This post discusses my monthly update of the Barnichon-Nekarda model. For an introduction to the basic concepts used in this post, read my introductory post (Full details are available here.)

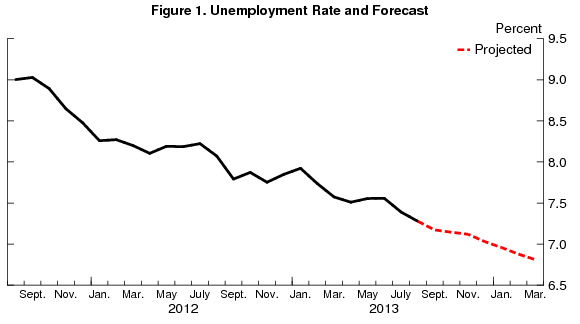

Due to the government shut-down, the unemployment rate for September may not be released on Friday. Here is the closest substitute: the most accurate forecasting model predicts 7.2% for September.

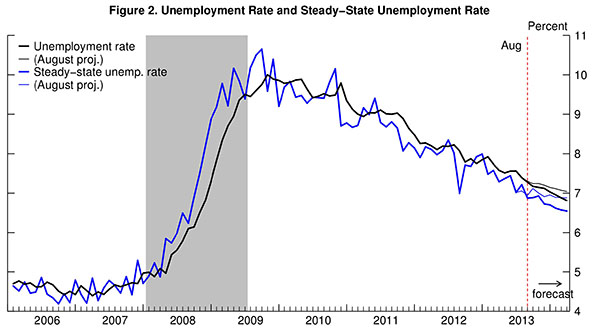

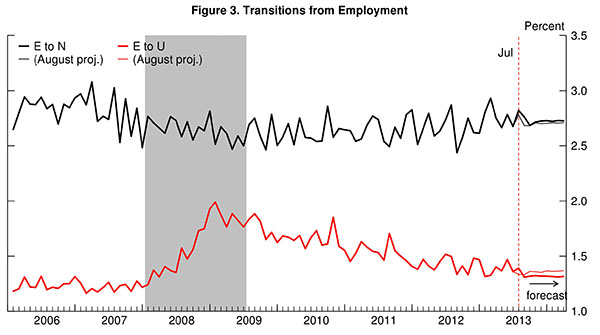

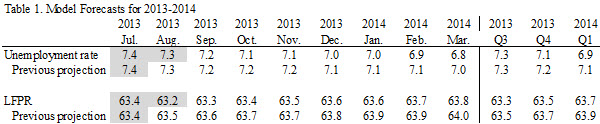

Back in August, the unemployment rate dropped to 7.3%—as the model predicted last month—pushed down by the steady-state convergence dynamics. The decline in unemployment will continue, with a 7.2% jobless rate expected for September, but at a slow pace, being mainly driven by a steady-state convergence dynamics, not by large improvements on the hiring front. The steady-state unemployment rate currently stands at 6.9% and is expected to remain flat over the next couple months. Towards the end of the year however, the model anticipates some improvement driven by an acceleration in the pace of hiring and in workers’ job finding rate (UE in figure 3). The steady-state unemployment rate is expected to resume its decline around November and reach 6.5% by March 2014, which will translate into a 6.8% unemployment rate in March 2014.

This forecast is easily understood by looking at the projected behavior of the “steady-state” unemployment rate. The steady-state unemployment rate, the rate of unemployment implied by the underlying labor force flows—the blue line in figure 2— stands currently at 6.9%. Our research shows that the actual unemployment rate converges toward this steady state. With a steady-state unemployment rate level lower than the actual rate (6.9 versus 7.3, a 0.4 percentage point difference), this “steady-state convergence dynamic” is pushing the unemployment rate down, implying a decline in unemployment going forward. However, going forward, the model anticipates the steady-state unemployment rate (SSUR) to remain roughly constant at 6.9 % over the next couple months (figure 2). The steady-state convergence dynamic will thus become weaker as the unemployment rate converges to 7 percent, implying a decelerating rate of decline until the end of the year. Towards the end of the year, the situation will improve again, and SSUR is expected to resume its decline to reach 6.5% by March 2014.

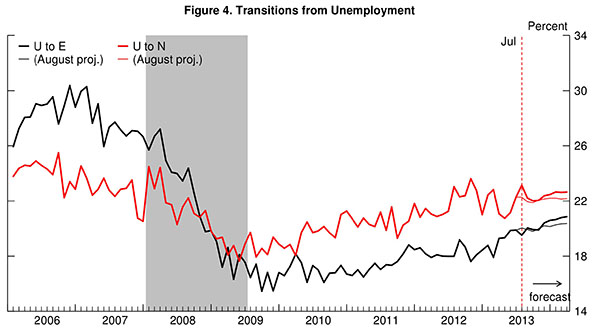

To forecast the behavior of steady-state unemployment (and hence of the actual unemployment rate), the model propagates forward its best estimate for how the flows between employment, unemployment and out-of-the labor force will evolve over time. Despite the large drop in new claims for unemployment insurance at the beginning of September, the number of job openings continues to be desperately flat since March. So it is a little puzzling to see the model anticipating a rebound in hiring towards the end of the year (figure 3). Since the model’s greatest strength lies in near-term forecasts (next 3 months), I am tempted to take the 2014 forecasts as a lower-bound for the future level of unemployment.

To read more about the underlying model and the evidence that it outperforms other unemployment rate forecasts, see Barnichon and Nekarda (2012).

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Unemployment Likely To Fall to 7.2% in September, With Smaller Gains Going Forward

October 3, 2013