Want to hear more from the Hutchins Center on this topic? Sign up for our Jan. 9 event here.

What is investment? How is it different from other types of government spending?

Public spending can be divided into consumption and investment. Consumption spending goes for goods and services that produce benefits today, such as health care for the elderly or mowing the lawn on the Washington Mall. Investment is spending that will provide benefits in the future, such as scientific research or building a new highway or better educating children. While conceptually simple, the distinction between government consumption spending and investment spending is, as the White House Office of Management and Budget puts it, “a matter of judgment.”

This explainer will focus primarily on public investment as traditionally defined: local, state and federal government spending on physical infrastructure and research and development. Broader definitions of public investment include education, health care and other benefits for children that pay off in the future. The White House Office of Management and Budget and the Congressional Budget Office, for instance, define federal investment spending to include physical capital and R&D as well as education and training.

Where does the government spend public investment dollars?

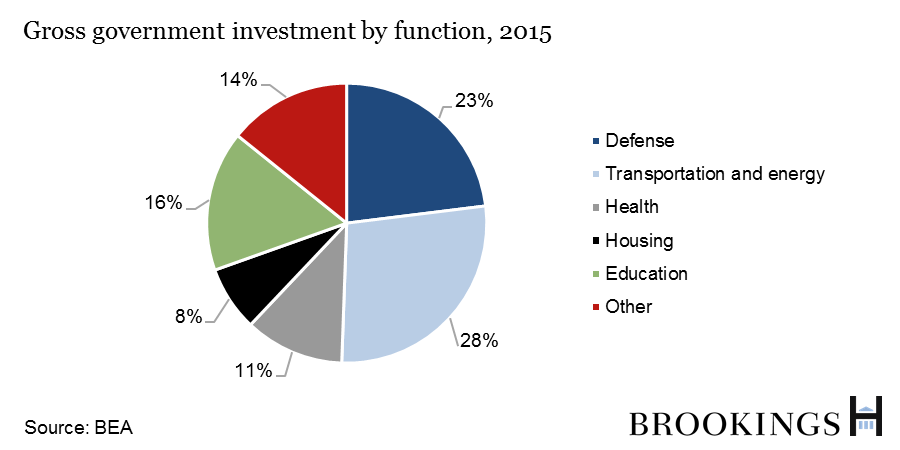

In 2015, the largest shares of gross investment at all levels of government went to economic affairs, defense, education, and health.

What are the trends in investment at all levels of government?

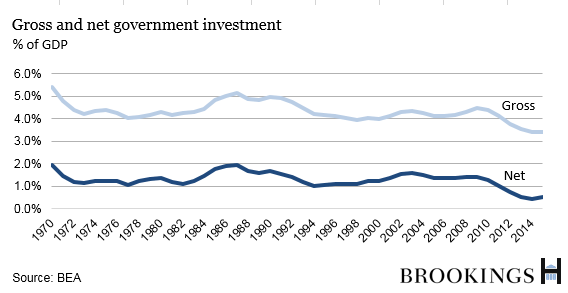

In 2015, spending on structures, equipment, software and research and development at all levels of government was equivalent to about 3% of GDP. Net government investment — that is, government spending on infrastructure minus the deterioration of old infrastructure – was a small fraction of that: close to 0.5% of GDP, far below the historical range of between 1% and 2% of GDP during 1970-2010.

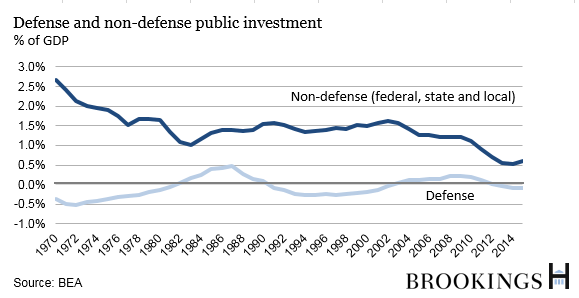

Although investment in national defense, at least to the extent it is prudently made, benefits society and the economy in the form of stronger national security, recent public discussion of government investment focuses on the non-defense activities that have a clearer link to private-sector productivity growth, profits and wages. Net non-defense public investment spending has been trending down for the past decade.

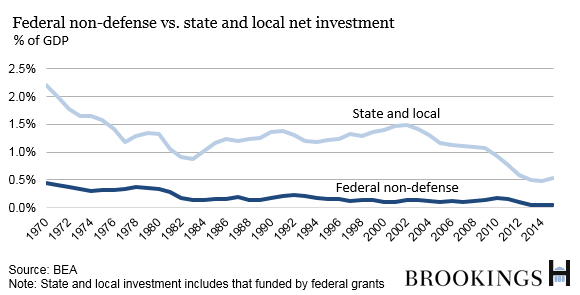

The bulk of non-defense public investment spending is done at the state and local level, some financed by federal grants and some by local borrowing or taxes. State and local investment spending has been significantly more volatile than federal investment over the last few decades, and accounts for most of the recent decline in total net government investment.

Why has infrastructure spending been declining?

The reasons for the recent decline are subject to debate. One possible explanation may be the lingering effects of the Great Recession; for example, a slow recovery in property tax receipts that many local governments rely on to finance infrastructure projects. Another possible explanation may be that the Great Recession made many state and local governments postpone capital projects due to worries about the debt they have already accumulated as well as debt they expect to have in the future.

Under current law, federal non-defense investment is projected to decline further relative to the size of the economy over the next decade. The Congressional Budget Office (CBO) estimates that by 2023, federal non-defense investment (including grants to state and local governments) will be less than two thirds of its average share of GDP from 1962 to 2012. These projections, however, are based on the assumption that discretionary spending caps established under the 2011 Budget Control Act continue to hold through 2021 and that there will be no major policy changes. President-elect Trump campaigned on a promise to substantially increase infrastructure spending.

How does public infrastructure spending vary across the states?

State and local capital spending – on buying, building and renovating buildings as well as buying land, equipment and structures – declined in most states between 2000 and 2014, measured as a share of each state’s GDP. Only 12 states and Washington, DC saw an increase in state and local capital expenditures as a percent of their GDP over that period. The biggest declines were in Nevada, Utah, Michigan, Tennessee and Massachusetts. The map below shows the divergent capital spending pattern across states.

What’s the case for spending more on infrastructure?

Many advocates for increasing investment point to our crumbling roads and bridges. One element of the case for spending more on infrastructure than we do today is that the average age of many types of infrastructure has increased over the last 15 years, most notably for highways and streets and public transportation. The average age for streets and highways, for example, grew from about 23 years in 2000 to over 28 years in 2015 (See the chart below). The average age of infrastructure can be lowered by investing in either new infrastructure assets or maintenance and repair of the existing physical capital.

How does the federal government pay for infrastructure?

Federal spending. Federal spending can be used to finance infrastructure directly – that is, by federal employees or by contractors hired by the federal government. Spending can also take the form of grants or loans to state and local governments. In 2015, federal capital grants accounted for about 22% of state and local gross investment. Some of those grants for infrastructure spending are provided to state and local governments on the condition that they contribute a certain percent of project costs (so-called matching requirements); federal funding for grants can also be determined by a formula or on a project-by-project basis. Some federal spending is discretionary, meaning that the Congress appropriates funds each year; other spending is financed out of trust funds with dedicated revenues. The Highway Trust Fund, for instance, is largely funded from the 18.4-cent-a-gallon federal tax on gasoline and the money is supposed to be spent on the repair and expansion of the highway system and support of mass transit

Public-Private Partnerships. A PPP is a legally binding contract between a public sector entity and a private company where the partners agree to share some portion of the risks and rewards inherent in an infrastructure project. For example, a private company might borrow money to build a road, and then collect tolls to pay off the bonds. In a recent report, IMF notes that the evidence on the success of PPPs is mixed. For example, on the one hand, under a PPP, financing is typically provided by a firm upfront and is convenient for a resource-constrained public agency. On the other hand, private financing is typically more expensive than government borrowing.

Tax subsidies for state and local borrowing. Another way the federal government finances infrastructure is by lowering the cost to states and local governments, which can finance large capital projects by issuing municipal bonds – obligations that entitle owners to interest plus repayment of principal at a specified date. An important feature of municipal bonds is that interest payments received from them are not subject to the federal income tax; this federal subsidy allows states and localities to borrow more cheaply than corporations. Tax-exempt municipal bonds reduce the cost of borrowing by state and local governments, but the benefits of the tax break flow primarily to the highest-income Americans for whom tax-exempt interest is attractive. In an innovation during the Great Recession, Congress created temporary Build America Bonds program. Interest was taxable to investors, and the federal government provided a subsidy to the issuing state and local governments.

What other ideas for financing infrastructure are being discussed?

Infrastructure bank. Often envisioned as an independent federal government agency, an infrastructure bank would select and finance infrastructure projects through direct loans, loan guarantees and lines of credit. Proponents say that this approach would lead to higher-quality investments being selected and could improve project management and coordination of investments across agencies and across states. Others argue that the allocation of federal spending is an inherently political choice that Congress cannot delegate to an independent agency.

Tax credits for private investors. As proposed by two advisers to Donald J. Trump – economist Peter Navarro and business executive, now Commerce Secretary-designate Wilbur Ross – giving private contractors tax breaks for investing in infrastructure would give the private sector the freedom to decide which projects to invest in and allow them to make profits from the tolls or fees they would charge to consumers. One of the major drawbacks of this approach is that private contractors will concentrate their investments on the most profitable projects and shun projects that are needed but can’t produce a commercial return, such as repairs in public schools.

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

The Hutchins Center Explains: Public investment

January 3, 2017