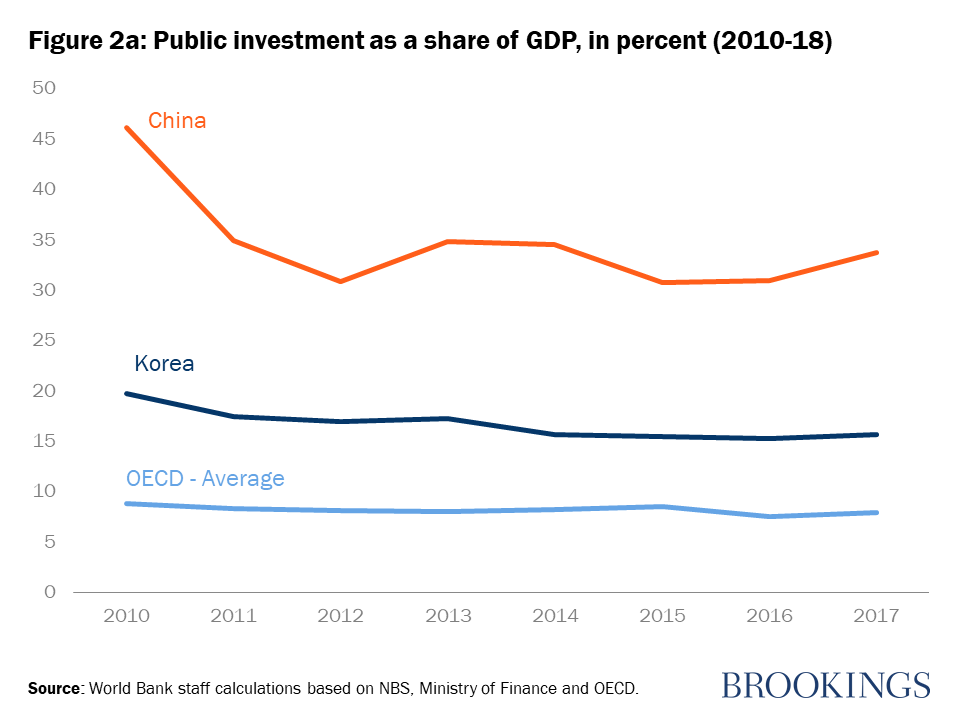

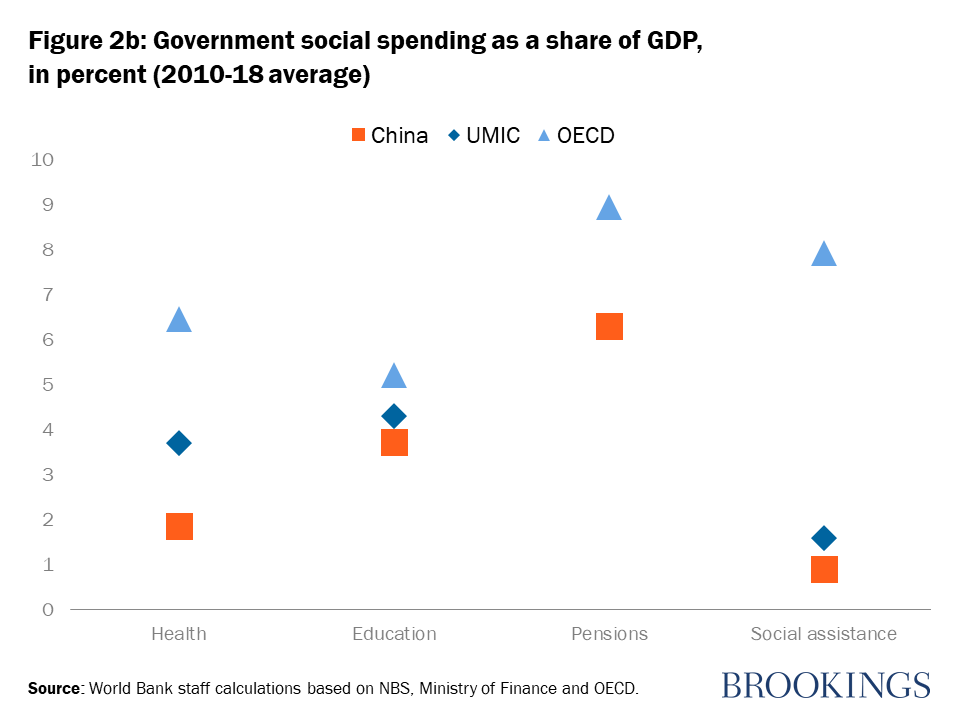

During the last decade, China has doubled down on a public-investment-led growth strategy, while investments in human capital have lagged particularly in the non-coastal and rural areas (Figure 2). The result has been declining returns to physical investment, just as the Solow model would have predicted. Besides, China’s labor force, which grew much faster than the total population until around 2010, has since stabilized and is expected to begin to decline in the next decade. To sustain growth, China might soon need to shift public spending from physical investment to human capital.

The third theory is the model of growth proposed by Sir Arthur Lewis. Growth is driven by the reallocation of labor from low-productivity agriculture to high-productivity industry. China’s experience provides ample evidence in support of Lewis’ theory. When it began its heralded reform efforts in 1978, three-quarters of the labor force were in rural areas. This has now fallen to below 40 percent and surplus labor in agriculture may disappear completely by the middle of the 2020s. This is perhaps the main difference between China and Eastern Europe at the start of the reform process and one of the key reasons for the different output trajectories during transition. As in the rest of East Asia, China’s industrialization was export-oriented, using international trade to access technology and other inputs and global competition as the yardstick for domestic entrepreneurship. As the scope for further labor reallocation has declined, China’s growth rate has moderated, just as it had in other fast-growing East Asian economies.

The final theory examined here is that of endogenous growth, originating in work during the 1980s by Robert Lucas and Paul Romer. This is not a single theory but rather a whole literature focusing on the determinants of technical progress or total factor productivity, which becomes increasingly important as economies mature. Among the factors identified as determinants of innovation and technical progress are structural ones such as the benefits of agglomeration in large urban centers, and institutional factors, such as the role of competition in driving innovation. China fits these models well too. The rapid development of its coastal cities spawned ideas and entrepreneurship. Competition in the global marketplace stimulated domestic upgrading while competition between provinces and rapid growth of domestic private businesses added to competitive pressures at home.

Yet China now seems to have cast the findings of endogenous growth theory aside. The investment drive to develop inland and secondary cities has often shunned agglomeration economies, which have only recently been rediscovered with the concept of city clusters. The role of competition as a driver of innovation has been replaced with state-led innovation drives. While China has some world-class companies when it comes to innovation, technological diffusion is more limited and total factor productivity has fallen by more than half during the last decade.

Familiar trajectory, special institutions

China’s success and recent growth moderation thus provide ample evidence in support of traditional development theories. This argument is not to deny the importance of policy or of China’s specific institutional innovations. A simple comparison of China’s record before and after the reform and opening-up 40 years ago clearly illustrates this point. China’s policymakers found ways to deal both with market and government imperfections that might have weakened the natural forces of development. Examples include the dual-track pricing system first tested in agriculture or the hybrid ownership model of the township and village enterprises which effectively dealt with risks to private investment in the absence of secure property rights.

Despite these institutional specifics, China’s growth trajectory is quite similar to the East Asian “Tiger” economies. As an upper-middle-income country (UMIC), China is now facing many of the same challenges confronted by these economies earlier in their history, such as declining productivity growth as the forces of structural change run out of steam, and a rapidly aging labor force. These developments have been fuelling fears of a middle-income trap. Moreover, some of China’s specific institutional solutions—such as the substantially larger role played by state-owned enterprises, particularly in finance and services, or the highly decentralized and competitive system of inter-governmental relations—may hinder growth more than help going forward.

While there is much to learn from China, there is also a lot that China can learn from previous transitions to high income and what has made them so difficult. We will take up this issue in a companion blog, based on the findings of a recent World Bank report that analyzes China’s likely future drivers of growth.

Related Content

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

China’s rise fits every development model

October 17, 2019