Content from the Brookings Institution India Center is now archived. After seven years of an impactful partnership, as of September 11, 2020, Brookings India is now the Centre for Social and Economic Progress, an independent public policy institution based in India.

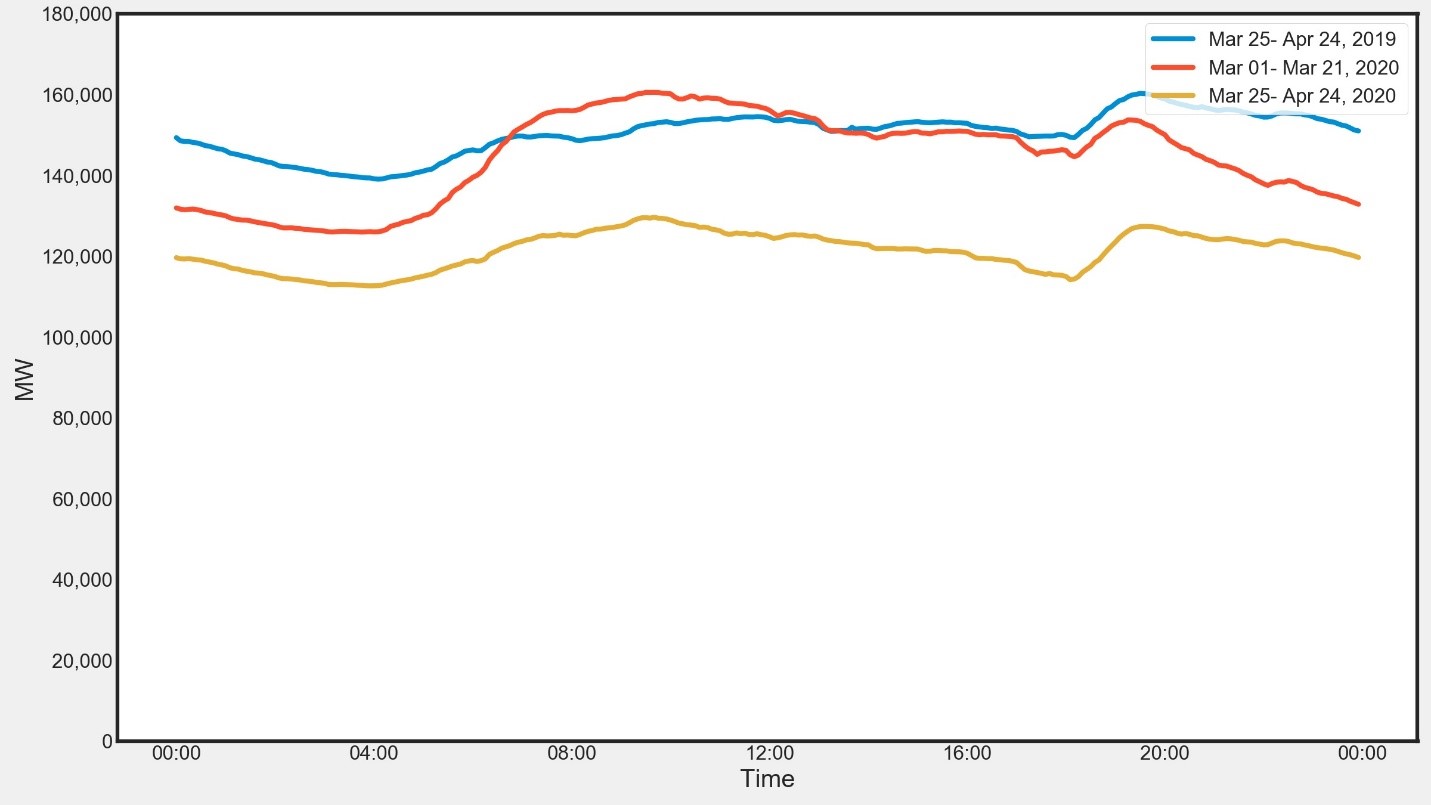

The arrival of COVID-19 in India led to a lockdown requiring 1.3 billion people to stay at home. Economic activity, at least in the first two versions of the lockdown, almost came to a standstill. By many standards, this was the world’s strictest lockdown. Total demand of grid electricity between March 25 and April 24 of this year sharply decreased by around 25% in comparison to the demand for the same period in the previous year. The electricity demand for this time period was 1,14,808 GWh in 2019 vs 85,994 GWh in 2020. Figure 1 below shows the average daily demand met curves for these periods. We see how the demand met has changed for the lockdown period, compared to earlier times.

Figure 1. Average daily Demand met curves

Lower emissions from lower coal use

On the supply side, the brunt of this fall in demand was almost entirely borne by the coal power plants, with the average coal generation decreasing to 86 GW between March 25 and April 24, 2020. On comparison with the last year for the same period, when the average coal generation was 116 GW, this accounts for a 29% decrease. The peak instantaneous coal generation in this period was 110 GW, in comparison to last year’s 132 GW. On the other hand, renewable energy (RE) being ‘must run’, it continued to run at full capacity (though there might have been marginal curtailment at noon). For balancing the RE, hydropower played an even more important role as the coal capacity online decreased. The lockdown, thus, gave us a glimpse of a high RE future, where hydropower will play a critical role (at least till cheap and scalable storage becomes commercially available). For the 9 minutes lights off event on April 5, hydropower again emerged as the primary resource for grid balancing. Hydropower’s role in these recent events has led to a renewed interest in it among scholars and the power industry.

With the decrease in coal generation, the carbon dioxide (CO2) emissions from electricity generation also decreased. The power sector CO2 emissions between March 25 and April 24, 2020 were 32% less than the same time period last year. Now, as demand as well as coal generation increase as the lockdowns have eased, there is an increase in emission levels.

With the ease in lockdown measures, demand has slowly increased from April to May. For May 2020, the highest instantaneous demand (measured as grid-level load met) was around 165 GW. Compared to May 2019, when the highest demand was 182 GW, this is a decrease of 17 GW. This figure however does not take into account the organic growth in demand each year. Assuming a conservative growth rate of 3%, this would roughly come to 5.4 GW. Thus, the peak demand right now is at least 22.4 GW lower than it would have been in a business-as-usual scenario. Almost all the incremental supply under lockdown is from coal.

Opportunity to clean up faster

To comply with the Ministry of Environment, Forest and Climate Change (MoEFCC) norms for coal power plant emissions, the retrofitting of Flue Gas Desulphurisation (FGD) systems in the coal power plants to decrease their Sulphur Oxides (SOx) emissions is scheduled to be largely concentrated for the years 2021 and 2022, with minimal retrofitting planned in 2020 and preceding years. However, given that the power demand is lower now, and plants are in shutdown, it would be possible for coal plants to undergo FGD upgrades now. Similarly, any Particulate Matter (PM), Nitrogen Oxides (NOx) and Electrostatic Precipitator (ESP) upgradation could be preponed with minimal disruption, compared to the earlier plan where retrofitting in the future could clash with growing demand. Stated another way, there is no reason to “take offline” plants per se – they’re already offline today.

COVID-19 came as a surprise and the measures taken by the government were sudden and much needed. However, the present first wave of COVID-19 in India might not be the last. There might be a second and/or a third wave as we have seen with previous global pandemics like the Spanish flu. This could again lead to lockdowns and a drop in electricity demand, further leading to coal plants decreasing their outputs and many shutting down. Any such lockdown period will be another important window for power plants to carry out FGD and other emission related upgrades. However, to achieve this would require agile planning as well as availability of capital to the generators, which has always been a challenge, more so during the present times. This process should also allow learning, both technological and in procurement. The latter, really, is the key to getting the private sector to be aggressive in pricing cheaper solutions – the crash in solar prices was largely driven by efforts on bidding.

India has had a very ambitious target for RE. However, with COVID-19 and the accompanying financial crunch, there might be a delay in that transition, leading to an increased dependence on coal (at least in the short term). In such a case, it becomes increasingly important that the FGD and other emission related upgrades are carried out at the earliest, and COVID-19 might just have provided the power sector with that opportunity.

Note– All calculations mentioned in the above piece are based on data from Carbontracker and might differ from the official data by a few percentage points. The Carbontracker and several related studies are supported by the Shakti Sustainable Energy Foundation.

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Is COVID-19 an opportunity to clean up India’s coal power plants faster?

June 15, 2020