This report is the sixth and final in a series on “Europe’s energy transition: Balancing the trilemma” produced by the Brookings Institution in partnership with the Fundação Francisco Manuel dos Santos. It was finalized for translation in mid-March 2026.

Executive summary

In a continually darkening geostrategic environment, energy security is becoming an ever more urgent goal for European policymakers. Russia’s invasion of Ukraine, recent U.S.-Israeli strikes on Iran, and a more coercive United States have Europe rethinking its external energy dependencies, almost all of which come with political baggage. Europe is also focusing on internal energy security—ensuring energy reaches consumers efficiently, reliably, and affordably.

Energy integration within the European Union (EU) and with neighboring states enhances all three aspects of the energy trilemma: security, affordability, and sustainability. When a member state faces disruptions to electricity or natural gas supply, cross-border transfers from neighboring states can smooth over supply and price shocks. As Europe continues its clean energy transition, greater integration allows better management of intermittent renewable electricity like solar and wind, reducing curtailment. Overall energy costs in the EU will also decrease, as more demand can be met by the least expensive available generation within the bloc and connected neighboring countries.

But there are economic and political challenges. Building and modernizing infrastructure like transmission lines and pipelines will require major funding from the EU and individual member states, along with private funding. The sheer scope of costs will lead to questions about who pays for what. Each country will have to give up some control of its energy system. Although system integration lowers overall energy costs, not every consumer will be better off all the time, and some energy producers face new competition from cheaper sources of energy elsewhere in Europe. These situations may create political constituencies against integration. Regulatory policies like the Emissions Trading System and the Carbon Border Adjustment Mechanism (CBAM) can stymie integration where it is needed most: in prospective EU member states.

In September 2025, European Commission President Ursula von der Leyen identified eight critical regional energy bottlenecks that span the EU and its periphery. Priority projects across the Baltics, the Balkans, the Iberian Peninsula, the Mediterranean, and the North Sea demonstrate how these challenges might be overcome by extending or deepening existing energy systems and connections and championing new decarbonization projects.

In today’s threat environment, supply shocks are the new normal. However, policymakers should not assume that this alone will sell the need for new cross-border projects. Rather, they will need to address social and economic costs from the beginning. With sustained political will, a more integrated European energy system could even become a driving force for European growth and competitiveness.

Introduction

Finding itself under pressure from three revisionist powers—first Russia and China, and now the United States under President Donald Trump—has galvanized Europe. European leaders now realize that they must move fast to mitigate their vulnerabilities and boost their sovereignty. Across the continent, governments are reassessing deterrence and defense (conventional and nuclear), the resilience of physical and digital infrastructure, and supply security, both at the EU level and within most of its member states. The same is true of many of the EU’s neighbors, including those seeking membership (like the Western Balkans), and other nations that desire pragmatic, deeper collaboration on cross-border issues (like Switzerland or the United Kingdom). Energy security has become a key component of the continent’s quest for greater strategic autonomy.1

Until recently, discussions around European energy security focused mainly on external security. The goal was to ensure reliable imports for a continent still significantly dependent on fuel imports despite its ongoing transition toward renewables.2 Yet the external supplier environment is increasingly uncertain. Key suppliers—including Russia, Qatar, and most recently, the United States—carry political risk or are willing to actively disrupt or weaponize supply security for political leverage. The U.S.-Israeli strikes on Iran that began in late February have exacerbated that uncertainty. As a result, strengthening internal security has become ever more important. Energy must reach EU industrial and private consumers efficiently, reliably, and at a lower cost.

The European single market was established in 1993 to reduce physical and regulatory barriers to the free movement of people, goods, services, and capital in the EU. In this turbulent geostrategic environment, the single market is no longer viewed solely as a tool to enhance prosperity and competitiveness. Instead, it is increasingly seen as a framework for maximizing sovereignty and security by integrating other areas of the European economy, such as capital and banking markets, digital communications, and common borrowing. In his seminal 2024 report on European competitiveness, former European Central Bank President and Italian Prime Minister Mario Draghi identified 10 key sectors for deeper integration into the single market, with energy in first place. Draghi’s report followed a similar paper by Enrico Letta, another former Italian prime minister.

In her State of the Union address on September 9, 2025, European Commission President Ursula von der Leyen endorsed this emphasis, noting the energy sector as one of three key areas where the European single market remains incomplete.

This is how the European Commission defines energy integration:

“Energy system integration means creating stronger links between different types of energy carriers (such as electricity, liquid, gas and solid fuels, heat and cold), energy infrastructure and consumption sectors. This integration supports the optimisation of the energy system to deliver decarbonised, reliable and resource-efficient energy services, at the least possible cost.”

In practice, energy integration takes a variety of different forms. It involves building physical infrastructure—like power transmission cables and gas pipelines—to connect markets, while also reducing policy or commercial barriers that prevent cross-border energy flows.

Energy security is now clearly recognized as an essential European public good. Yet integrating Europe’s energy systems comes with non-trivial political challenges—especially relating to solidarity and fairness, which cannot be resolved by markets alone. Integration can make the overall energy system less expensive, but allocating the costs and benefits will require some form of state- or EU-level intervention. Without it, policies could break down under political strain, especially since not every consumer will be better off all the time. In a time of polarized and divided politics—and especially in view of the rise of far-right parties that are constantly exploiting social tension for political gain—getting the policy’s politics right is no longer just an implementation problem, but central to preventing a policy failure. Given current debates over “de-greening” and even over the viability of the EU Emissions Trading Scheme (ETS)—considered one of European climate policy’s real successes—the risk of beggar-thy-neighbor policies and a race to the bottom is real.

Integration enhances all three elements of the energy trilemma

Greater integration in EU energy markets—particularly in electricity, where future demand is expected to grow most dramatically—can enhance all three aspects of the energy trilemma: security, affordability, and sustainability.

Energy security is a key argument: greater integration would allow energy flows across borders to make up for supply shortfalls or interruptions (and prevent price spikes with possible political fallout). Russia’s invasion of Ukraine and its subsequent cutoff of natural gas supply to Europe is only the most recent case. Countries were unevenly exposed to the Russian supply shock, and market fragmentation prevented energy trade from acting as a buffer for the countries most dependent on Russian gas, particularly in Eastern Europe. (An earlier paper in this series described the regional impacts of the Russian gas cutoff in detail.) The continuation of Russia’s war against Ukraine, concerns about the Trump administration’s willingness to use Europe’s dependence on U.S. liquified natural gas (LNG) for political coercion, and the current turmoil in the Middle East strongly suggest that Europeans should reckon with further supply uncertainty. But supply challenges can also happen within the Western European space, as the Iberian Peninsula blackout in April 2025 showed—and they too can be weaponized in disinformation operations.

Greater integration also increases sustainability and, in most cases, affordability, by enabling greater access to renewable electricity. Integration would allow more renewable electricity generation to be built where resources like sun and wind are most plentiful. It would also reduce or eliminate the need to curtail renewable generation when there is not enough demand to absorb it. Since renewable electricity is the lowest-cost resource when it is available, integration could lower electricity prices across the EU. Prime Minister Kyriakos Mitsotakis of Greece—which has also seen massive electricity price spikes—put it forcefully in a Financial Times op-ed: “Market integration is happening à la carte and few want to share their cheap electricity. So we end up with negative prices in one country while another has prices in the triple digits. This is madness.” The EU estimates that integration in today’s electricity market saves consumers 34 billion euros (about $40 billion) each year, and greater integration could increase these savings to 40 billion euros to 43 billion euros annually by 2030.

In addition to reducing the cost of power itself, the system also benefits from greater integration. A power system with a lot of intermittent resources is easier to balance when it covers a larger geographic area,3 so integration reduces the challenges that come with a grid more reliant on renewables. Shared power dispatch, or managing the grid across larger geographic areas, could also reduce the costs of running the system.

Integration can also boost European competitiveness by lowering costs. EU natural gas and electricity prices are higher than in most industrialized economies, and the gap between the EU and its main competitors is growing. A key reason for disparity is the EU’s reliance on expensive imported LNG, whose costs then flow through to electricity prices. (Substituting Russian pipeline gas with LNG after the invasion eliminated a vector of coercion, but it increased both prices and price volatility.) Additionally, inefficiencies and a lack of integration in the electricity system also increase energy costs. Therefore, the EU must have cost control as a central goal to maintain economic competitiveness. Integration means that energy within the EU can move around efficiently and seamlessly, keeping overall costs down.

Yet integrating Europe’s energy system faces significant obstacles. It will require massive infrastructure investments and involve difficult discussions about funding. Even a fully optimized system would likely increase costs for some consumers at some times. Balancing the costs and benefits among different regions and interest groups (private households vs. industrial consumers, for example) is especially difficult; as discussed in the next two sections of this paper, the nature of this challenge differs across the electricity and natural gas systems.

Expanding electricity integration to move renewable power to demand centers

Electricity is the path to decarbonization. Any reasonable energy transition scenario predicts surging electricity demand and a growing share of energy use supplied as electricity, largely met by renewables. Thus, EU energy integration policy focuses primarily on integrating the electricity grid, which could deliver more efficient use of existing infrastructure, greater resilience, and lower capital costs for new infrastructure in an improved system.

In the EU, governance of electricity markets is shared between the EU and the member states. The EU establishes a framework for the market, including wholesale and retail market rules. Member states establish their own supply structures—the mix of electricity generation sources—and are responsible for ensuring security of supply within their territories.

A number of EU policies support electricity system integration. The Trans-European Networks for Energy is the EU regulation governing the connection of member countries’ energy networks. It was revised in 2022 to make it more consistent with EU climate policy. The EU set out a vision in 2023 for a market where electricity can flow freely across borders, enhancing the security and reliability of supply for everyone. In December 2025, the European Commission released the European Grids Package, a plan to implement this vision, and estimated that the EU’s electricity grids need 1.2 trillion euros in investment by 2040.

An optimized, fully integrated electricity market requires eliminating infrastructure and regulatory barriers to trade, allowing wholesale electricity prices to converge across the EU. This would enable electricity to be produced at all times by the least expensive available generation sources in the entire EU. (Prices paid by consumers might still differ across nations and consumer types because of taxes and other fees.) Renewables are the least expensive source of power when they are available, since they have extremely low marginal costs. Greater integration will allow greater penetration of renewable power and reduce curtailment (wasting power that cannot be used) at times of high renewable power generation.

This ideal, fully integrated electricity system is likely impossible to achieve, and Figures 1 and 2 show that the goal of converging electricity prices is far from realized. Prices differ greatly across countries, even in some neighboring countries. Differences between residential and nonresidential electricity prices within a country reflect policy choices about how to distribute system costs across residents and industry. That said, differences in prices across countries, especially for nonresidential consumers, are mostly a function of discontinuities in the power system, where insufficient infrastructure exists to allow electricity to flow from low-cost to high-cost areas. Reducing these discontinuities, therefore, can significantly lower price differentials.

To advance its integration goals, the EU set a target for all member states: each country should have sufficient cross-border transmission capacity to import or export 10% of its electricity demand by 2020, rising to 15% by 2030. However, six countries in continental Europe have not yet met the 2020 target—France, Greece, Italy, the Netherlands, Poland, and Spain. These are among the largest economies in the EU, each with its own political and financial reasons for lagging. (Cyprus and Ireland have also not met the targets, but their island geography makes that a particular challenge.)

The EU electricity system reaches beyond the bloc’s borders, but the level of integration differs. Several neighboring countries are full participants in the system. For example, Norway is a key participant in the EU electricity grid, with a higher rate of connection to EU countries than many EU member states. In 2025, Switzerland signed an agreement to participate fully in the EU internal electricity market. Its central geographic location and long history of connection with its EU neighbors make its integration beneficial for both sides. Both of these countries participate in the EU Emissions Trading Scheme, which applies a carbon price to electricity generation, making integration easier from a policy perspective. (As another paper in this series described, Ukraine managed the extraordinary feat of complete synchronization with the European grid only a few weeks after Russia’s full-scale invasion in 2022; yet Russia’s continued bombardments throughout a severe winter have deeply damaged Ukraine’s energy infrastructure.)

However, EU policy acts as a barrier to the greater integration of other nonmember countries. Beginning in February 2027, the Carbon Border Adjustment Mechanism will apply the EU carbon price to electricity imported into the EU and thus functions like an entry tax for non-renewable electricity. Non-EU countries could avoid CBAM charges by participating in the ETS or establishing a similar program. However, doing so would raise costs for all domestic industries—not just for electricity generation—making it politically difficult before it is required for EU membership. Non-EU countries in the Western Balkans region (Albania, Bosnia-Herzegovina, Kosovo, Montenegro, North Macedonia, and Serbia) are examples of countries that are experiencing policy barriers to greater integration with the EU energy system.

Aggregating natural gas supply

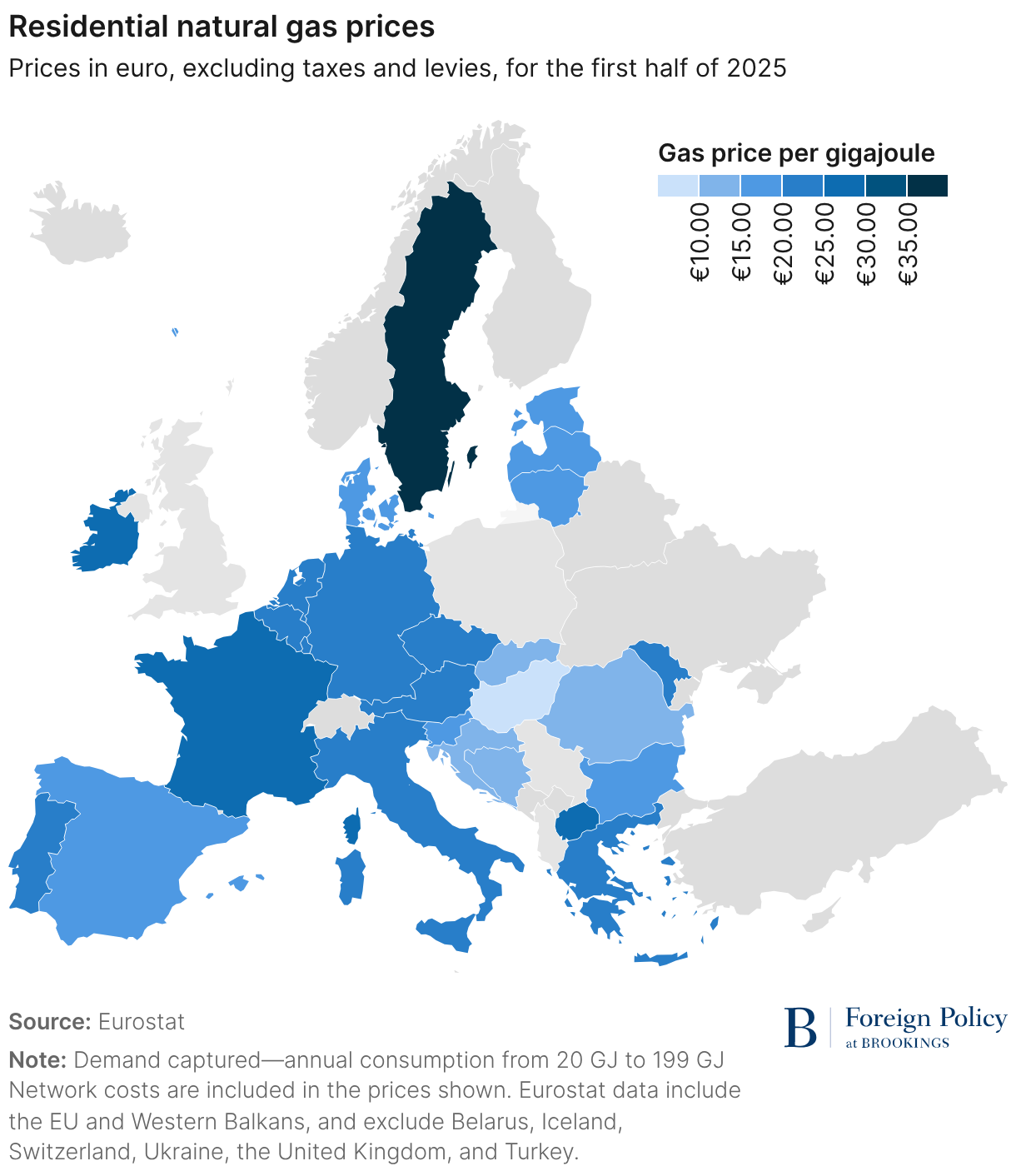

Integration of the EU natural gas system has been underway for more than two decades. EU reforms in the early 2000s, especially the second and third energy packages in 2003 and 2009, laid the groundwork for the development of more integrated gas markets. These reforms opened access to infrastructure, eliminating monopolies and increasing the number of buyers and sellers. Furthermore, the development of virtual gas trading hubs in Europe, particularly the Netherlands’ Title Transfer Facility (TTF), has provided sufficient liquidity for transparent price development based on gas market fundamentals, rather than linking gas prices to those for oil.4 These changes brought greater price convergence across parts of Europe. However, the TTF is located in northwestern Europe and is based on market conditions there. Eastern and southern Europe are less connected to the rest of the bloc, and thus, TTF gas prices are less reflective of market conditions in those regions.

Since Russia’s full-scale invasion of Ukraine in 2022, EU natural gas security policy has focused on eliminating EU reliance on Russian supply. Progress so far has been impressive: a 45% share of imports from Russia in 2021 declined to a 19% share in 2024. As part of the REPowerEU Plan in response to Russia’s aggression, the EU set a goal of reducing total natural gas demand by 15% (compared to average demand in 2017-2021), achieving a 17% reduction in early 2025. (Some of this total no doubt represents demand destruction due to high prices, rather than conservation or efficiency.) Furthermore, the EU plans to eliminate all Russian gas, both pipeline and LNG, by the end of 2027.

Gas integration policies helped the EU cope with the Russian disruption and will continue as the phaseout deadline approaches. In some cases, integration involves new infrastructure to provide alternative supply routes. For example, the Poland-Lithuania interconnector, which began operation in May 2022, connects the Baltic states and Finland to the EU gas market through Poland. (Estonia and Lithuania were the first to ban imports of Russian natural gas, including LNG, in April 2022. Latvia followed in July 2022.) In other cases, the reversal of existing pipelines allowed new supply to flow to areas that were formerly dominated by Russia and were dependent on Russian gas supplies. For example, Moldova now receives gas from the reversed Trans-Balkan pipeline, which, instead of shipping Russian gas through the Balkans to Turkey, now moves non-Russian gas northward through Romania and Ukraine.

Other gas integration policies focus on markets rather than infrastructure. In April 2023, the EU began a joint purchasing initiative called AggregateEU, with the goal of pooling demand from European companies to achieve more competitive offers from global suppliers. The mechanism matched nearly 100 billion cubic meters (bcm) of supply and demand—almost a third of the EU’s natural gas demand in 2024—before it expired in March 2025. EU Energy Commissioner Dan Jørgensen recently announced plans to launch a new, similar joint gas purchasing scheme to facilitate the EU’s ongoing efforts to eliminate Russian gas supply.

Figures 3 and 4 show that, similar to electricity, natural gas prices vary across the bloc. These variations are largely due to differences in gas supply and gas connections. LNG has been much more prevalent after 2022, even more so since January 1, 2025, when pipeline exports of Russian gas through Ukraine ended.

New priorities in EU energy integration

Since 2013, the EU has designated cross-border energy infrastructure projects that are considered critical for implementing the EU’s energy objectives as “projects of common interest.” These projects benefit from faster planning and permit approvals, along with access to funding through the Connecting Europe Facility. The similar designation of “projects of mutual interest” applies to projects that connect the energy systems of EU countries with those outside the EU.

In her 2025 State of the Union address, von der Leyen described eight critical regional energy bottlenecks in the EU to be addressed in an initiative called Energy Highways. This appears to be a subset and combination of established projects of common interest. The priority areas are:

- Strengthen power links in the Baltic states.

- Better connect the Iberian Peninsula across the Pyrenees to France.

- Improve energy supplies in the Balkan region and eastern neighboring states.

- Improve price stability and energy security in southeastern Europe.

- Connect Cyprus with continental Europe to end its electricity isolation.

- Turn the North Sea into an offshore interconnector hub.

- Build a south hydrogen corridor connecting the North Sea to the Mediterranean.

- Build a southwest hydrogen corridor from Portugal to Germany.

A closer look at these prioritized areas sheds light on the nature of the EU’s internal integration challenges and the ways that they can be overcome. The first five of these are extensions of the current energy system or deepening of existing connections, whereas the last three are more aspirational proposals toward a decarbonized energy system.

Baltic states

Historically, Estonia, Latvia, and Lithuania were connected to the Russian energy system, a legacy of their incorporation into the Soviet Union between 1940 and 1991. They joined the EU in 2004 and applied to join the European electricity grid in 2007, but the integration process took time. Then, Russia’s full-scale invasion of Ukraine in 2022 and its weaponization of gas supplies to Europe created a new sense of urgency. Synchronization with the EU grid occurred on February 8, 2025, 10 months ahead of the original schedule, severing electricity ties with Russia and Belarus and connecting to the EU grid through Lithuania’s short border with Poland.

Plans are in the works to further deepen the connection between the Baltics and the rest of the EU. The high-voltage linkages already in place are LitPol between Lithuania and Poland, NordBalt connecting Lithuania and Sweden, and Estlink 1 and 2 between Estonia and Finland. These total 2,200 megawatts (MW) of capacity. Future plans include an additional 700 MW connection to Poland and, more speculatively, a 2,000 MW connection with Germany. The Baltic Energy Market Interconnection Plan aims to achieve energy market integration among the eight EU countries that surround the Baltic Sea (with nonmember Norway participating as an observer). All of these projects are or have been EU projects of common interest.

Iberian Peninsula

A previous paper in this series focused on energy issues on the Iberian Peninsula. The peninsula has significant energy resources and infrastructure, including LNG terminals, a natural gas pipeline from Algeria, and a greater percentage of renewable generation than the EU average. The challenge is that Iberia is poorly connected with France and beyond to the wider EU. Spain is able to import or export only 3.6% of its electricity demand—well below the EU goal for electricity system integration. Portugal’s connections exceed the goal, but it can only connect to the rest of Europe through Spain. The limited connections between the Iberian Peninsula and France did not cause the widespread blackout of April 28, 2025, but greater connections would make such events less likely and easier to recover from.

The peninsula’s LNG terminals are generally underutilized, in part because of insufficient connections to the rest of Europe. Five of the seven LNG terminals in Spain ran at utilization rates less than 33% in the first half of 2025, compared to the EU average of 52%. Greater connection with the rest of the EU in both gas and electricity might lead to higher LNG terminal utilization rates and lower electricity and gas prices in neighboring countries.

Balkan region and southeastern Europe

Electricity prices in southeastern Europe—from Greece, Bulgaria, and Romania through the Western Balkans—are significantly higher than those in much of the rest of Europe. Natural gas generation often sets the market price in these areas, and the switch from Russian pipeline gas to LNG made that gas much more expensive. Additionally, limited interconnections with neighboring countries and other parts of Europe, fragmented grids, and weak regional communication contribute to high prices and increase the likelihood of outages. Most countries in the region, including non-EU countries that are part of the Energy Community Treaty, are members of the Central and South-Eastern Europe Energy Connectivity Group, formed in 2015.

The wider Balkan region includes 11 countries, some within the EU and others aspiring to join, which creates unique challenges for energy integration. The five EU member states (Croatia, Greece, Bulgaria, Romania, and Slovenia) apply EU law and regulations. The six non-EU countries (Albania, Bosnia and Herzegovina, Kosovo, North Macedonia, Montenegro, and Serbia) are parties to the Energy Community Treaty. Through this agreement, they have committed to implementing some portions of EU energy law to further the goal of creating an integrated energy market and as part of their long-term goals of joining the EU. However, these countries are not members of the ETS, meaning that carbon emissions from their electricity systems are not priced today, and that electricity imports from these countries will be subject to the CBAM in 2027. The CBAM is therefore likely to become a barrier to deeper market integration between EU and non-EU countries in the region.

Despite the regulatory challenges, greater integration still makes sense. The Trans-Balkan Electricity Corridor is the region’s flagship electricity integration project. It is a system of high-voltage connections in various stages of planning and completion. Lines connecting Serbia and Romania are complete, with further construction ongoing across Serbia to Montenegro and Bosnia and Herzegovina. Eventually, the connection is intended to reach Italy. The project supports many regional goals, including improving reliability by replacing outdated transmission lines and allowing broader access to the region’s renewable energy resources. The region’s EU members benefit from integration when hydrological conditions allow the region to export hydropower (although CBAM regulations will make it difficult to designate this power as renewable, and thus exempt from charges).

An additional aspect of Balkan energy connectivity is the change in the operation of the Trans-Balkan natural gas pipeline after Russia’s invasion of Ukraine in 2022. The pipeline runs through Greece, Bulgaria, Romania, Moldova, and Ukraine. Prior to the war, it transported Russian gas to Turkey and southeastern Europe. Today, it has been reversed; it now transports gas imported as LNG at terminals in Greece and Turkey along with pipeline gas from Azerbaijan north into Bulgaria, Romania, and Ukraine. This is part of the larger Vertical Gas Corridor project, intended to rearrange gas supply in the region away from Russia. Several related projects are included on the projects of common interest list, demonstrating the EU’s commitment to the region.

Cyprus

In addition to being a geographic island, Cyprus today is an electricity island, with no connections to the wider EU grid. The Great Sea Interconnector (GSI) is a project to build a high-voltage direct current line connecting the electricity grids of Cyprus, Greece, and, perhaps later, Israel. The project has encouragement from the EU as a project of common interest, and a ceremony marking the start of construction was held in October 2022. However, the GSI is a technically and politically demanding project, certainly the most demanding included in the Energy Highways program. The GSI would be one of the world’s longest and deepest subsea cables. Additionally, cost sharing among the participants has been a challenge, along with objections from Turkey, which does not recognize the Republic of Cyprus’s exclusive authority over the island’s maritime zones.

North Sea offshore interconnection

The North Sea is an area of tremendous potential for offshore wind energy. Offshore interconnection hubs could collect electricity generated at multiple projects and distribute it to multiple countries’ grids. This hub-and-spoke structure is intended to be more flexible than links from individual projects to points onshore, providing greater supply security to all parties and reducing the likelihood of curtailment. But achieving the benefits of this structure requires deep cooperation among the participating countries.

The North Seas Energy Cooperation supports the development of interconnection hubs in the North Sea. At the North Sea Summit in Hamburg in late January 2026, the group further committed to the cooperative nature of the project, agreeing that up to 100 gigawatts (GW) of the 300 GW wind power goal would be developed through cross-border cooperation projects. Challenges remain in financing these projects and in determining how to share the costs among their beneficiaries.

Hydrogen corridors

Hydrogen is a pathway to decarbonize applications, like high-temperature processes in heavy industry, that cannot be easily electrified. Hydrogen can be produced with electricity by splitting molecules of water into their components, hydrogen and oxygen, in a very energy-intensive process. Renewable hydrogen is produced using renewable electricity.

In 2022, the REPowerEU plan called for 10 million metric tons of domestic renewable hydrogen production and an additional 10 million metric tons of renewable hydrogen imports by 2030. Achieving this goal would require pipelines to move imported hydrogen from ports to centers of industrial demand. Within the EU, hydrogen can be produced in areas with abundant renewable energy resources—like North Sea wind power or Iberian solar power—and moved via pipeline to demand centers. Alternatively, electricity can be moved via the transmission system, and hydrogen can be produced where it is used, a more likely scenario for hydrogen users away from the planned corridors.

The two hydrogen pipeline corridors described in the Energy Highways program, the North Sea to the Mediterranean and Portugal to Germany, are part of the planned European Hydrogen Backbone initiative. This larger initiative aims to create a liquid, competitive market for hydrogen across the EU. Greater development of hydrogen has broad support among potential users in heavy industry, but opposition primarily centers around the very high costs and energy needs of green hydrogen production.

Repurposing natural gas pipelines for hydrogen is an area of study for the EU. However, hydrogen causes pipeline metal to become brittle, meaning that not all existing natural gas pipelines can transport hydrogen, and others will need to be operated at lower pressure when carrying hydrogen. Nonetheless, a study by a large group of natural gas companies found that as much as 60% of the European hydrogen pipeline network in 2040 might be created from repurposed natural gas lines. Luckily, some areas with good natural gas infrastructure, like the North Sea, also have good renewable energy and hydrogen potential, making this infrastructure repurposing easier. Still, the EU estimates that 240 billion euros in investment in hydrogen networks will be needed by 2040.

Lessons from the prioritized projects

Electricity storage is underrepresented in EU integration and investment plans. Storage is essential in a grid reliant on intermittent sources of generation. It lessens intermittency—and the price spikes and political costs that accompany it—and allows more renewable electricity to be considered a “firm” source of supply. No electricity storage projects are included in the Energy Highways program, and electricity storage makes up only 24 of the 235 most recent projects of common or mutual interest lists, released at the end of 2025.

The most urgent integration needs are in the EU’s newer and prospective members. Taking on the EU regulatory scheme was not and will not be an easy task for many of these countries, particularly due to the costs to businesses of such programs as the ETS. Now, infrastructure integration is the key to fully enjoying the benefits of the EU integrated energy market, reducing energy costs, and thus gaining payback for the upfront work. Many projects included in the Energy Highways and projects of common and mutual interest lists are focused on the periphery, showing the EU’s commitment to its newer and prospective members.

Barriers to integration

To achieve greater integration, countries must give up some control of their energy systems. Although relinquishing some control provides benefits overall, as described earlier, not every energy provider or consumer benefits all the time. This sets up constituencies that can hold back the integration process. For example, inexpensive hydropower meets most of Norway’s electricity needs, but growing electricity connections to the EU have caused Norway’s electricity prices to rise when the EU calls for more power. The political consequences became clear in early 2025, when an EU-skeptical party pulled out of the country’s governing coalition in response, leaving Prime Minister Jonas Gahr Støre at the helm of a minority government.

France represents a different kind of challenge: it exports much of the power from its large (and aging) fleet of nuclear power plants, but its electricity generators do not want to compete with lower-cost renewable generation in Spain and Portugal. A way to prevent this competition has been to limit interconnection. (An earlier paper in this series identified France and Spain’s inadequate connectivity as a key issue.) In this case, integration might be good for consumers, but bad for the incumbent industry. The French government is attempting to square this circle by building new nuclear reactors and pursuing wind and solar energy at the same time—yet the latter is meeting fierce opposition from the French far right, despite the fact that renewable electricity will be the cheapest form when it is available.

Another ever-present challenge in integration is who will bear the costs. Deeper integration could reduce electricity prices in the long term, but the upfront infrastructure costs are significant—estimated at 1.2 trillion euros by 2040 in the electricity sector alone. Compared to the previous 2021-2027 budget, the EU budget proposal for 2028-2034 increases spending on energy connection projects from 5.84 billion euros to 29.9 billion euros. The remaining costs will be borne by users of the electricity grid, as transmission system operators recover investment costs from their customers. However, exactly how these costs will be distributed among customers is an area of active policy and academic debate. A key question is the division of costs between countries that host infrastructure projects and those who stand to benefit from those projects. A free-rider problem can develop when countries benefit from their neighbors’ investments—through lower costs and greater resilience—without paying for them.

Conclusion

A unified energy market will require stronger governance. Coordination will be needed at the local, regional, national, and EU levels to close information gaps and create transparency, align policies and investments, set incentives, and build predictability and trust. The European Grids Package announced in December 2025 is designed to take on some of those challenges. EU Energy Commissioner Dan Jørgensen described the goals this way: “A truly interconnected and integrated energy system is the foundation of a strong and independent Europe. To achieve it, we need an energy infrastructure network of cables, pipes and grids that is up to date, fully interconnected, and that enables clean, affordable, homegrown energy to flow freely and securely to every corner of our Union.”

The sharpening geopolitical environment also continues to reinforce the importance of overcoming the barriers to European energy integration. In January, in a nod to the recent turmoil over the Trump administration’s threats to annex Greenland, a self-governing territory of his native Denmark, Jørgensen said, “We are not against trading with the US,” but “we are not aiming at replacing one dependency with a new dependency. We want to grow our own energy and our strategy in the future is to become free of gas.”

As Europe works to achieve its goals of increasing renewable energy and decreasing fossil fuel reliance, electricity integration becomes ever more important, allowing better adaptation to renewable intermittency, decreasing system costs, and increasing reliability. Integration also leaves room for individual countries to make their own choices about generation, meaning that policy preferences about nuclear energy, for instance, need not act as barriers to deeper integration.

Yet even though the economic benefits of integrating Europe’s internal energy supply are clear, European governments should not assume that external shocks and efforts by hostile powers at sabotage, pressure, and coercion will be enough to convince their citizens and their neighbors that this is not just another technocratic project. It would, in fact, be wise to embed mitigation of social and economic costs into energy integration policy from the beginning. Such an effort ought to be underpinned by a credible push for an across-the-board European competitiveness and growth strategy—as was recommended by Enrico Letta and Mario Draghi.

In Partnership With

Authors

Related Content

-

Acknowledgements and disclosures

The authors would like to thank Ryan Beane and Mathilda Silbiger for their research, graphics, and editorial support, Rachel Slattery for layout and graphics, and Adam Lammon and Ted Reinert for editing.

-

Footnotes

- This paper will therefore consider policy issues relating to the European Union, its member states, as well as membership candidates and non-candidate neighbors; the term “Europe” is used to refer to the continent as a whole as well as to the collective levels of governance therein.

- In 2023, the European Union imported 58% of its fuel (oil, natural gas, and coal), a level that has been largely consistent over the last 20 years. Key sources include the United States, Norway, Australia, Kazakhstan, Algeria, and the United Kingdom—plus Russia, albeit at a far lower level than before its full-scale invasion of Ukraine.

- Integrating a larger number of wind and solar installations in various locations is easier than integrating a single generator. Weather variability over distance is a friend of renewable power—sudden cloud cover or heavy wind in one place tends to balance out over larger areas. A mathematical description for this phenomenon is the theorem of large numbers, which states that the total result of a large number of uncertain processes becomes more predictable as the total number of processes increases.

- A virtual hub is not a physical location, but a point where transactions for natural gas are settled, based on the supply conditions and interconnections in that area. A good location for a hub has extensive supply and delivery connections and thus provides enough liquidity for robust price discovery. Northwestern Europe has pipeline supply and several LNG terminals, and is thus a good hub location, but points further away from the hub may experience different market conditions. The Netherlands’ TTF is considered the only mature natural gas trading hub in Europe.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).