This article was amended on May 25, 2026, to clarify daily production volumes of crude and refined product.

The shortfall in global oil supply due to the closure of the Strait of Hormuz has roiled markets and prompted discussions of a global recession. Yet, despite this massive shock—on the order of 20% of global oil supply—the conflict in Iran has to date failed to boost oil prices to catastrophic levels, with oil benchmarks remaining below their 2022 highs in the wake of Russia’s invasion of Ukraine. (Price movements for natural gas and some refined products have been more severe.) In this post, we focus on crude oil and present a rough framework to explain why global prices have yet to skyrocket, while also advancing a timeline to assess when prices could reach more alarming levels. The bottom line is that the supply shortfall will build in coming months as temporary buffers are depleted. And if markets grow increasingly pessimistic over an eventual resolution to the impasse in the strait, oil prices may rise materially higher.

Structural versus temporary forces in global oil markets

Sharp crude price gains have been constrained by three primary factors. One, structural adjustments in the crude oil trade—including pipeline bypass and the onset of new crude sources—that mitigate the supply shock. Two, the existence of global inventories that are designed to address supply volatility and provide temporary relief in instances such as this. And three, an overarching belief in markets that the impasse in the Strait of Hormuz will be resolved in short order.

From this perspective, the current market for crude is characterized as a race between the levels of temporary buffers and expectations for the duration of the impasse. This framework is supported by observed price action since the start of the conflict. The sharp swings in global oil prices reflect changing views on the likely duration; indications that the strait will remain closed for longer sees oil prices rise, while headlines suggesting a quick resolution prompt oil prices to tumble.

Our contribution is to quantify temporary and structural adjustments in the current shortfall. This distinction is important because—as the closure drags on—the ability of temporary forces to offset supply disruptions dwindles. Differentiating between temporary and structural forces allows us to identify what conceivably is a lasting supply deficit that may last for many months, regardless of near-term developments.

Prior to this conflict, around 20 million barrels of oil and refined product transited the Strait of Hormuz daily, with volume markedly lower in recent months. Measured against global production of crude and other liquid fuels of around 100 million barrels of oil per day (mb/d), plus similar volumes of refined product, this ranks as the biggest supply disruption ever.

Our focus here is on crude oil, for which pre-conflict trade through the strait totaled around 15 million barrels per day (mb/d) according to the International Energy Agency (IEA). We focus on crude because supply disruption here feeds into all subsequent markets by forcing refineries to cut production, which in turn, pushes up prices for jet fuel and other derivatives. Moreover, focusing on crude incorporates the impact of pipeline workarounds, which serve as a permanent and important offset to the supply disruption.

Prior to the war, global crude oil trade stood at about 45 mb/d, suggesting that approximately one-third of global trade is potentially disrupted before structural and temporary adjustments.1 If not offset, such a shock is sufficient to spike energy prices to levels consistent with a global recession.

Below, we first distinguish between structural adjustments (i.e., those that can continue indefinitely) and temporary adjustments, then attempt to quantify the duration that temporary adjustments can withstand the supply shock.

Structural factors:

- Pipeline bypass: Saudi Arabia and the United Arab Emirates (UAE) maintain pipelines allowing exports to circumvent the Strait of Hormuz chokepoint. Saudi Arabia’s East-West pipeline to the Port of Yanbu on the Red Sea has a maximum capacity of 7 mb/d, while the UAE’s pipeline to the Port of Fujairah in the Gulf of Oman has a maximum capacity of between 5 and 1.8 mb/d. Factoring in that some capacity in both of these pipelines was already being used prior to this conflict, we estimate incremental capacity from these bypasses at around 5.7 mb/d.

- Pre-war surplus: Prior to the war, global crude oil markets were in surplus, driven especially by rising supply from the Americas—including the U.S., Guyana, and Brazil. Global refinery throughput and production averages from 2025 put the pre-war surplus around 0.7 mb/d, which contributed to a five-year high in inventory build. The structural mismatch between supply and demand was sufficiently acute that an October 2025 IEA report characterized the imbalance as an “untenable surplus,” speculating that “something has to give.”

Temporary Factors:

- Inventory drawdowns: The IEA announced a more than 400 million barrel emergency oil release from government stockpiles shortly after the closure of the Strait of Hormuz, of which 301 million barrels are crude oil. The most high-profile of these is flow from the U.S.’ Strategic Petroleum Reserve (SPR). Factoring in emergency releases by foreign governments, this amounts to around 2.5 mb/d over a four-month period, which represents a meaningful buffer to oil prices. However, this buffer is time limited, as the fixed initial emergency release stockpile will deplete quickly, and any additional emergency releases would draw from already-reduced national reserves.

- Floating storage and sanctions waivers: At any point in time, a large number of fully laden oil tankers are in transit. As a result, a roughly constant amount of crude is at sea while it makes its way to its ultimate destination. After the U.S. sanctioned Lukoil and Rosneft in October of last year, Russia started stockpiling crude on oil tankers idling at sea. Figure 1 shows how this “floating storage” changed the picture for oil at sea, with the stock of Russian crude stockpiled at sea rising to as much as 90 million barrels ahead of hostilities. After war broke out and the strait closed, this stock was mostly run down as U.S. sanctions waivers allowed buyers in Asia to purchase it. Iran built a similar floating storage in anticipation of the U.S. blockade—Figure 1 shows a smaller rise by about 60 million barrels—which is another buffer for global supply shocks.2 However, the inventory drawdown is a finite buffer and will get depleted relatively quickly. Indeed, the U.S. in April sent letters to financial institutions in several countries, including China, threatening secondary sanctions if they facilitate the sale of Iranian oil, a measure designed to materially encumber Iran’s floating storage.

Quantifying the global supply shortfall over time

We now assemble a timeline for these structural and temporary factors and, more importantly, project it forward through the end of this year. Our goal is to quantify at what point the temporary factors holding down oil prices are exhausted, whereupon the global imbalance between demand and supply widens sharply. Figure 2 shows a monthly time series for the Strait of Hormuz supply shortfall factoring in structural and temporary factors.

Beginning February 28, directly following the U.S. strike on Iran, we estimate that crude oil flows through the Strait of Hormuz are reduced from 15.0 mb/d to 2.5 mb/d, the level at which it remains up to the continuing U.S. blockade starting April 13, at which point flows drop to 1.5 mb/d.3 Permanent buffers, such as increased pipeline oil flows and the previous global supply surplus, replace roughly 6.4 mb/d of lost Hormuz crude flows.

Temporary buffers play a large role in reducing the overall market adjustment, which is the difference between pre-U.S.-strike Hormuz crude flows and buffers, but they also deplete quickly. Russian floating stocks, with an estimated average of 1.6 mb/d buffer beginning March 12, are depleted by the end of April; similarly, Iranian floating stocks, with an estimated average of 1.3 mb/d buffer beginning April 13, are depleted by the end of May. The emergency oil release from IEA members beginning March 11 and depleting by July 9 provides a buffer of 2.5 mb/d. Thus, by the middle of July, the full extent of temporary buffers will have been exhausted, with an overall market adjustment of 7.1 mb/d, roughly 16% of global crude oil trade, needing to be absorbed.

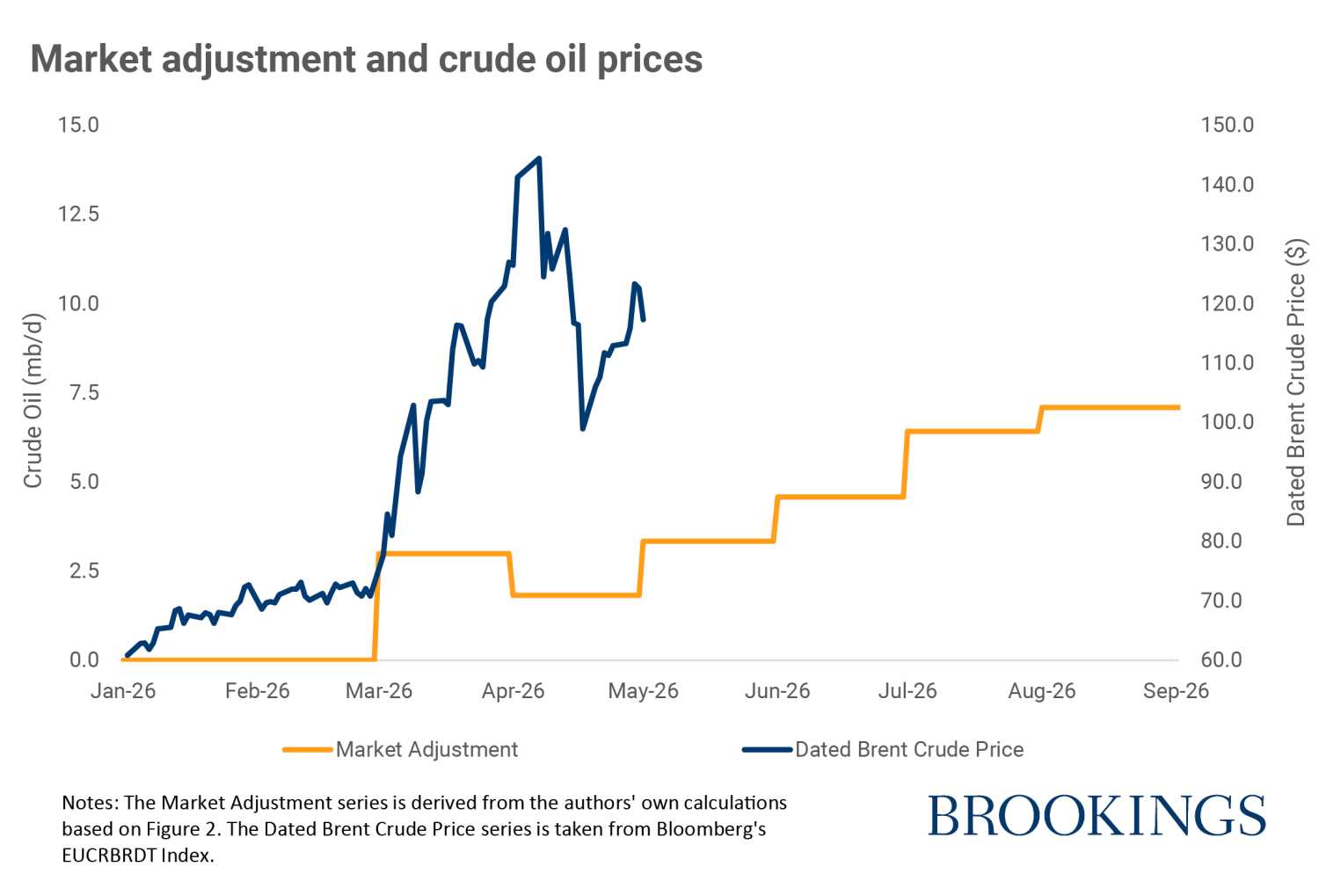

The path of global oil prices so far has closely tracked the evolution of this supply shortfall. Figure 3 plots the dated Brent price, from Bloomberg’s EUCRBRDT Index, together with our estimate for the evolving global supply shortfall. As markets digest headlines, they lengthen or shorten their estimate for the duration of this conflict, increasing or decreasing the size of the shortfall. Our projection for the evolution of the shortfall suggests that oil prices could rise substantially further if the Strait of Hormuz does not reopen by the end of June. For example, based on historical relationships between supply changes and expected market prices (i.e., price elasticities), an expected 10% decline in supply between the start of the war and June suggests Brent crude prices could be $120 a barrel. Once markets expect the temporary buffers will be exhausted, the market price could rise to nearly $150 per barrel based on these elasticities.

The volatility in global oil prices reflects market efforts to price the duration of Strait of Hormuz closure. The longer this persists, the worse the global supply shortfall grows. In this post, we disentangle the various forces in this shortfall and quantify how rapidly it grows as temporary buffers fall away. The potential is for oil prices to rise substantially further if the Strait of Hormuz remains closed for months to come.

It is fair to say that the scale of the supply shortfall is now well-known to markets. But the timeline on which temporary buffers run out and how this interacts with prices is of critical importance. This interaction means non-linear outcomes in prices—in other words, sharp price spikes—are possible the longer this conflict is expected to take. The potential for non-linear outcomes grows the longer oil tanker traffic through the Strait of Hormuz remains severely encumbered.

Related Content

Authors

-

Footnotes

- While the focus of this article is on crude oil, it bears mentioning that shortages in refined oil products, already being acutely felt in products like jet fuel and petrochemical feedstocks, will only exacerbate the need to increase refinery throughput, to which crude oil is the primary input.

- Estimates for Russian and Iranian floating storage are the authors’ own calculations, derived from analysis of Bloomberg’s FZWWFST Index, a measure of global crude oil floating storage.

- Based on the authors’ own estimates of limited crude oil export flow through the Strait of Hormuz from February 28 through April 13 preceding the U.S. blockade, at which point flows drop further.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

The timing of the impending crude crisis

May 22, 2026