Studies in this week’s Hutchins Roundup find that low-income people won’t purchase health insurance without very large subsidies, reduced regulatory oversight increases risky bank behavior, and more.

Want to receive the Hutchins Roundup as an email? Sign up here to get it in your inbox every Thursday.

Most low-income individuals are willing to pay at most half the cost of their health insurance

Using administrative data from Massachusetts’s health insurance exchange, Amy Finkelstein of MIT and Nathaniel Hendren and Mark Shepard from Harvard find that most low-income people will not purchase health insurance without extremely large subsidies. For example, they estimate that low-income people are willing to pay at most half the cost of their health insurance and that, even with a 90 percent subsidy, 20 percent of low-income people would remain uninsured. The authors suggest that the availability of uncompensated (free) healthcare likely reduces the value of being insured for low-income people. They conclude that modest enrollee premiums can be a major deterrent to universal coverage among low-income individuals.

Reduced regulatory oversight increases risky bank behavior

When the Federal Home Loan Bank moved its Ninth District headquarters from Little Rock to Dallas in 1983, most of the supervisors quit and it took years for normal supervision scrutiny to return. John Kandrac and Bernd Schlusche of the Federal Reserve Board find that this reduced oversight led savings and loans (S&Ls) in the district to take more risks than S&Ls in other regions that were subject to the same regulations. Specifically, Ninth District S&Ls increased risky real-estate investments as a share of all assets by 5 percentage points on average. “The shock to supervisory capacity and the subsequent expansion in risk-taking resulted in slower resolutions, more costly failures, and, ultimately, a higher incidence of failure,” the authors conclude.

Increasing minimum wage decreases machine-replaceable jobs and increases unemployment

Analyzing data from the Current Population Survey between 1980-2015, Grace Lordan of the London School of Economics and David Neumark of the University of California, Irvine, find evidence that low-skilled workers whose jobs are easily automated, particularly older workers in manufacturing, suffer when the minimum wage is raised. The authors find that a $1 increase in the minimum wage decreases the share of low-skilled workers whose jobs are easy to automate by 0.43 percentage point. Such a minimum wage increase also raises the unemployment rate for low-skilled workers in easily automated jobs by 0.12 percentage point.

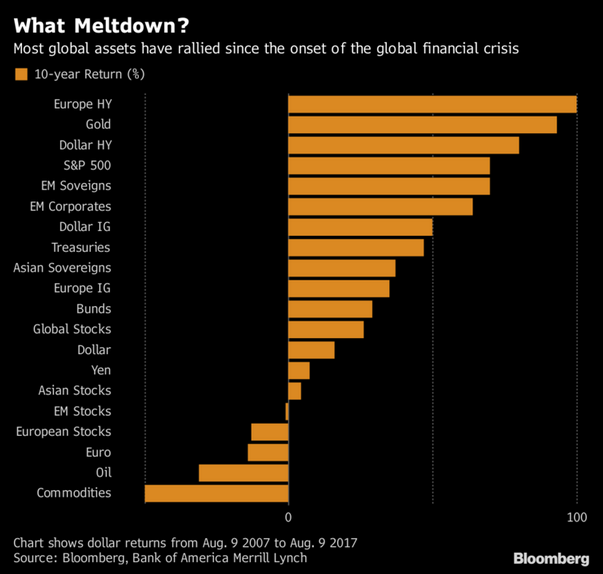

Chart of the Week: Junk bonds and gold have had a great decade

Quote of the week:

“It took almost 80 years after 1930 to have another financial crisis that could have been of that magnitude. And now after 10 years everybody wants to go back to a status quo before the great financial crisis. And I find that really extremely dangerous and extremely short-sighted,” says Fed Vice Chair Stanley Fischer.

“One can understand the political dynamics of this thing, but one cannot understand why grown intelligent people reach the conclusion that [you should] get rid of all the things you have put in place in the last 10 years…The Congress is very involved in these things and the pressure is on now to ease up. The pressure to ease up on small banks is fine with me. But the pressure I fear is coming to ease up on large banks strikes me as very, very dangerous.”

Related Content

Related Books

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Hutchins Roundup: Valuing health insurance, regulatory oversight and bank behavior, and more

August 17, 2017