Studies in this week’s Hutchins Roundup find that U.S. firms have sharply increased prices relative to costs in recent decades, oil price fluctuations have a persistent effect on core inflation, and more.

Want to receive the Hutchins Roundup as an email? Sign up here to get it in your inbox every Thursday.

Firms’ market power has increased dramatically over past 35 years

Jan De Loecker of Princeton and Jan Eeckhout from University College London find that U.S. firm market power—as measured by the markup of prices over costs—was roughly stable between 1950 and 1980, but has increased steadily since then, with markups increasing from 18% in 1980 to 67% in 2014. They find that most of this rise is attributable to an increase in the markups of the firms with the highest markups initially. This increase in market power, they argue, may help explain several macroeconomic trends, including the decline in the share of income attributed to labor, falling labor force participation, and the slowdown in output growth.

Oil price fluctuations have small but long-lasting effects on core inflation

Using a novel econometric approach, Cristina Conflitti of the Banca d’Italia and Matteo Luciani of the Federal Reserve Board examine the impact of oil price fluctuations on non-energy prices. They find that oil price changes have a small but persistent effect on core inflation (inflation excluding energy and food), contrary to the existing literature that finds no effect. In particular, they estimate that the plunge in oil prices from roughly $100 to $30 per barrel between July 2014 to February 2016 decreased core personal consumption expenditure (PCE) price inflation, the Fed’s favorite measure, by a quarter of a percentage point in 2015 and a third of a percentage point in 2016. The downward pressure is likely to persist until 2020, they conclude.

Inexperience with inflation targeting may explain weak effect of Japan’s monetary policy

In 2013, the Bank of Japan introduced a monetary policy approach that included inflation targeting and aggressive use of forward guidance, communications tools that attempt to change inflation expectations by announcing future monetary policy. Mark Gertler of NYU argues that these policies have been much less effective at increasing inflation than conventional macroeconomic models would predict. He attributes this failure to the fact that, in contrast to assumptions in most macro models, people’s expectations are influenced by not only policy announcements, but also past experience. His conclusion: unless an economy has a history of using an inflation target to anchor inflation, individuals must witness some inflation in order to believe that more is coming.

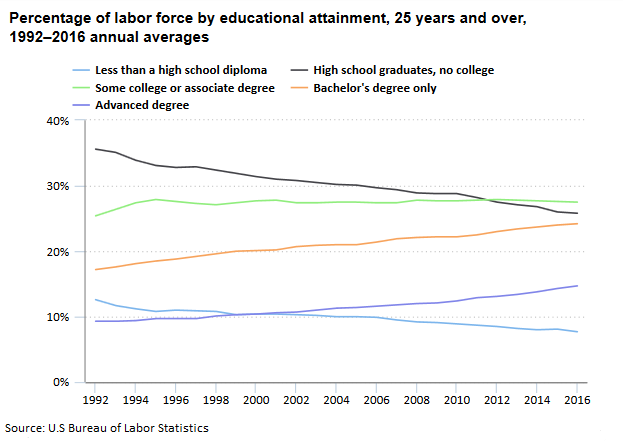

Chart of the week: U.S. labor force has become increasingly educated over the last 24 years

Quote of the Week:

“When the world changes as it did ten years ago, policies, especially monetary policy, need to be adjusted. Such an adjustment, never easy, requires unprejudiced, honest assessment of the new realities with clear eyes, unencumbered by the defense of previously held paradigms that have lost any explanatory power…” says ECB President Mario Draghi.

“[W]e must be aware of the gaps that still remain in our knowledge. Our mainstream macroeconomic models still have little to say, for instance, about the non-linear propagation of shocks, the distributional impacts of policies, or how endogenous firm entry and exit can affect economic performance. Policy actions undertaken in the last ten years in monetary policy and in regulation and supervision have made the world more resilient. But we should continue preparing for new challenges.”

Related Content

Related Books

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Hutchins Roundup: Increased price markups, oil prices and inflation, and more

August 24, 2017