Athens desperately needs to sell a 3 billion euro, five-year Greek government bond with a yield of around 4.5-4.7 percent as it strives to convince the markets—as well as domestic voters—that the economy is about to recover after eight years of depression and austerity. So, it is willing to pay much more than the 0.89-1.2 percent that the European Stability Mechanism (ESM) is currently charging as part of Greece’s bailout program. Indeed, on July 11, the ESM announced that 7.7 billion out of a total tranche of 8.5 billion euros would flow to the Greek state, of which 6.9 billion euros will cover loan maturities that expire this month. Then, on July 21, the board of the International Monetary Fund approved in principal a conditional loan worth as much as 1.6 billion euros for Greece—just the reassurance requested by many euro-area creditors. Yet Greece’s Gordian knot is far from untied and the most recent conditional acceptance by the fund regarding what amounts to a “precautionary stand-by arrangement” won’t translate to an immediate disbursement.

The urgent need for a “Grexit” to the global borrowing markets’ either amounts to a symbolic government effort to show investors that the economy is recovering or is something political. Despite recent optimism expressed about the likelihood of a Greed re-entry, its timing is far from guaranteed. According to the latest news, the European Commission, the European Central Bank and the IMF—also known as the troika—seem to have reacted by favoring a postponement of a bond issuance by Greece for the next few days, weeks, or even months. But questions remain, as the troika surely knew in advance about the Greek government’s intentions.

The IMF is insisting that Greece’s debt is hugely unsustainable, especially in the long-term. According to the fund, measures either taken or proposed so far by the Europeans, such as the 15-year interest deferral and maturity extension for some of the European Financial Stability Facility/ESM loans, won’t make the country’s debt burden sustainable. The IMF’s July 20 Debt Sustainability Analysis (DSA) just confirmed this view. Greece is not qualified by any standard to exit its program and re-enter the markets. Among other things, such a move would add new debt to the already colossal burden it currently carries, which is equivalent to around 180 percent of GDP. So, even if Greece successfully borrows with a 4.5 percent interest rate, which will make the debt even more unsustainable, mainly by adding to the government’s gross financial needs (GFN).

Paradoxically, it is not only the German finance minister who is painting a far rosier scenario, whereby Greece sticks to reforms agreed with the creditors through the conclusion of the program in August 2018, after which the country is to re-enter the capital markets and borrow at sustainable rates. HSBC’s analysis, as seen in Figure 1, emphasizes that, with a primary fiscal balance of around 2 percent, gross financial needs should be well below the level required as part of the IMF’s DSA.

Figure 1: Debt-to-GDP ratio (LHS) and grow financing needs (RHS) for Greece

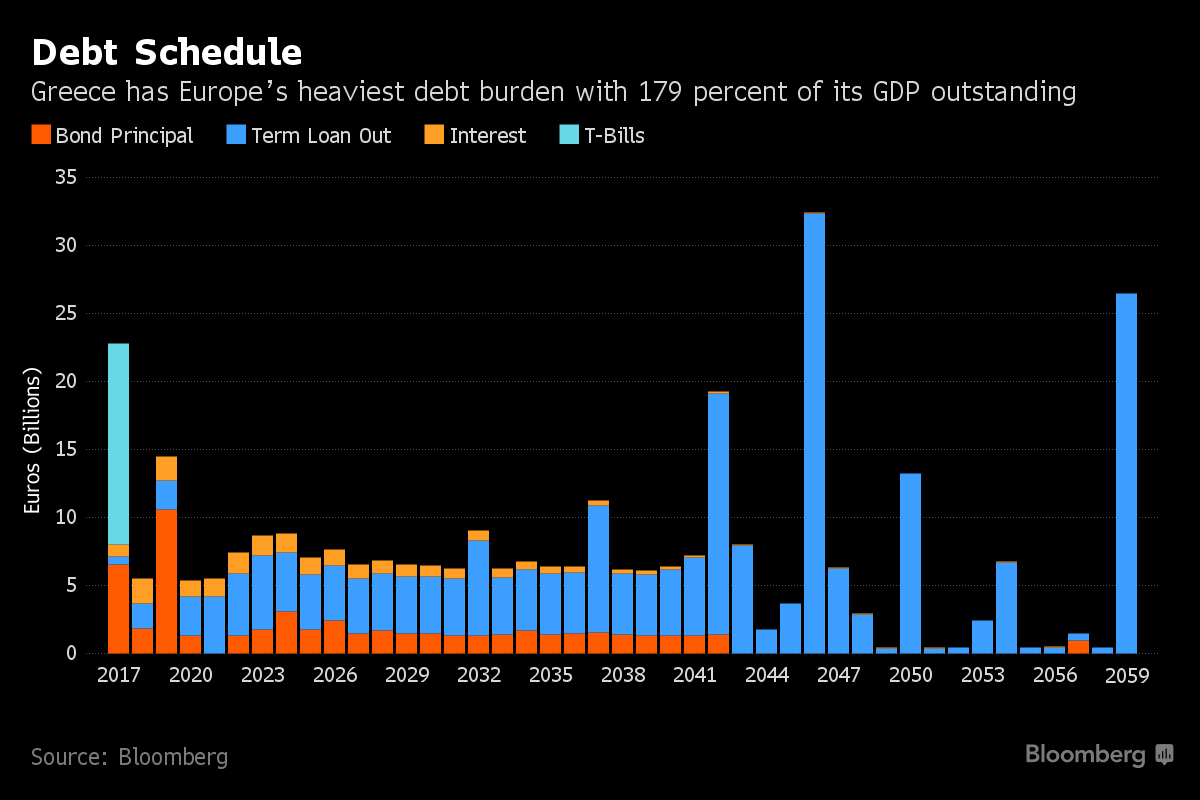

But, another, even more awkward fact regarding the Greek government is being overlooked. The second evaluation—of the third bail-out program agreed two years ago—was delayed for a year and a half because of the fact that Prime Minister Alexis Tsipras insisted on getting in advance specific promises from creditors regarding a debt relief schedule, arguing openly that Greek debt is hugely unsustainable, a view that is widely shared with international media, think tanks and independent analysts, the IMF, and other organizations (Figure 2).

Figure 2: Debt schedule for Greece

But again, even if we look closely at Figure 2, debt seems to begin to possibly become unsustainable only after 2040. This (surprisingly) coincides with the IMF DSA analysis (Figure 1), where in fact only after 2040 do gross financial needs seem to climb above the IMF’s 15-20 percent sustainability threshold. It should be noted here that no special analysis is available regarding the way and methods that the gross financial needs are calculated by the IMF, but this is another story.

This puzzle becomes even more complicated if one takes into account the sky-high coupons that the government is willing to pay to exit to the markets and borrow. Why such a high-yield when debt is clearly sustainable, at least in the short term? Furthermore, Greece is in fact in a five-year program and potential bond buyers should feel relatively secure to buy a bond that matures in 2022. That would clearly justify much lower yields. And consequently, why such a big split between Greece’s rate (4.5 percent) and Portugal’s (1.3 percent) (Table 1) when the latter has to service more than 60 billion Euros compared to the 33 billion Euros that the former has to service?

Figure 3: Debt service in billion euros

It may all come down to politics. Creditors—Europeans and Germans in particular—are eager to tell voters that the Greek program has at last succeeded and that Greece is now ready to borrow from the markets. Tsipras also desperately wants to tell domestic voters that “…borrowing from the markets is a proof that… we will soon be independent from creditors, leaving austerity behind us.” Or, Tsipras may plan to borrow from the markets at any cost so as to be prepared for the coming elections, meaning sending “helicopter money” to the voters. In this case, one is wondering whether the institutions (formerly the troika) are well aware of this version of the story and if they condone it.

Related Books

Tsipras said some months ago that “…we will soon order markets to dance according to our interests.” Well, now that he is ready to borrow with a sky-high interest rate, he may understand that it is the markets that have the upper hand. And since he needs the money to tell voters that at last his government has succeeded in something, Tsipras may now understand that it takes two to tango. Just in case he knows how to dance.

Related Content

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

To exit (to borrow from the markets) or not to exit: Greece’s new dilemma

July 21, 2017