A version of this article originally appeared on Real Clear Markets on June 26, 2017.

GOP lawmakers may eventually throw in the towel on their campaign to repeal the Affordable Care Act. If so, the road to surrender will have been marked by a strange reversal. Less than nine months ago voters elected a Republican President and Congress pledged to reverse Democrats’ signature achievement in the Obama years. Fierce public opposition has so far prevented conservative majorities in Congress from acting on the pledge. This reversal of fortune is odd because until 2017 there was little sign Obamacare enjoyed broad public support. Yet when the insurance expansion was in jeopardy, many voters had a change of heart. What was once an unwanted, even detested government intrusion became an essential pillar of the American safety net.

One lesson may be that it is harder to take away an entitlement once implemented than it is to enact the entitlement in the first place. What is certain is that voters’ opposition can be aroused when a tangible protection they count might be taken away. As the Democrats learned, it is fiendishly hard to get broad popular support for a complicated reform to improve an already staggeringly complicated system. Before Obamacare passed, the U.S. healthcare system had hundreds of moving parts. The Affordable Care Act added dozens more, few of which were understood by voters. However, it turns out to be much easier for voters to understand that a family, a friend, or a neighbor is about to lose insurance. The only parts of the social safety net we see clearly are those that touch us directly.

Most press coverage of GOP efforts to replace Obamacare focused on two effects of repeal. The first was the impact on taxpayers. Obamacare benefits were financed with premium hikes and tax increases, imposed mostly on high-income families. Rolling back the Affordable Care Act meant those revenue enhancers could be eliminated, lightening burdens on high-income taxpayers, especially those on the very top rungs of the income ladder.

A second effect of Obamacare repeal would be to reduce health coverage or boost premium costs to people who gained access to free or subsidized insurance after 2013. Whatever the blemishes of the Affordable Care Act, it unquestionably boosted the ranks of Americans covered by health insurance. Both the Gallup Poll and the Centers for Disease Control agree that coverage increased sharply after Obamacare was implemented. Between 2010 and 2016 the number of Americans who lacked coverage fell by 20 million. If lawmakers replaced Obamacare with one of the GOP-supported plans, the population without insurance could increase by an equal number or more.

It turns out to be much easier for voters to understand that a family, a friend, or a neighbor is about to lose insurance. The only parts of the social safety net we see clearly are those that touch us directly.

Part of the difficulty of comparing the winners and losers if Obamacare is repealed arises from the fact that there is no simple yardstick for measuring the gains of the winners against the losses of the losers. Most of the winners from repeal had assured health coverage before the Affordable Care Act passed in 2010, and they will still have good insurance if the law is repealed. Their gains can be measured in straightforward money terms, as the drop in their taxes. It is harder to measure the losses of Americans who are deprived of access to affordable coverage. In the short run–so long as they remain healthy–many of them may be financially better off. If the mandate to buy insurance is dropped, some will choose to forego coverage. This could be a good bet for people who are young and healthy. It is a riskier one for those who are less healthy. For people who will lose their newly acquired eligibility for Medicaid, there is no upside. Since Medicaid enrollees receive their coverage for free, they won’t see any savings on insurance premiums.

It is hard to calculate in dollars and cents the gain that comes with good insurance and the economic harm that accompanies a lapse in coverage. These gains and losses seem crucial to people who worry about medical bills or who face a crushing, but unknown, financial burden if they are forced to pay for doctors and hospitals without any insurance. Yet the risk of losing coverage may appear manageable to people in good health who expect to have modest medical bills.

Related Content

The difficulty of computing the money value of health insurance is one reason that coverage is only rarely counted in our measures of household income. Most estimates of a family’s income only include the items that are expressed in dollar terms or are easily translated into money values: wages (before or after taxes), interest and dividends, Social Security and unemployment benefits, food stamps. The economic gains resulting from reliable health coverage are hard to translate into money terms, at least at the level of an individual family.

The Affordable Care Act requires employers to report the cost of coverage under each employee’s health plan. The portion of that cost borne by employers is counted as part of employee compensation. This gives a good indicator of the employer’s cost of covering an average employee, but it is not a reliable guide to the value of coverage to a particular worker. Individual employees may face health risks that make insurance coverage more costly to their employers and much more valuable to the worker. For example, an employee who has suffered a heart attack in the past is more likely to need expensive care in the future. The potential cost of this care makes insurance much more valuable to the affected worker.

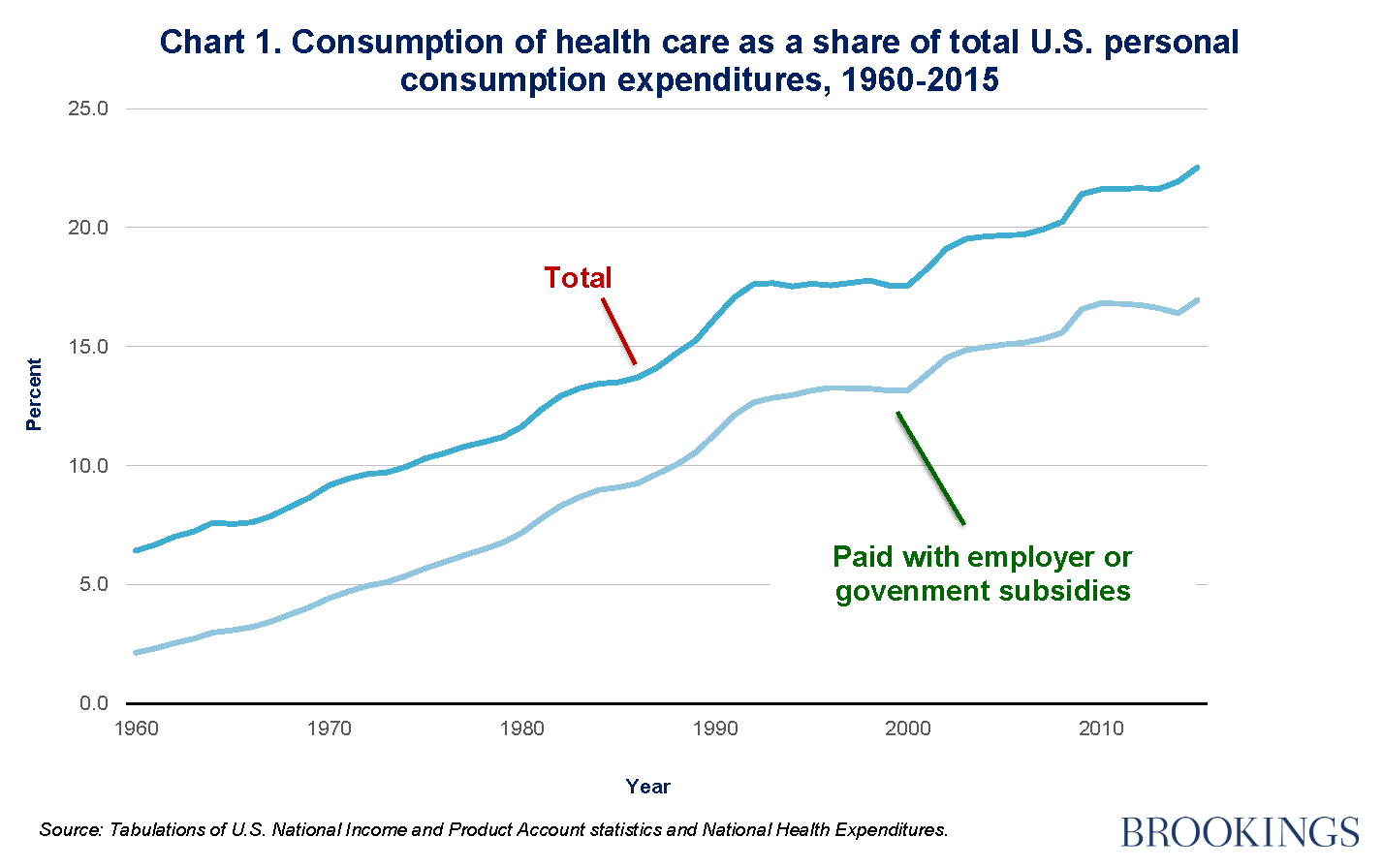

Even though it is hard to quantify the value of decent insurance for a particular family, it is straightforward to calculate the total dollars spent by families, employers, and the government to pay for personal health care. In 2015 this spending accounted for more than 22 percent of all personal consumption expenditures in the United States. The share of consumption spending devoted to health care has risen steeply in recent decades (Chart 1). It was just 6 percent in 1960 and 16 percent in 1990. Despite the big increase in health spending, direct spending by households on payments to health providers and to insurers for health coverage has climbed much more modestly. Most spending for personal health care is now financed by the government (through Medicare, Medicaid, and other public insurance plans) and by employers (in the form of contributions for employee health plans). Government outlays account for about half of all spending on personal health care, and employer spending accounts for a little more than a quarter of it. Out-of-pocket household spending on care, either to medical providers or as health insurance premiums, pays for less than a quarter of the personal health care we consume. This is far below the share back in 1960, when households paid directly for about two-thirds of the care they received.

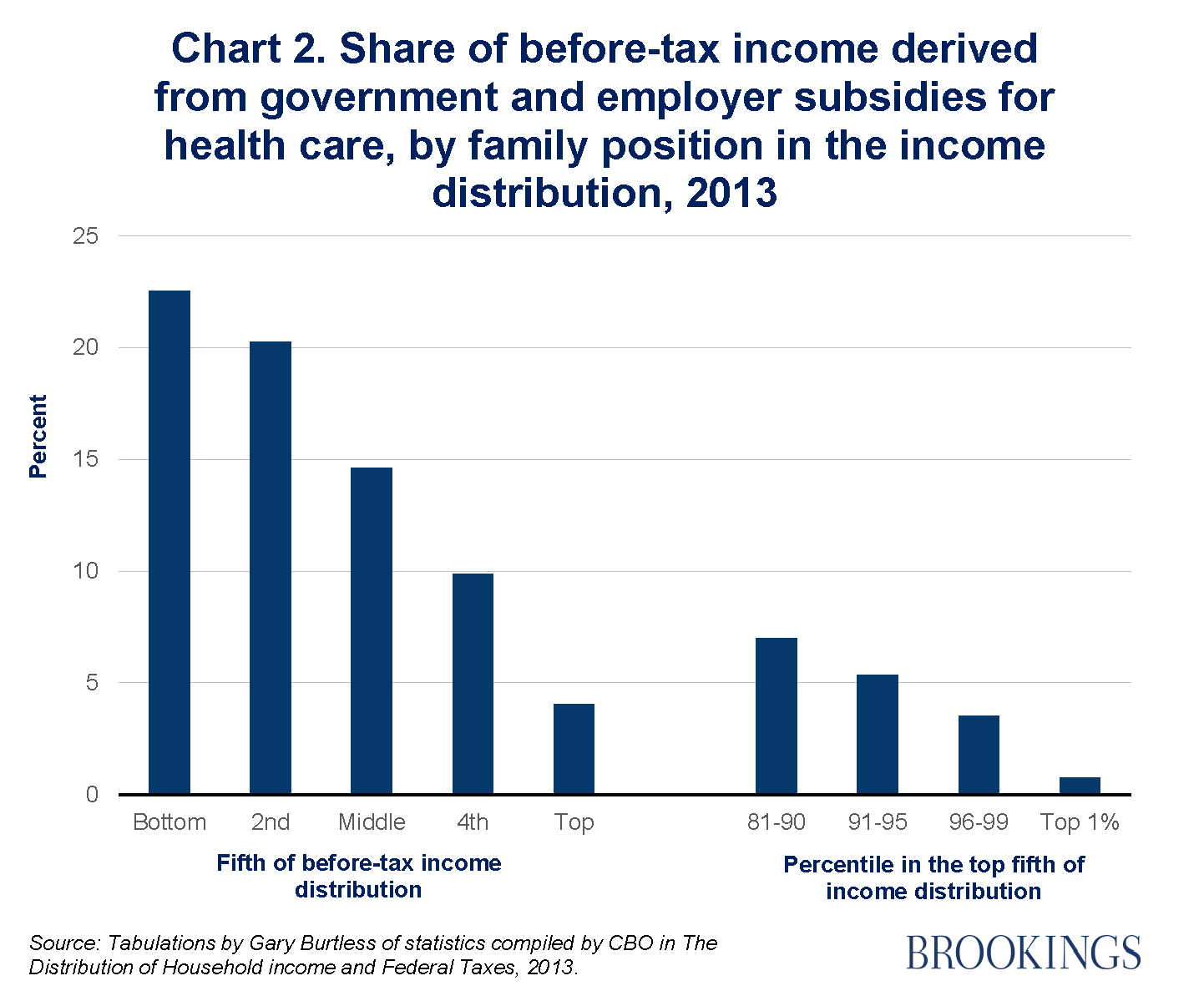

If health care consumers pay directly for only a quarter of the care they consume, it matters greatly how the remaining three-quarters of spending is divided among U.S. families. The Congressional Budget Office tried to make an assessment for the 35 years ending in 2013, just before the Affordable Care Act was implemented. CBO’s estimates of the value of insurance reflect the cost to employers of paying their share of premiums and the cost to the government of paying for coverage under Medicare and Medicaid, net of the premiums paid by the insured. CBO’s calculations show that in 2013 employer premium contributions and government subsidies to the main public health insurance plans represented 9.3 percent of pre-tax household income. None of this is counted in standard income statistics, even though the share of income from health benefits more than doubled between 1979 and 2013.

If health care consumers pay directly for only a quarter of the care they consume, it matters greatly how the remaining three-quarters of spending is divided among U.S. families. The Congressional Budget Office tried to make an assessment for the 35 years ending in 2013, just before the Affordable Care Act was implemented. CBO’s estimates of the value of insurance reflect the cost to employers of paying their share of premiums and the cost to the government of paying for coverage under Medicare and Medicaid, net of the premiums paid by the insured. CBO’s calculations show that in 2013 employer premium contributions and government subsidies to the main public health insurance plans represented 9.3 percent of pre-tax household income. None of this is counted in standard income statistics, even though the share of income from health benefits more than doubled between 1979 and 2013.

When CBO ranked families by their pre-tax incomes, those in the bottom one-fifth of the distribution were found to receive about 23 percent of their 2013 income in the form of health benefits from the government or from employers (Chart 2). When we move up the income distribution, the absolute value of health benefits increases but the percentage of pre-tax family income that consists of health benefits falls. In the top one-fifth of the income distribution, for example, health benefits are twice their level in the bottom one-fifth, but they constitute just 4 percent of families’ pre-tax income.

Obamacare has had an impact on these income patterns, but except near the bottom and at the very top of the income distribution the effects have been modest. If CBO’s tabulations were extended to 2016, when most elements of the Affordable Care Act were fully implemented, it is likely they would show that both the value of health benefits and their share as a fraction of family income increased noticeably in the bottom fifth of the income distribution. Health benefits increased much less in the middle. The gains at the bottom were mainly driven by the expansion of Medicaid coverage and the availability of income-tested subsidies for lower income adults who purchase health coverage through insurance exchanges. The incomes of most people in the middle and upper part of the income distribution were unaffected by Obamacare, because only at the very top of the distribution did families face noticeably higher taxes or Medicare premium hikes.

Obamacare has had an impact on these income patterns, but except near the bottom and at the very top of the income distribution the effects have been modest. If CBO’s tabulations were extended to 2016, when most elements of the Affordable Care Act were fully implemented, it is likely they would show that both the value of health benefits and their share as a fraction of family income increased noticeably in the bottom fifth of the income distribution. Health benefits increased much less in the middle. The gains at the bottom were mainly driven by the expansion of Medicaid coverage and the availability of income-tested subsidies for lower income adults who purchase health coverage through insurance exchanges. The incomes of most people in the middle and upper part of the income distribution were unaffected by Obamacare, because only at the very top of the distribution did families face noticeably higher taxes or Medicare premium hikes.

The shift in public opinion on the value of the Obamacare is traceable to a simple fact. Over time, an increasing fraction of Americans is affected by events that make them eligible for the protections offered under the Act. People are injured or become seriously ill and require expensive care; workers lose their jobs and health coverage. Many of us are only one medical emergency away from bankruptcy if we do not have adequate insurance. It is not easy to measure the financial value of a backup insurance plan if we lose our current health coverage. When the backup plan faces elimination, however, the intangible value of such a plan might seem quite appealing.

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Op-edWarts and all, Obamacare could win a popularity contest that matters

July 26, 2017