Studies in this week’s Hutchins Roundup find that lower income students have limited access to colleges but have similar earnings as other students if they attend, LSAPs were more effective than forward guidance, and more.

Want to receive the Hutchins Roundup as an email? Sign up here to get it in your inbox every Thursday.

Lower-income students have less access to college, but have similar earnings if they attend

Examining college students from 1999-2013, Raj Chetty from Stanford and co-authors find that lower income students are much less likely to attend college than higher income students. For example, students in the top 1 percent of the income distribution are 77 times more likely to attend an Ivy League college than those who are in the bottom income quintile, they find. However, lower-income students who do attend college have similar earnings outcomes as their classmates, implying that colleges equalize opportunities for students of different socioeconomic backgrounds, they say. The authors point to certain mid-tier public colleges as having the largest effects on intergenerational income mobility, because these schools admit many low-income students and have good earnings outcomes.

Regional differences in house prices affect economy’s response to interest rates

Martin Beraja from Princeton and MIT and co-authors argue that the effectiveness of monetary policy depends on the regional distribution of housing equity. They find that, in the Great Recession, areas of the country with the largest house price declines and unemployment increases were the least responsive to interest rate reductions, because households in those regions were unlikely to have enough housing equity to refinance their mortgages. In contrast, in the 2001 recession, which had little effect on house prices, refinancing activity was strongest in high-unemployment regions. The authors conclude that monetary policy makers should track the regional distribution of housing equity over time in order to gauge the likely effectiveness of a given change in policy.

Unconventional monetary policy: LSAPs more effective than forward guidance

With the federal funds rate near zero following the global financial crisis, the Federal Reserve resorted to unconventional monetary policies: forward guidance (communicating future policies) and large-scale asset purchases or “LSAPS” (buying longer-term U.S. Treasury bonds and mortgage-backed securities). Eric Swanson from the University of California, Irvine disentangles the effects of these tools and finds that both had effects comparable in magnitude to traditional policies on medium-term Treasury yields, stock prices, and exchange rates. Forward guidance had larger effects on short-term Treasury yields, he finds, while LSAPs were more effective with longer-term Treasury yields and corporate bond yields. The effects of forward guidance were more transient than those of LSAPS, suggesting that LSAPs were a more effective policy tool than forward guidance, Swanson says.

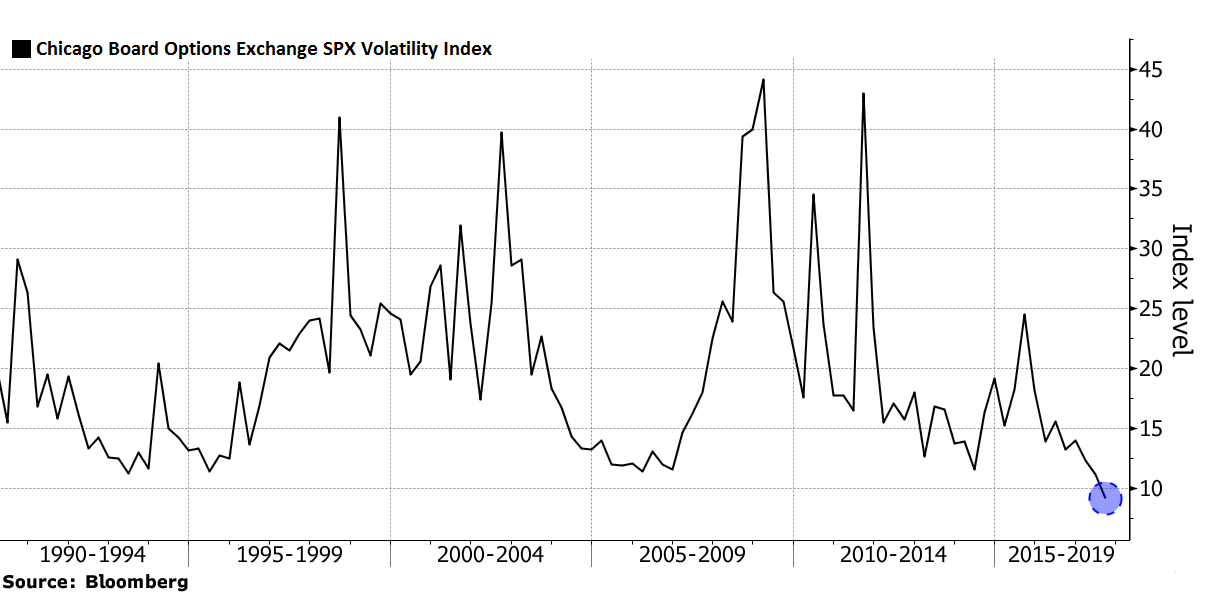

Chart of the week: Expectations of market volatility fall to an all-time low

Quote of the week:

“The persistent slow growth in wages is creating a challenge for central banks. It is contributing to an extended period of inflation below target. In years gone by, the more standard challenge was to keep wage growth in check, so as to stop upward pressure on inflation, which could lead to restrictive monetary policy. No advanced economy faces this challenge at present,” says Philip Lowe, Governor of the Reserve Bank of Australia.

“It is possible that things could change in the not too distant future, particularly in those countries at, or near, full employment. It may be that the lags are just a bit longer than usual. If so, we could hit a point at which workers, having had only modest pay increases for a run of years, decide that it is time for a catch-up. If such a tipping point were reached, inflation pressures could emerge quite quickly. In this scenario we could see a period of turbulence in financial markets, given that markets are pricing in little risk of future inflation.”

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Hutchins Roundup: Colleges and upward mobility, regional differences in monetary policy effectiveness, and more

July 27, 2017