The choice of ExxonMobil’s Chief Executive Officer Rex Tillerson as United States secretary of state took some people by surprise because of his lack of diplomatic experience. But the choice is far less surprising to those familiar with today’s giant energy multinational corporations. ExxonMobil, like other big oil companies, is a company with operations around the world, including in locations rocked by political violence. Executives of such companies do not shun tough locations. They acquire experience managing extraordinary levels of political risk and sometimes overseeing operations in war-torn countries. But are big oil companies less sensitive to political risk and conflict than other firms? And if so, why?

In a recent paper, we look at the sensitivity of different types of multinational firms to different types of political violence, including civil wars, terrorism, state terror, and assassinations. Our analysis, based on a dynamic fixed-effects model for a panel of 90 developing countries from 2003 to 2012, shows that multinationals in the natural resource sectors are more resilient to political conflict than those operating in the non-resource sectors. These results are in line with a paper looking at the effect of political instability in the Arab countries before and during the Arab Spring. Resource-related greenfield foreign direct investment (FDI) flows—the flow of investment projects that start from scratch like building new factories or manufacturing plants—do not decrease when political conflict intensifies, regardless of whether the conflict is nationwide or geographically dispersed. However, non-resource-related greenfield FDI flows decline with political conflict. We also find that less geographically diversified multinationals are more sensitive to the risk of conflict.

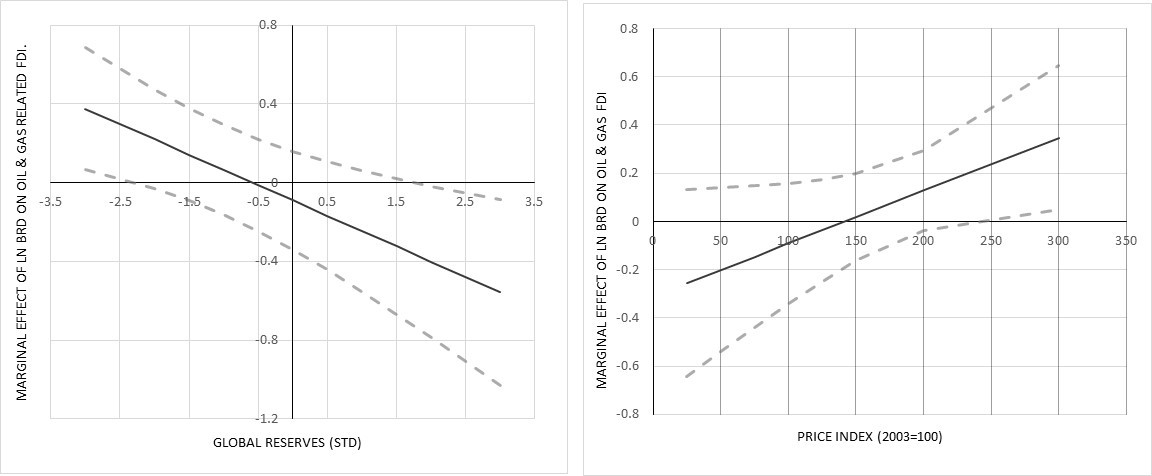

Figure 1: Marginal effect of battle-related deaths on oil-and-gas-related FDI at different levels of oil and gas reserves and prices

Source: Witte, Burger, Ianchovichina, and Pennings (2016).

The insensitivity of the big oil companies to political conflict can be attributed to the high profitability of oil extraction and these companies’ geographic constraints on location choice during the period of estimation (Figure 1). The two mechanisms at play—the size of the economic rents and the geographic constraints on location choice—are related. During periods of commodity booms, high profitability and limited investment opportunities reinforce one another. However, when new technologies (such as hydraulic fracturing) reduce the constraints on location choice or economic rents from resource extraction drop due to other reasons (e.g., a fall in world oil prices), energy multinationals’ appetite for investment in fragile countries declines considerably. Their sensitivity to political conflict comes close to that of multinationals in other sectors.

Furthermore, we find that only relatively persistent and high-impact political conflicts have a significant and negative effect on greenfield FDI. Sporadic acts of terrorism and political assassinations tend to be low-impact events and do not affect most greenfield investments, while repression through political terror is positively associated with FDI in the extractive industry as it reduces the risk of government change and therefore opportunities to renege on resource license agreements.

According to FDI markets data, in terms of value more than 13 percent of all greenfield investment flowing to developing countries in the period from 2003 to 2012 went to countries experiencing a political conflict with at least 25 battle-related deaths per year, and nearly 5 percent went to countries experiencing a war. Our paper implies that political-violence risk should be priced differently depending on the characteristics of the investing firm and the type of political violence. Simply put, one size does not fit all.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

One size does not fit all: Multinationals’ sensitivity to political violence

April 10, 2017