The COVID-19 crisis has had extraordinary effects on human mobility and short-term international migration flows. While at the beginning of March 2020 only 1 percent of the bilateral country-to-country travel corridors were affected by mobility restrictions, these are currently enforced in 43 percent of the routes. The effects that such travel obstacles may have on remittance activity are uncertain, since the reduction in migration flows has led to a decrease of potential remittance senders, but may have affected the remittance behavior of current migrants. The existing evidence on the consequences of the crisis for the size of the cash transfers sent by migrants is indeed mixed. In April 2020, the World Bank predicted a fall of around 20 percent in remittances worldwide for the past year. The World Bank’s forecasts for 2021 still reflect a volume of global remittances that is below that of 2019 by 14 percent. The experiences of individual countries in the past year have been very different: Many economies report a significant decrease in the inflow of remittances, while others, such as Pakistan or Bangladesh, saw an increase in the transfers from migrants.

Remittances contribute to socioeconomic development in several different ways, at the household, community, and national levels. In particular, their effect as a catalyst of poverty reduction is widely recognized. Goal 10 of the Sustainable Development Goals explicitly identifies remittances as an instrument to achieve economic development at the household and community levels in the receiving countries. Target 10.c of the Sustainable Development Goals aims at a reduction of transaction costs of migrant remittances to less than 3 percent and at the elimination of remittance corridors with costs higher than 5 percent. Achieving this target through the design of effective evidence-based policies that facilitate the reduction of the costs of remittances requires data on the particular locations of money transfer operators at a disaggregated level of spatial detail. On the one hand, such information is necessary to assess the degree of (spatial) competition taking place in the market for money transfers and thus explain differences in prices and transaction costs across and within countries. On the other hand, combining data on the geographical location of money transfer agents with population maps and other sources of geocoded information should help in the identification of potential undersupplied communities and infrastructure constraints to remittance activity.

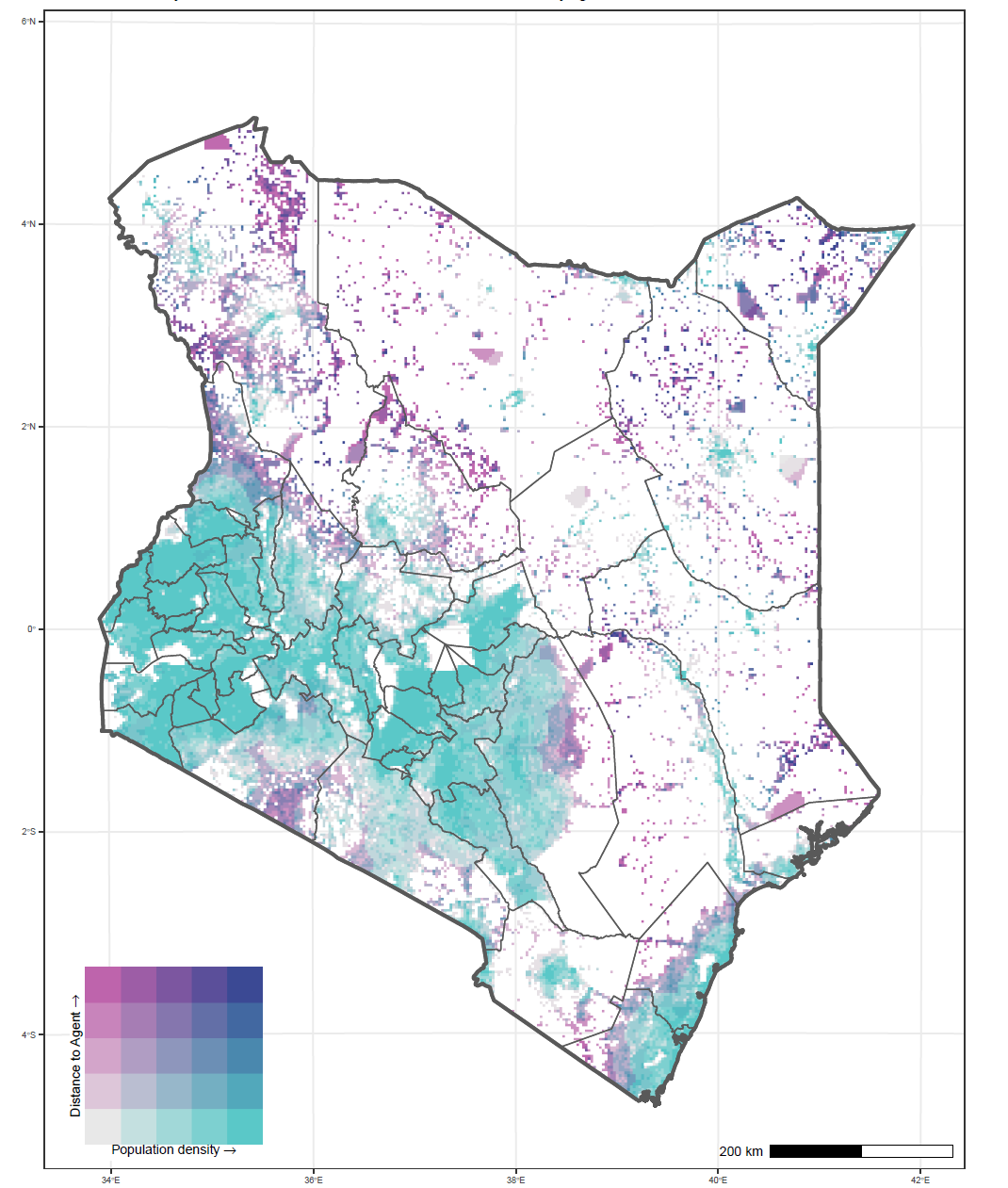

Such data were not existing until recently and now have been developed in the context of a partnership of researchers of the World Data Lab, the Vienna University of Economics and Business, and Developing Markets Associates with the European Union and the International Fund for Agricultural Development (IFAD) through the Financing Facilities for Remittances program (FFR). Using alternative data sources based on web scraping, information on the geographical location of money transfer agents was harvested and mapped in combination with geocoded population data for nine sub-Saharan African countries. The websites of prominent remittances service providers have the functionality to search for all money transfer agents and provide (imperfect) information about their location within a radius of a given geographical coordinate. Using hexagonal search grids over the area of the country of interest, the project resulted in new datasets of geocoded locations of money transfer agents on the African continent, which can then be combined with population density information (see Figure 1 for Kenya). This data reconstruction exercise allows us to identify undersupplied populations in terms of physical access to money agents and can be used to inform policies aimed at facilitating financial inclusion as an instrument to combat poverty. In Kenya, almost 13 million people, a quarter of the country, live more than 10 kilometers away from remittance service providers. These underserved parts of the population can be found everywhere in Kenya, especially in the north.

Figure 1. Central and Western Kenya are well served by money transfer agents

Source: World Data Lab estimates.

Note: Combination of the distance of each 3-km grid cell to the nearest money transfer agent location with geocoded population density. The color code depicts joint levels of population density and money transfer agent remoteness (see legend).

The access to financial infrastructure is a driving factor of cost reduction for both senders and receivers of remittances, and this effort has been enshrined in the fulfillment of Sustainable Development Goal (SDG) 10.c to help reduce the transaction costs of migrant remittances and eliminate remittance corridors. Current efforts to achieve this SDG face several challenges. Identifying populations at risk of financial exclusion is the first step toward designing efficient policies to increase the penetration of access points to receive cash in the subnational regions that require it. Reducing the costs of remittances should contribute significantly to achieving poverty reduction and empowering migrant workers as agents of change in local communities. The new developments in data science applications presented here can help boost financial inclusion and contribute to sustainable economic development on the African continent.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Modeling remittances flows with web scraping

February 26, 2021