The sanctions imposed on Russia are having a devastating effect on Russian financial markets. The ruble depreciated by 40 percent in the week leading up to March 1, and the central bank has doubled interest rates to 20 percent to support the currency. The stock market had to be closed after steep declines. The adverse effect of these sanctions on the Russian economy will build over time, despite Russia’s efforts to build a financial position resilient to external sanctions following those imposed after its annexation of Crimea in 2014.

This note describes the current structure of Russia’s external financial position and how it has evolved in recent years. Russia is better prepared for international sanctions than it was in 2014. However, the breadth and scope of the sanctions imposed in the past few days—which go much beyond those adopted eight years ago—will impose very severe costs on the Russian economy. In particular, sanctions that limit access to and use of foreign exchange reserves hamper the ability of the central bank to support the ruble and to provide foreign exchange liquidity to banks and corporations shut out from international capital markets.

Russia’s external position: increased financial autarky

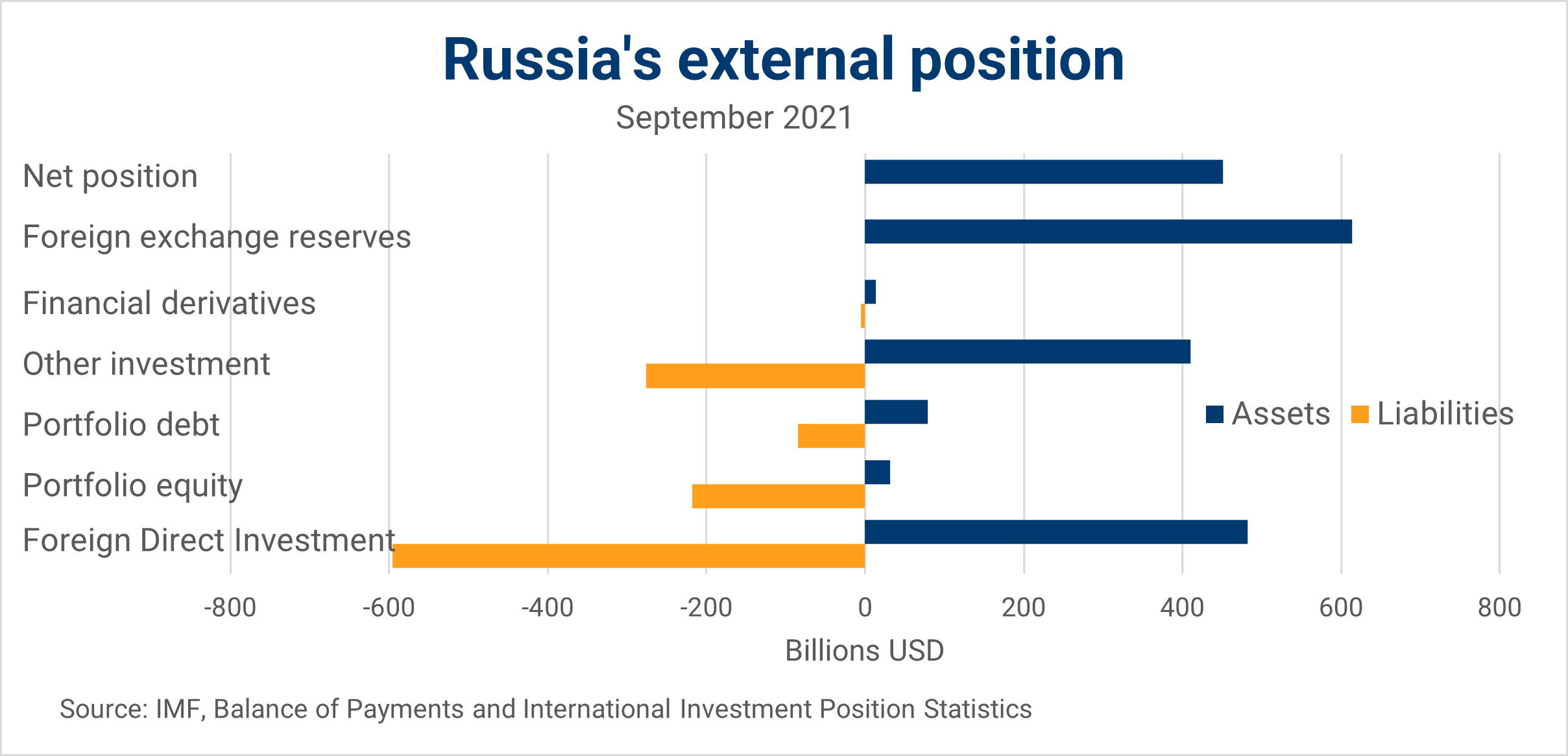

Russia is a net creditor on international markets: the value of its foreign assets exceeds the value of its foreign liabilities. Its total foreign assets at the end of September 2021—the latest date for which we have comprehensive measurement—amounted to $1.62 trillion against $1.18 trillion in foreign liabilities. The accumulation of net external assets was helped by rising oil and metals’ prices, which brought the current account surplus in 2021 to $120 billion, over 7 percent of GDP.

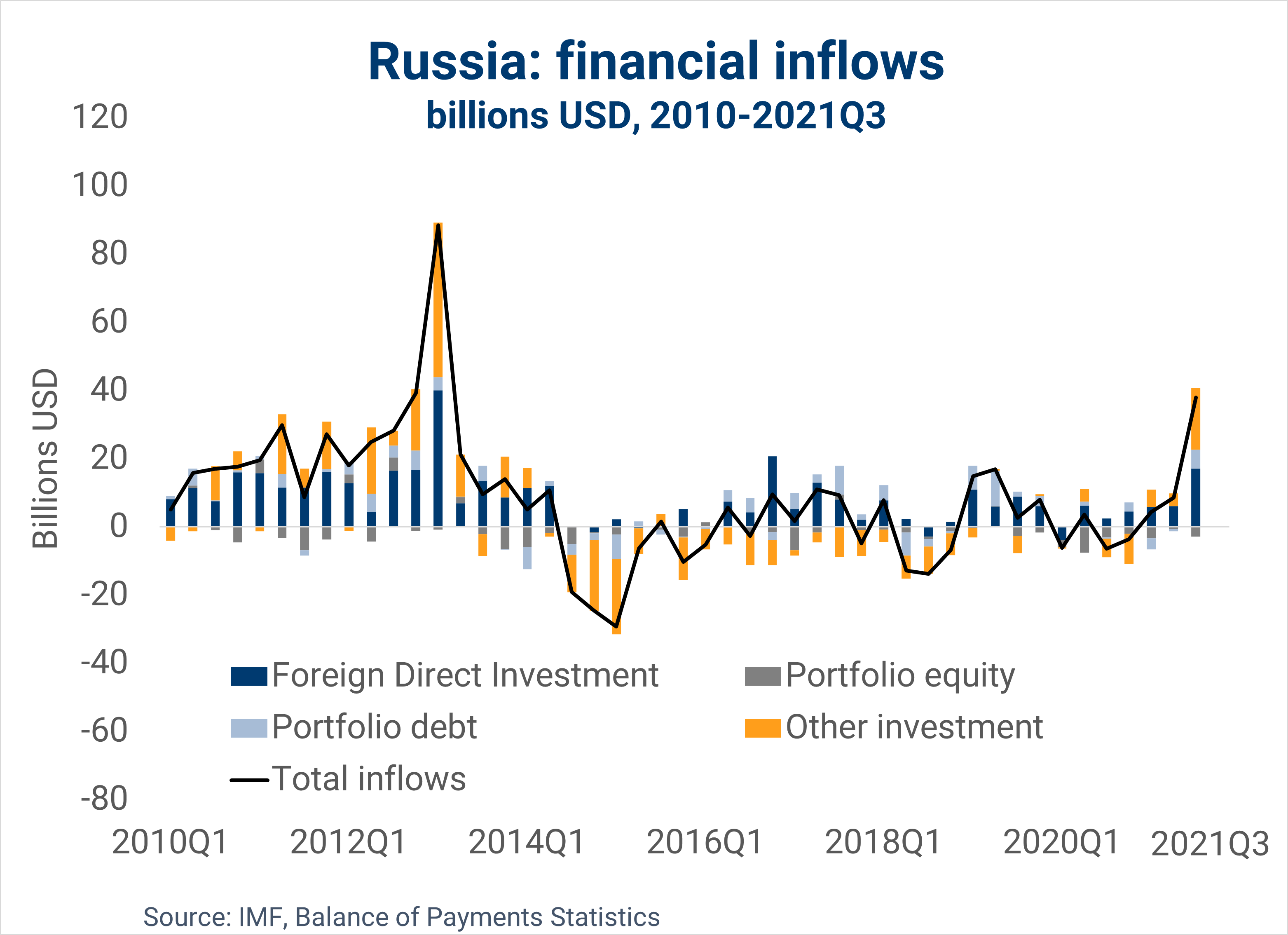

How did Russia accumulate this creditor position? The pattern of foreign capital flows to Russia changed sharply in 2014. Foreign capital left Russia, responding to the combined effect of sanctions imposed after the takeover of Crimea and much worsened macroeconomic prospects due to declining oil prices (see below chart). Foreign capital inflows have remained very modest since 2014, as the Russian economy moved towards increased financial autarky to reduce external vulnerabilities, including to financial sanctions. During this period Russia reduced its external debt by over $200 billion.

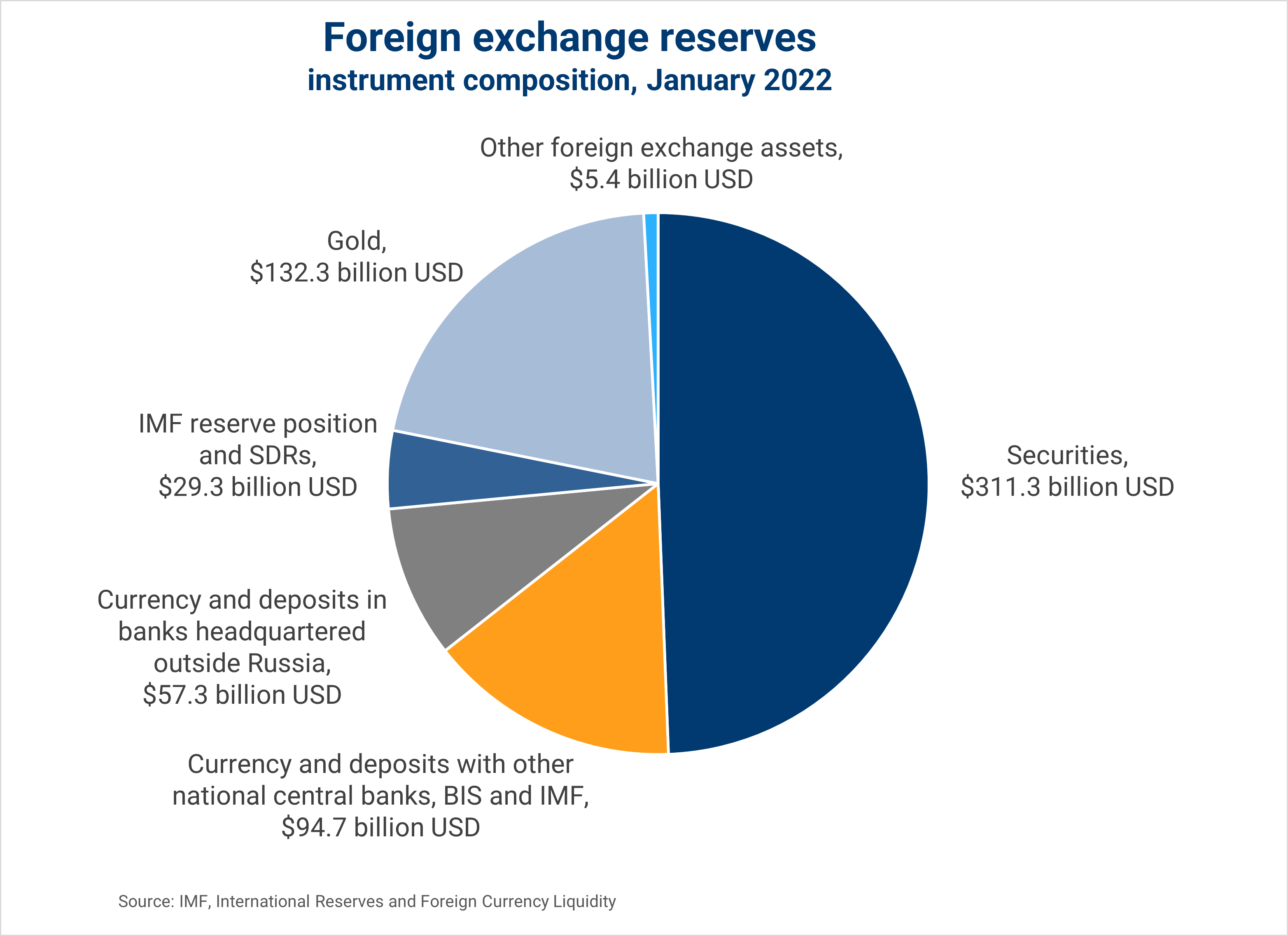

Acquisitions of foreign assets by the Russian private sector have remained subdued since 2014. However, the Central Bank of Russia accumulated substantial reserves (chart, light blue bars), more than offsetting the reserve losses it had incurred in 2014-15. Foreign exchange reserves exceeded $630 billion in January 2022—1.7 times the level of imports of goods and services.

Foreign exchange reserves

Reserves more than fully account for Russia’s net creditor position (see below chart). With most other external assets also denominated in foreign currency, the net creditor position in foreign-currency instruments is even larger—over $1.1 trillion. It is partly offset by a net debtor position in domestic-currency instruments of $700 billion, since most foreign direct investment and portfolio investment in Russia is denominated in rubles.

The foreign exchange reserves held by the Central Bank of Russia in January of this year comprised mainly $311 billion in debt securities, $95 billion in deposits with other national central banks and the Bank for International settlements (BIS), $57 billion in deposits in foreign banks, and gold ($130 billion) (see below chart).

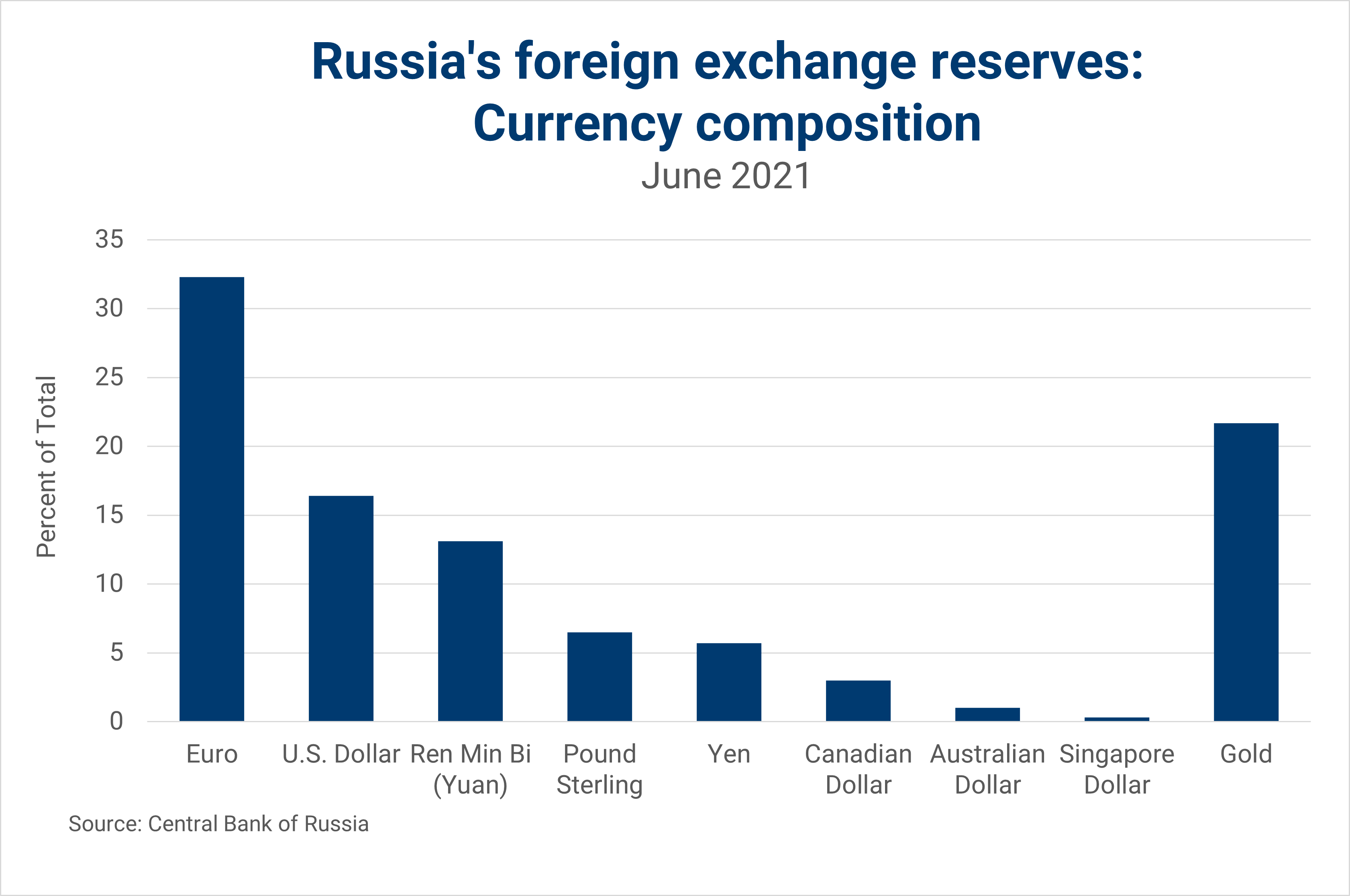

As for the currency composition (see below chart), over 30 percent are held in euro-denominated instruments, while the U.S. dollar’s share is half that level, much reduced from 46 percent at the end 2017.[1] The RMB share of reserves (13 percent, entirely built up since 2016), while much more elevated than for other major central banks, is still modest in comparison to G7 currencies. As discussed below, sanctions are limiting Russia’s ability to tap these reserves.

Russia’s other external assets and liabilities

The second largest category of Russia’s external assets is foreign direct investment (FDI) overseas (some $500 billion). However, it is difficult to establish where those holdings ultimately are—the main destination is Cyprus, a financial center used as an intermediate stop for investment ultimately destined elsewhere. It is therefore very hard to determine how vulnerable they might be to asset freezes or confiscation.

The other two categories of assets are portfolio investment (which covers ownership of equity shares and bonds) and “other investment” (consisting of loans, deposits, trade, credits, etc.). Other investment is the larger category (some $400 billion). About $150 billion are held by Russian banks while the remainder is mostly assets of nonfinancial corporations. Portfolio investment (some $100 billion) consist mostly of debt securities issued in financial centers such as Ireland, Luxembourg, and the UK (reported direct holdings in the U.S. were around $15 billion at end-2020, consisting mostly of shares).

On the liability side, the largest category is FDI (around $600 billion)—that is, foreign investment in Russia. As is the case for the asset side, the majority of FDI in Russia flows through financial centers, with Cyprus, Bermuda, and the Netherlands being the largest partners. The second-largest category of foreign investment in Russia is portfolio investment, with over $200 billion in equity securities and around $75 billion in government debt securities, mostly denominated in rubles. As of end-2020, these debt securities were held mostly by investors in Ireland and Luxembourg, with around $15 billion held by U.S. investors. U.S. investors’ holdings of Russian shares was much more substantial ($68 billion as of end 2021). Russian liabilities in the form of loans and deposits were around $275 billion, with nonfinancial corporations accounting for over half of the total.

Challenges in measuring positions and exposures

In all likelihood these data understate assets held abroad by Russian residents. The cumulative value of errors and omissions and “fictitious transactions/non-repatriation of export proceeds”—balance of payments items which capture unrecorded capital outflows—exceeds $500 billion over the past 25 years.[2] While identifying the owners of these assets is a daunting task, they are likely to be mostly in private hands and difficult to “tap” for the government in periods of need.

Also, a lot of Russian financial interactions with the rest of the world take place through entities domiciled in financial centers, rather than as direct links between entities resident in Russia and foreign investors. This complicates the analysis of Russia’s financial linkages with other countries, and hence the possible repercussions of financial sanctions. We have highlighted in the preceding paragraphs these financial center connections for FDI, where Cyprus is both the largest source and destination of Russian investment. Also, many Russian corporates raise funds through the issuance of debt securities overseas (with affiliates domiciled in Ireland, Luxembourg, the Netherlands). International securities issued offshore by Russian entities (such as Gazprom, major metal producers, major banks etc.) amount to close to $90 billion, and establishing the pattern of ownership of these bonds is much more difficult.[3]

The external positions and sanctions

With these considerations in mind, what could be the consequences for Russia of an exclusion of Russian entities from international capital markets? Bank for International Settlements data suggest that Russian banks are net creditors vis-à-vis the banks of other countries, while the nonfinancial sector in Russia is a net debtor to foreign banks. Still, as the experience of 2014 shows, both bank and nonbank entities losing access to international capital markets because of sanctions need to rely on foreign exchange liquidity support from the central bank to stave off default, as access to their assets overseas is restricted, maturing bonds are not rolled over, and lines of credit are withdrawn. Total external debt (the sum of portfolio debt liabilities, other investment liabilities, and the debt of Russian affiliates towards foreign parents in FDI relationships) is lower than in 2014 at $478 billion, roughly the size of reserves held in foreign exchange. As a mitigating factor, part of the debt—in particular most foreign-owned Russian government bonds—is denominated in rubles. Finally, energy prices are very elevated, boosting export revenues, which were instead falling rapidly in the second half of 2014 and in 2015.

However, the scope of financial sanctions is much broader than in 2014, especially the freezing of foreign exchange reserves held abroad. Curtailing Russia’s access to a sizable share of its foreign exchange reserves impairs the ability of the central bank to provide foreign-exchange liquidity to the private sector as it loses access to international capital markets, and substantially limits the capacity of the central bank to support the ruble. This is a major problem just when pressures on foreign exchange reserves mount as domestic residents demand foreign currency to hedge against currency depreciation. The sharp fall in the Russian currency, the resort to capital controls and to the forced repatriation of export proceeds, and the drastic increase in interest rates announced by the central bank at the end of February provide a vivid sense of the sanctions’ impact on Russian financial markets. A sharply depreciating currency will mean higher inflation and reduced standards of living. Further restrictions include the exclusion of (so far some) Russian banks from SWIFT, a messaging system underpinning a dominant share of cross-border bank transfers. This could further undermine Russia’s ability to conduct international trade by hampering trade settlements, even though sanctions so far have sought to limit the fallout for energy exports to the West, so as to limit spikes in already-high energy prices. A deep recession in Russia in 2022 looks inevitable.

[1] The share of reserves held in U.S. assets was even lower than the U.S. dollar share (below 8 percent). Other dollar-denominated assets held by the central bank include the dollar portion of IMF holdings (quota and SDRs) and dollar-denominated instruments issued by entities not domiciled in the U.S. Holdings of U.S. Treasury securities by Russian entities, including the central bank, exceeded $100 billion throughout 2017, but were then brought down to $15 billion by mid-2018, and further since then.

[2] Fictitious transactions/non-repatriation of export proceeds are “related to foreign trade in goods and services, securities trading, lending to nonresidents and fictitious transactions with money transfers to residents’ accounts abroad, which purpose is cross-border money transfer.”

[3] U.S. statistics on portfolio holdings on the basis of the nationality of the issuer suggest that as of end-2020, U.S. residents were holding some $6 billion in bonds issued offshore by Russian firms. The funds raised by issuing bonds offshore are typically channeled back to Russia through transactions between the offshore affiliate and the parent, which are recorded in the balance of payments as foreign direct investment in Russia.

The Brookings Institution is financed through the support of a diverse array of foundations, corporations, governments, individuals, as well as an endowment. A list of donors can be found in our annual reports published online here. The findings, interpretations, and conclusions in this report are solely those of its author(s) and are not influenced by any donation.

Author

-

Acknowledgements and disclosures

The author thanks Don Kohn & David Wessel for thoughtful comments, and Lorena Hernandez Barcena and Manuel Alcala Kovalski for assistance with the figures.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Russia’s external position: Does financial autarky protect against sanctions?

March 3, 2022