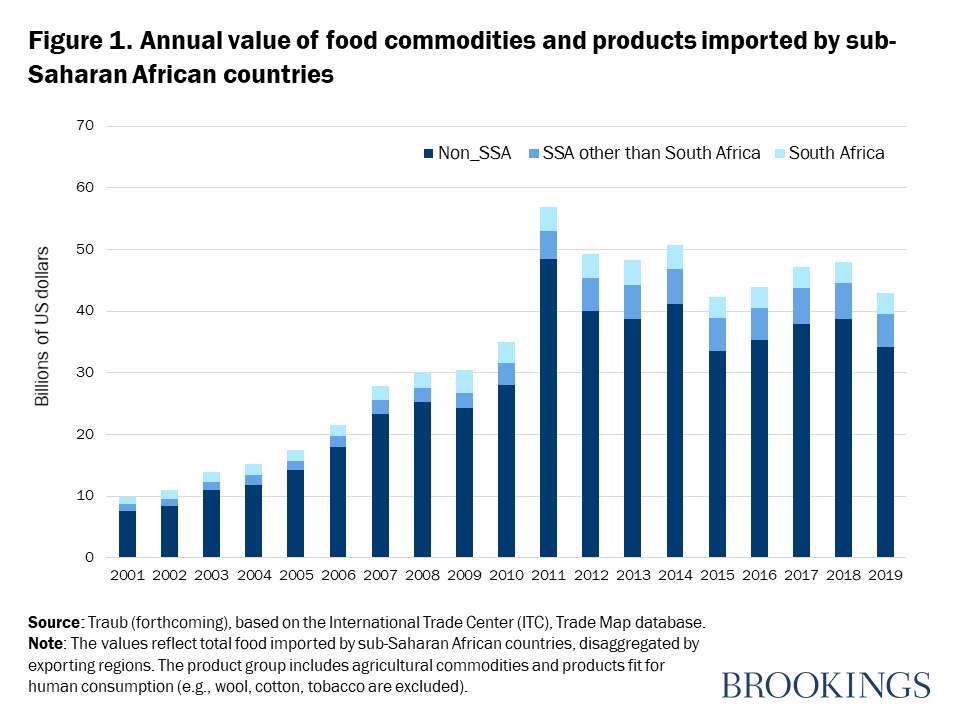

Sub-Saharan Africa’s spiraling food import bill—which stood at $43 billion in 2019—has attracted mounting attention as a worrisome trend. For years, many pundits have wondered why Africa seems increasingly unable to feed itself, despite having much of the world’s remaining unutilized arable land.

This alarming narrative is largely inaccurate. Our research, which disaggregates sub-Saharan Africa’s (SSA) agricultural trade performance by country and type, shows that four countries—Nigeria, Angola, the Democratic Republic of the Congo (DRC), and Somalia—account for most of SSA’s net agricultural import position. The rest of the countries in the region are actually net agricultural exporters. This is good news not only today, but for Africa’s future economic growth through trade, as we explain below.

Three key facts emerge from our analysis.

Sub-Saharan Africa’s food imports are not rising. While the value of SSA food imports rose rapidly during 2005-2011, the annual value of those imports has actually declined slightly and then leveled off since 2011, as shown in Figure 1. While the African Development Bank projected that Africa’s food imports would reach $90 billion by 2030, these projections were based on trends during 2000-2010—a period when global food prices rose rapidly—and do not reflect the more recent 2011-2019 period during which the value of SSA’s food imports has been relatively flat. The fact that—even with rapidly growing demand for food driven by population growth and rising per capita incomes—the value of SSA food imports has not continued to rise over the past decade can be explained by the region’s success in expanding food production. In fact, SSA has recorded the highest rate of agricultural production growth of any region of the world since 2000.

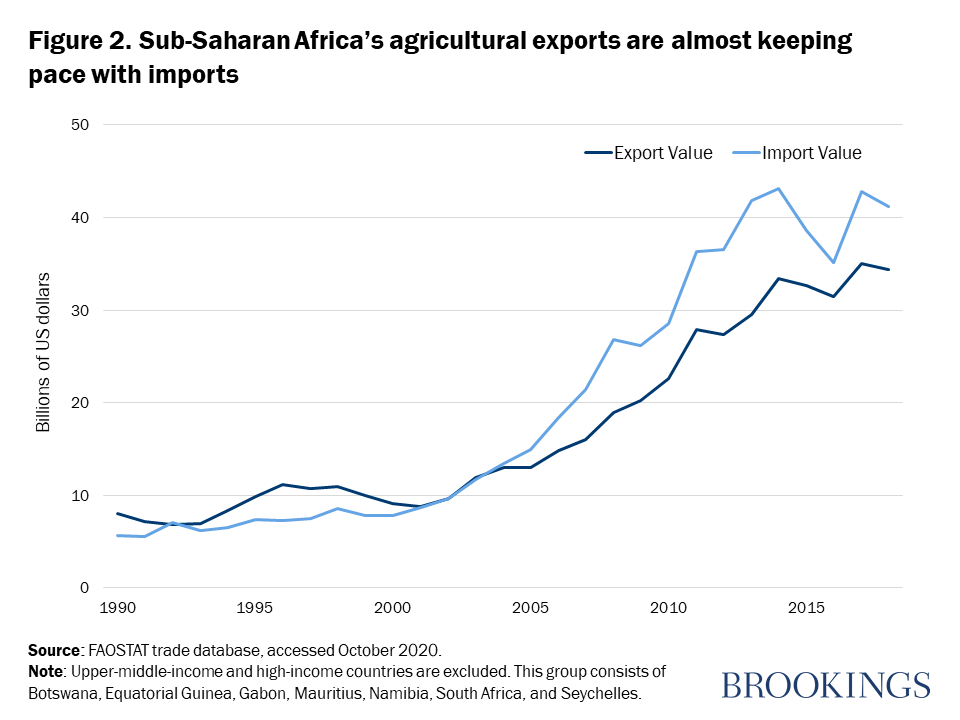

Africa’s agricultural exports are rising too. While SSA imports much more food today than it did two decades ago, it exports much more too (Figure 2). Indeed, the region imported roughly $40 billion per year over the past four years while it exported roughly $35 billion. Moreover, the region’s lower-middle-income countries, led by Côte d’Ivoire, Ghana, and Kenya, have become agricultural export powerhouses, with a net agricultural trade surplus of more than $5 billion per year. SSA’s top exports are mainly tropical commodities such as cocoa, coffee, tea, and cotton, while its main food imports are wheat, rice, soybeans, other oilseeds, and frozen meat products.

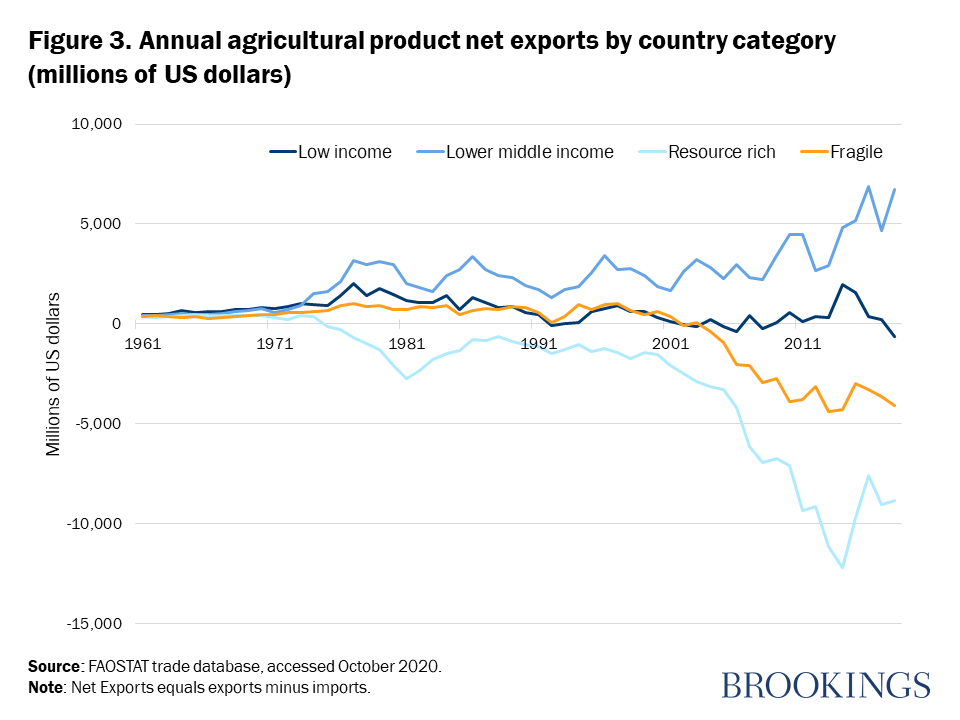

Four countries account for SSA’s agricultural trade deficit. Two types of countries are responsible for SSA’s net agricultural import situation—countries that export oil and minerals, and conflict-ridden states. These countries are almost fully responsible for the region’s net agricultural trade deficit. Nigeria alone is a net agricultural importer of over $5 billion per year, while Angola, the DRC, and Somalia account for another $5 billion per year combined. The role of rising commodity prices in triggering food imports through the Dutch disease mechanisms is visible in Figures 2 and 3, as food imports in resource-rich countries jumped substantially during the 2007-2012 commodity price upswing, and subsequently fell back down. Most of the region’s fragile states are also net agricultural importers.

Note: Low-income countries include Benin, Burkina Faso, Burundi, Eritrea, Ethiopia, Gambia, Guinea-Bissau, Liberia, Madagascar, Malawi, Mali, Mozambique, Niger, Rwanda, Sierra Leone, Tanzania, Togo, Uganda (n=18). Lower-middle-income includes Cape Verde, Cameroon, Comoros, Cote d’Ivoire, Djibouti, Eswatini, Ghana, Kenya, Lesotho, Sao Tome & Principe, Senegal (n=11). Resource-rich (as of 2005) includes Angola, Congo Republic, Mauritania, Nigeria, Zambia (n=5). Fragile includes Central African Republic, Chad, Democratic Republic of Congo, Guinea, Somalia, Sudan, South Sudan, Zimbabwe (n=8).

Africa can capitalize on its rapidly increasing demand for food through agricultural productivity growth and regional trade

As the region’s population grows and gets richer, the demand for food, especially high-value crops and livestock products, will continue to grow. Indeed, rapidly rising demand for food within Africa provides considerable untapped potential for intra-African trade. The proportion of African countries’ food imports originating from other African countries is currently very low, consistently averaging about 20 percent over the past several decades, with one country—South Africa—accounting for over a third of this intra-African food trade (Figure 1). Effective implementation of the African Continental Free Trade Agreement will be an important step in enabling African farmers and agribusinesses to increasingly meet the region’s growing demand for food.

To realize these opportunities for intra-African agricultural trade, though, SSA countries will need to focus on improving agricultural productivity to compete effectively against low-cost imports from the international market. To compete at this level requires investments in agricultural R&D and extension services. African states will also have to reduce the costs of trade, by removing tariff and nontariff barriers, streamlining customs procedures and improve regional transport links in order to realize the full potential of the AfCFTA.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Unpacking the misconceptions about Africa’s food imports

December 14, 2020