Contents

- Introduction

- House prices are affordable to middle-income households in most U.S. neighborhoods

- Affordability is mostly a problem in large Northeastern and Western cities

- Premium for oceans, discount for Great Lakes

- Which communities have the largest share of “too cheap” neighborhoods? Which communities are “too expensive”?

- Policy implications

Housing costs are an immediate concern to many U.S. families and to policymakers. If people spend “too much” on housing (defined by HUD as more than 30 percent of their income), they may not be able to afford other necessities, such as food or health care. Cities and towns with high housing costs are particularly tough for young families, who tend to have lower incomes and wealth. Conversely, communities with unusually low housing prices can also be problematic, especially for long-term homeowners, who rely on housing wealth to pay for their children’s education or to supplement retirement savings.

Assessing whether housing costs are too high or too low is somewhat subjective. One shorthand measure is the ratio of house prices to household income: historically, U.S. median house prices have been roughly 2.5 to 4 times median income. (What price is “affordable” to a buyer with a given income depends partly on mortgage terms, such as the loan-to-value ratio, interest rate, and share of income spent on housing.)1

In this analysis, we investigate the distribution of neighborhood house price-to-income ratios across the U.S., focusing especially on locations with unusually high or low ratios.2 Both incomes and housing market fundamentals—such as land availability, development costs, wages, and demographics—vary by geography. This analysis helps identify regions of the country where house prices are “too high” and “too low,” where middle-income households have to stretch to buy homes, and where homeowners find it difficult to build housing wealth. Because housing prices vary substantially within as well as across metropolitan areas, the analysis focuses on price-income ratios at the neighborhood (census tract) level. This allows us to look for within-metro patterns; for instance, comparing neighborhoods in the urban core to those in suburban areas.

One important caveat: our analysis considers housing affordability primarily for families in the middle of the income distribution. Prior research shows that the poorest 20 percent of U.S. households have difficulty paying their rent without foregoing other necessities, regardless of where they live.

House prices are affordable to middle-income households in most U.S. neighborhoods

In the median U.S. neighborhood, house prices are approximately three times annual household income. This matches expectations about how much individual families can spend to buy a home without putting themselves in financial jeopardy. A majority of Americans live in neighborhoods where home price-income ratios are between 2.5 and 4 (Figure 1).3 Neighborhoods with headline-grabbing high price-income ratios are rare: about five percent of the nation’s neighborhoods have ratios above eight (the far right of the graph). Another five percent of neighborhoods have price-income ratios below 1.7 (the left tail).

Affordability is mostly a problem in large Northeastern and Western cities

Because housing markets are fundamentally local, the national statistics mask substantial variation across different parts of the U.S. Almost all Southern and Midwestern households live in affordable neighborhoods, while large shares of Northeastern and Western neighborhoods have price-income ratios that would stretch middle-income family budgets (Figure 2). The South and West have larger shares of neighborhoods with unusually low price-income ratios, places where owning a home is unlikely to result in building wealth.

Housing affordability also varies across cities, suburbs, small towns, and rural areas (Figure 3).4 Highly unaffordable neighborhoods are most concentrated in the urban core of large metropolitan areas. Urban centers tend to have a highly diverse housing stock, with buildings of different ages, sizes, and architectural styles. Cities also have a wide range of incomes, with very poor and very wealthy families often living in close proximity. Both of these trends combine to give urban neighborhoods a wide dispersion of housing price-income ratios, with greater concentration of neighborhoods at both the high and low end of the distribution. Suburbs of large metropolitan areas—where the majority of U.S. families live—have lower average price-income ratios, as well as fewer neighborhoods with outlying ratios. The distribution of price-income ratios is narrowest for neighborhoods outside metropolitan areas (small towns and rural areas). Non-metropolitan areas also have the largest share of neighborhoods with unusually low price-income ratios.

Premium for oceans, discount for Great Lakes

Urban economists and real estate agents have long known that people will pay a premium for locations with special amenities, such as nice weather or scenic views. Proximity to large bodies of water offers both outdoor recreation and pretty scenery. Consistent with predictions, metro areas near saltwater coasts—the Atlantic and Pacific Oceans and the Gulf of Mexico—have higher price-income ratios.5 However, metro areas around the Great Lakes (“freshwater”) have somewhat lower neighborhood price-income ratios than either saltwater coasts or inland regions. (Note that the analysis compares all neighborhoods within water-adjacent metro areas to all neighborhoods in inland regions, rather than comparing neighborhoods at different distance to water within the same metro area.) Saltwater coastal metros have higher price-income ratios relative to inland or freshwater areas within census regions as well.

Which communities have the largest share of “too cheap” neighborhoods? Which communities are “too expensive”?

Neighborhoods with persistently low home price-income ratios raise concerns about the ability of families to build wealth because home equity is the main source of wealth for middle-income families. Notably, disparate rates of return on homeownership contribute to the racial wealth gap.

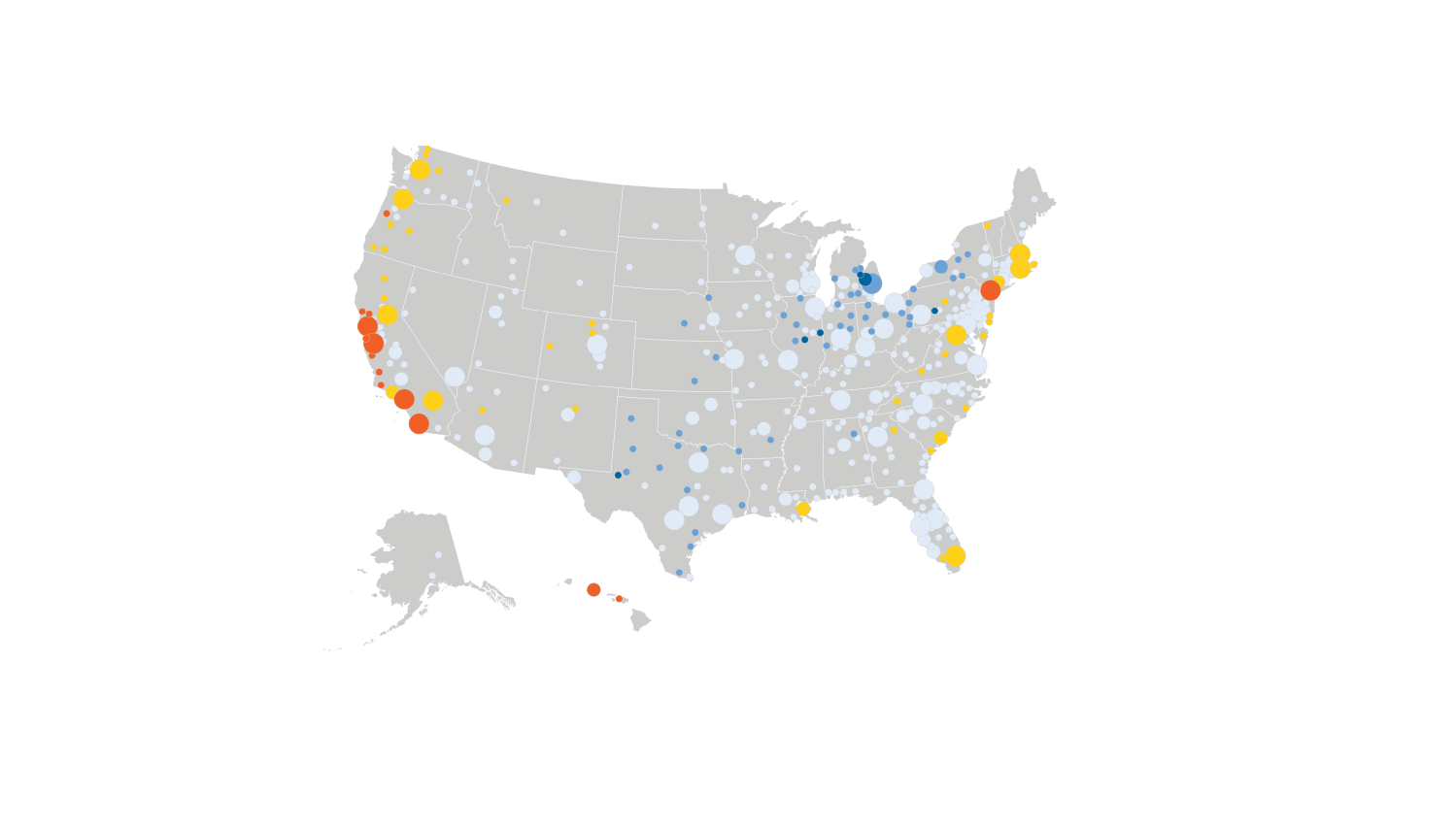

Metropolitan areas with low price-income ratios are located in very different parts of the country from high-priced metropolitan areas (Figure 5). The lowest ratio metros are mostly located in the Midwest, especially clustered around the Great Lakes, and scattered across Texas. The metros with the highest ratios are primarily along the Pacific and Northeast Atlantic coasts. South Florida, Colorado, and several smaller metros along the Southeast coast also rank among the most expensive areas. Across the U.S., most states have more metro areas with price-income ratios in the normal range (2.4-4.3) than metros with outlying values.

An alternative way to think about “cheap” versus “expensive” metros is to calculate the share of neighborhoods within each metro that have unusually high or low price-income ratios. This metric is useful because two metros could have similar average price-income ratios but different shares of low- and high-value neighborhoods. As has been widely covered by the media, Californian and Hawaiian communities stand out for having the largest shares of “too expensive” neighborhoods. By contrast, the five metro areas with the largest shares of “too cheap” neighborhoods are located in Illinois, Michigan, and Pennsylvania (Table 1)—a geographic pattern that has received less media attention. Large cities such as Flint, Mich. and Los Angeles have many neighborhoods with extreme price-income ratios, but some mid-sized and smaller communities, such as Danville, Ill. and Santa Cruz, Calif., share that characteristic. The overall price-income ratio and the share of tracts with low, middle, and high price-income ratios for all metros in this analysis are available in the downloadable appendix tables.

Policy implications

The spatial patterns of house price-income ratios suggest three avenues of improvement for policy—and highlights the need for coordination across different levels of government.

Public policies should not favor homeownership over other means of wealth building. Heartland cities and small towns have seen largely flat or falling real housing prices: this makes them affordable places to buy a home, but also means they are challenging places to build wealth through homeownership. As we saw during the Great Recession, low housing prices can trap families in place if they owe more on their mortgages than potential sale price of home. In low-priced areas, even families that have paid down their mortgages find it difficult to build wealth. That makes it harder for them to supplement retirement savings or borrow against home equity for their kids’ education. Federal tax policies that strongly favor owner-occupied homes over other asset types are not well suited to support middle-class wealth building in lower-price locations.

Housing unaffordability for middle-income households is a regional rather than a national problem. Nearly all communities have some neighborhoods that will be out of reach for middle-income families—the “nicest” neighborhood in town. But in most communities, middle-income households can still afford to buy a home in a reasonably wide range of neighborhoods. Because the problem is mostly regional, responsibility for policy solutions rests primarily with state and local governments.

Local governments broke their own housing markets, and they will have to fix them. Evidence suggests that in many of the Northeastern and Western communities where price-income ratios are highest, those high housing prices result from excessive land use regulation—that is, from policy choices of local governments. Making housing more affordable to middle-income families requires those same governments to revise their zoning and allow more housing to be built, especially near jobs and transportation. States can encourage better local regulation through carrots and sticks, if they figure out the politics. At the federal level, HUD could more effectively use its bully pulpit to call out communities that obstruct new housing, and share information on how to build housing more cheaply.

Future articles will explore in more detail how federal, state, and local agencies can each contribute to better-functioning housing markets.

Related Content

Authors

-

Footnotes

- Standard assumptions used in the literature are that a buyer will spend 30% of income on principal, interest, taxes and insurance and make a 20% downpayment. Interest rates have been at historic lows for the past decade, allowing buyers to purchase homes at higher multiples of their income. Varying these three parameters – income spent on housing, LTV, and interest rate – gives a range of possible price-income ratios for between 2.6 and 5.3.

- House prices are estimated using value of owner-occupied homes from the ACS. Although self-reported housing values often differ from observed sales prices, tract-level data from actual transactions are not available.

- We use Census tracts as a proxy for neighborhoods, and we exclude tracts where fewer than 10 percent of housing units are owner-occupied.

- We define urban Census tracts as those that fall inside the first-named city in the official title of one of the nation’s most populous 100 metropolitan areas, or any other city in the title that has a population of at least 100,000. We classify all other Census tracts in the largest 100 metro areas as suburban, and Census tracts in other metropolitan areas as small metro. Lastly, we classify Census tracts that do not fall inside any metro area as rural.

- Metropolitan areas are defined as “saltwater” if the centroid is within 75 miles of the Atlantic or Pacific Oceans or the Gulf of Mexico. Metropolitan areas within 75 miles of a Great Lake are defined as “freshwater.” All remaining metropolitan areas are defined as “inland.” Tracts outside metropolitan areas are not categorized.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).