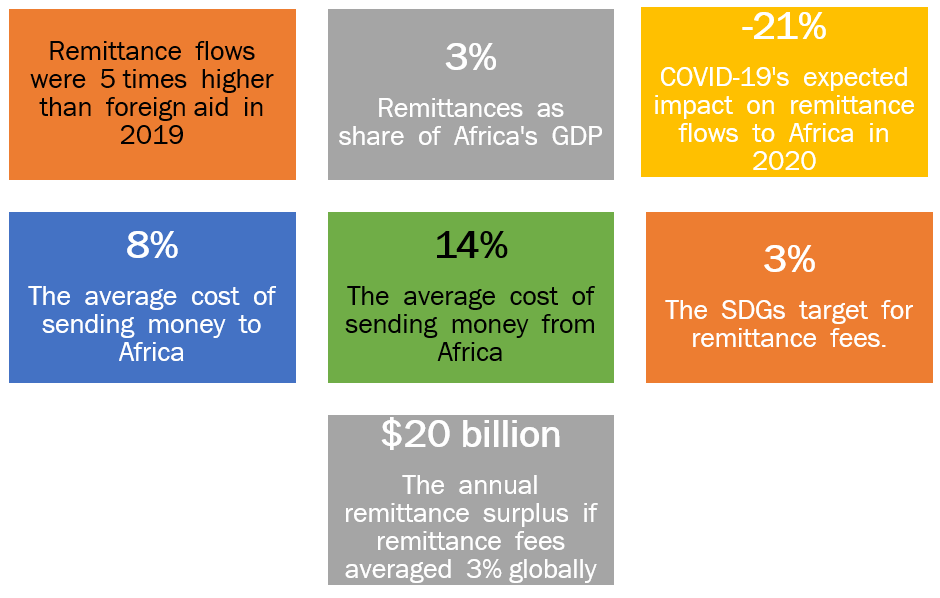

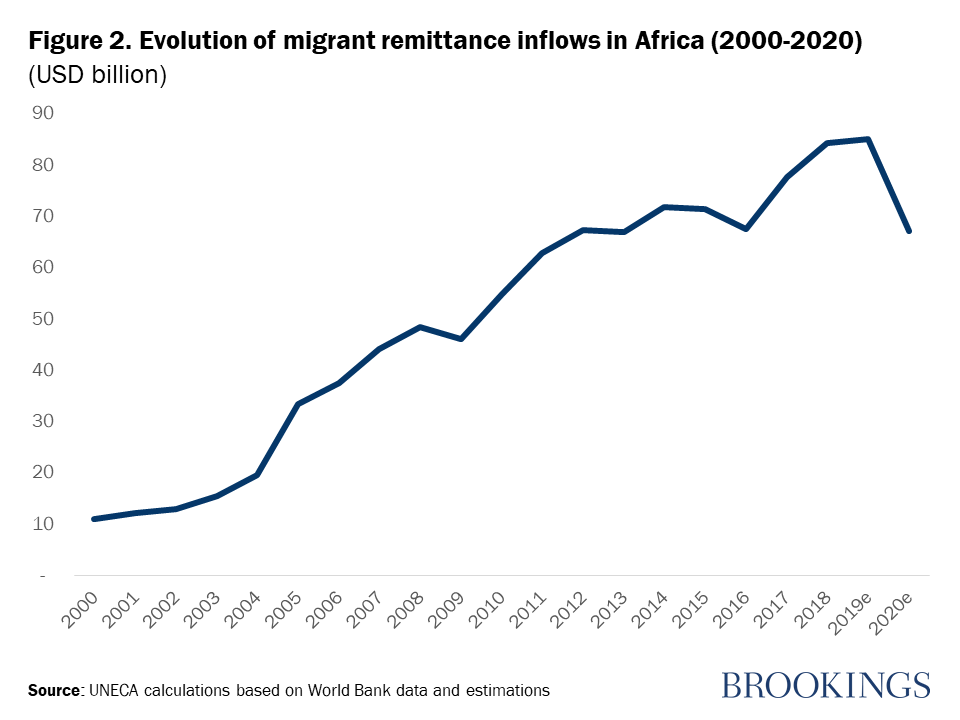

In Africa, 1 out of 5 people sends or receives international remittances. Since 2009, the flow of remittances to the continent has nearly doubled; they now comprise more than 5 percent of GDP in 15 African countries. In 2019, migrant workers sent about $85 billion to their relatives on the continent.

Worryingly, under COVID-19, precarious working conditions facing expatriates and operational difficulties facing remittance service providers (RSPs) have resulted in a major drop in this essential lifeline. In fact, remittance inflows to Africa are projected to decline by 21 percent—$18 billion in 2020. In comparison, global remittances to African countries fell by 5 percent during the global financial crisis of 2008. In short, the COVID-19 pandemic has wreaked generalized havoc with severe job losses by Africans in the diaspora, constraining their ability to remit funds to their home countries.

Figure 1. Global and African remittance flows: Key facts

COVID-19 has hit remittances hard

Indeed, COVID-19 is wreaking economic havoc around the world, and the fallout in Africa will be acute. Under the most optimistic scenario, the United Nations Economic Commission for Africa (UNECA) estimates that the continent’s economic growth could contract by 1.4 percentage points in 2020, pushing nearly 5 million people into extreme poverty. In Africa, remittance flows are expected to decline by 21 percent—reaching $67 billion in 2020, wiping out 6 years of progress (see Figure 2)—compared to East Asia and the Pacific (13 percent) or South Asia (22.1 percent).

For both remittances senders and recipients, COVID-19 has meant job losses and a decline in income. Since millions of vulnerable people use remittances to cover essential needs—it is estimated that three-quarters of the money is used to purchase nutritious food or fund health care, education, and housing expenses—the fallout of this trend could be devastating. Furthermore, around half of global remittances go to rural areas, where three-quarters of the world’s poor and food insecure live.

The challenge of high fees persists

Beyond loss of earnings, millions of senders also find it difficult to send money to their relatives during a lockdown. There are 1.7 billion unbanked adults globally, among which 75 percent have a mobile phone that could facilitate their access to financial services. Fintech companies, namely mobile operators, could help lower the remittances costs by facilitating access and speeding up clearing and settlement of the transactions.

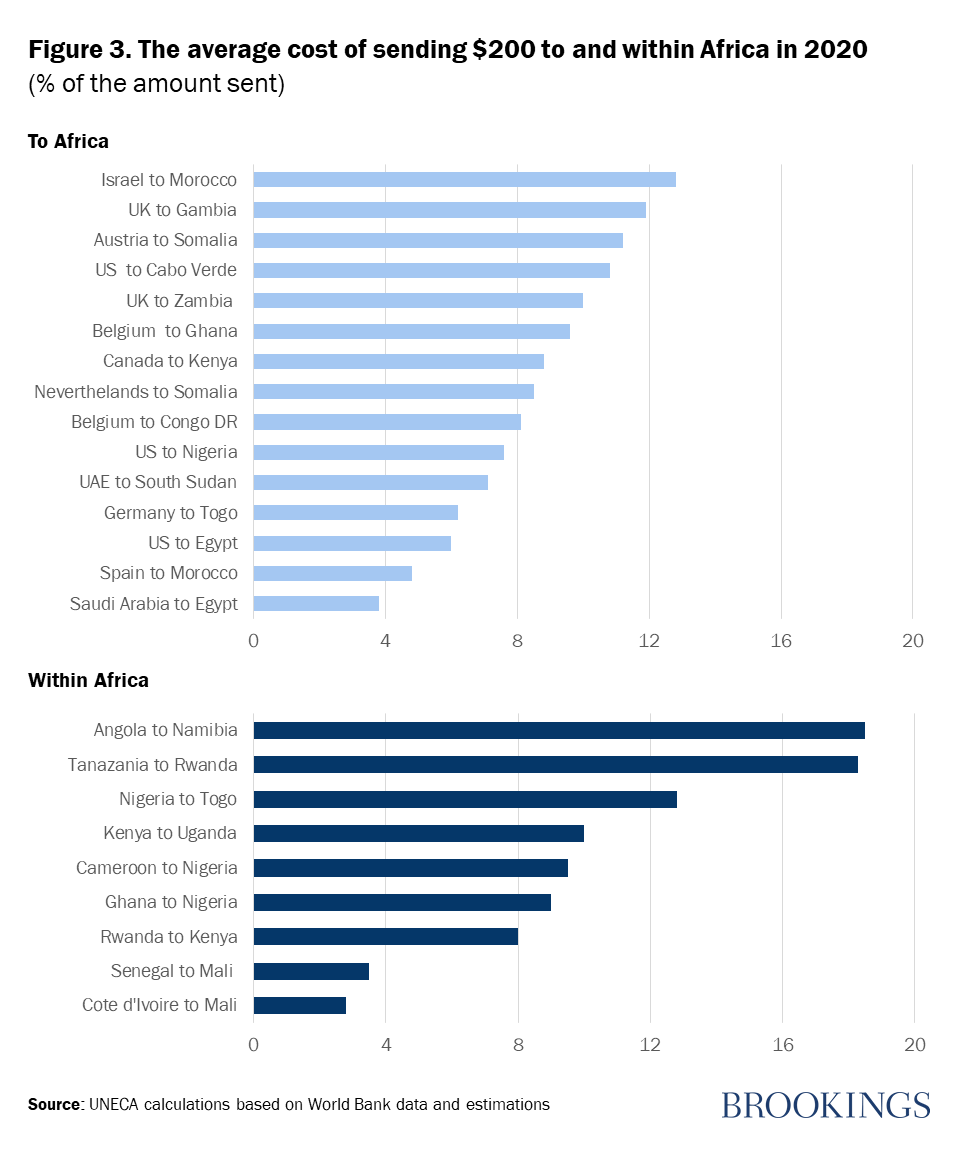

People living in poverty who rely on these payments already pay a premium. In fact, those sending remittances paid about $30 billion in fees globally in 2017. To send $200 to a family, the average migrant will pay $14 (7 percent) for the privilege. The more money you have, the less you pay; the global average of sending $500 is 5 percent. Banks charge the most at about 11 percent to send $200.

Worse, Africa, the region with the largest number of people living in poverty, is the most expensive region to receive remittances, at an average cost of 8 percent (South Asia has an average of 5 percent), though prices vary depending on the corridor. Similarly, the continent also has the highest cost of sending money at almost 14 percent (Figure 3). As they work to implement African Continental Free Trade Agreement (AfCFTA) and build their economies back better after the pandemic, African governments should incorporate strategies to considerably reduce the cost of sending cash.

Policies for boosting remittances

Some countries have rolled out support for families that typically rely on remittances, such as the Philippines, where remittances account for 10 percent of GDP. There, the government is providing cash assistance to over 1 million workers during the quarantine period, including migrant workers. Other countries have taken action to enable continued money flows. In Ghana, the government has lowered barriers to remittances, announcing that all mobile phone users could open accounts and transfer up to $170 daily without additional “Know Your Customer” documentation. In Uganda, telecom company MTN waived temporary fees on mobile money transfers.

The Kenyan Central Bank coordinated with private banks and rolled out a series of policy changes to preserve access to remittances, including waiving the typical fees assessed when transferring money from bank accounts to digital wallets, doubling the daily transaction limit, removing the cap on the number of transactions per month, and increasing the amount of money that can be kept in e-wallets.

The developed world has a part to play in supporting these lifelines too, including implementing the below recommendations, as we outline in our recent report “COVID-19 Remittances: Protecting an Economic Lifeline.”

- G-20 finance ministers should amend their national remittance plans, including bank regulations, to reduce costs of sending remittances to close to 0 percent until the pandemic ends, and thereafter ensure remittance costs do not exceed 3 percent, as stated in the Sustainable Development Goals.

- Governments should promote digitizing the remittance value chain from sender to receiver to help increase volumes, reduce costs, and enhance the convenience of sending money. Investing in innovation and reducing the digital gap is therefore decisive.

- Governments should offer tax incentives to remittance service providers for lowering fees and relaxing stringent “Know Your Customer” requirements for smaller transactions.

- All countries should include migrant workers in social protection and stimulus programs and extend visas so migrants can continue to work and send money home.

- Governments should ease regulations to classify money operators as essential businesses so they can remain in operation during COVID-related lockdowns.

- Governments in low- and middle-income countries should establish or complement appropriate safety nets for rural households that rely heavily on remittances.

African remittances have the potential to support African countries in mitigating the socioeconomic implications of COVID-19, as these remittances support strategic areas such as small and medium enterprise financing and building productive capacities, food systems, and the development of regional value chains, all of which encourage inclusive economic transformation.

Governments need to make remittances an essential component in their COVID-19 “build back better” strategies, as they represent an important source for financing development. Reduced remittance flows could exacerbate the current crisis, cutting poor people off from their primary lifeline. Conversely, facilitating remittance flows is one of the best ways to directly support people in need, provide an economic boost to countries, and thereby quicken an international recovery.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

COVID-19 and migrant remittances: Supporting this essential lifeline under threat

October 26, 2020