When the world begins to emerge from the COVID-19 crisis, it will be saddled with social and economic challenges of an immense scale. In this policy brief, we recommend the use of outcome-based or pay for success financing—including social and development impact bonds (SIBs and DIBs)—to spur renewal and prosperity by crowding-in private funding, focusing existing resources on outcomes, reducing government risk, and strengthening systems of social service delivery. Since in an impact bond, private investors provide upfront financing that the government or other funder only repays (plus returns) if the social service program is successful, the mechanism represents an opportunity to inject new, private or philanthropic funds into public service financing during crisis recovery. Most impact bond contracts are at least three to five years long, which allow governments or other entities time before making payments and then, only if the intervention has delivered results. Furthermore, as impact bonds are used to finance social services, such as employment and job training (or retraining), homelessness, and education, they can contribute directly to economic recovery in the areas hardest hit by the pandemic. This puts the government in a better position to have more funding available when the time for repayment comes around, as people get back on their feet and tax revenue bases increase. In addition, as the country and the rest of the world looks to rebuild, this innovative tool could strengthen entire systems of social services by incentivizing collaboration, improving monitoring and evaluation, and driving adaptive management. Finally, impact bonds and other forms of outcome-based financing provide an opportunity to focus relief measures on marginalized populations, including through added incentive payments.

In this brief, we describe the impact bonds model, explain why it could be particularly well suited at this time, and suggest concrete policy measures that would expand outcome-based financing for social services and environmental challenges. In the domestic context, use of this instrument could be increased by municipal and state governments and supported by federal agencies (e.g., the departments of Health and Human Services and Education) as well as through a dedicated office of innovation in the White House. Globally, the tool could support development aid through agencies such as the U.S. Agency for International Development (USAID), and through U.S. support of multilateral aid. While we provide recommendations to the new Biden administration, our suggestions also extend to other countries and international institutions with the hope of renewal and prosperity for the entire globe after this devastating crisis.

Challenge

Progress is stagnating to achieving social and environmental goals. The joint efforts of government, nongovernmental, multilateral, and philanthropic organizations around the world—mobilized through and alongside the Sustainable Development Goals (SDGs)—has resulted in unprecedented global progress in ending extreme poverty, reducing inequality, and promoting environmental sustainability. Although governments around the world have long invested resources to address national priorities for improving health, economic, education, and environmental outcomes, the increased global attention and financial resources committed to addressing these issues over the recent decades have helped to accelerate progress in many dimensions. For instance, global under-5 mortality has more than halved over the past three decades. Yet, despite the progress achieved, many people have been left behind, especially those from marginalized communities. In 2019, over 5 million children died from mostly preventable and treatable causes. In the U.S. in 2019, 10.5 percent of families were below the poverty line before the pandemic, 57 percent of which were families of color. Moreover, socioeconomic and social divides are further magnified by communities’ unequal access to environmental and health resources, including safe water, green spaces, and climate change mitigation infrastructure.

The COVID-19 pandemic is exacerbating inequalities. The current pandemic has exacerbated existing social challenges, and the world’s poorest and most marginalized populations have been the hardest hit. For example, the health and safety measures and social distancing requirements put in place to help slow the spread of the pandemic have constrained capacity and disrupted delivery of essential health and education services. For instance, according to an April 2020 study, less than a quarter of students in low-income settings had access to remote learning, as compared to 90 percent in high-income settings since schools closed. In the United States, 8 percent of households with students (4.4 million households) lack consistent access to a computer and 3.7 million lack internet access. Lack of access to high-quality remote learning is tied directly to learning loss. On the jobs front, the number of employed persons and hours worked declined steeply across countries, ranging from a staggering 46 percent decline in hours worked in Mexico to a still high rate of 10 percent fewer hours worked in Australia. In December 2020, the United States economy lost 140,000 jobs—all of them were held by women.

Funding for social services and the environment is scarce. Although the SDG global framework has helped to mobilize important resources, social and environmental services have long faced funding challenges, which are critical to improving and expanding delivery to harder-to-reach populations and improving outcomes. In the U.S., it is estimated that it would cost another $111 billion, in addition to the $29 billion already spent per year to provide universal access to early childhood development. Globally, the financing gap to achieve the SDGs has been estimated at an annual $2.5 trillion, and this problem has only gotten worse with the havoc that the pandemic has wreaked on global economies and tax bases. In the United States, state and local government revenues are projected to decline by $167 billion in 2021 and $145 billion in 2022—about 5.7 percent and 4.7 percent, respectively. The current global crisis necessitates dramatic expansion in public services to respond to the growing needs of individuals, however the ability of government to do so is increasingly limited as a result of the pandemic’s negative effects on already lean social service budgets. In the short to medium term, the economic impacts of the pandemic may incentivize short-termism among governments as they seek to recover quickly, which may shift funding away from social and environmental sectors and risk dialing back progress in improving social and environmental outcomes.

Failures to achieve prosperity for millions of citizens around the globe has caused policymakers and funders to seek innovative ways to tackle intractable social challenges, and pandemic recovery efforts necessitate them even more. Governments must innovate to provide sufficient social services and create enabling environments for improved social outcomes.

Limits of historic and existing policies

Historical funding of social services

The government plays a critical role in ensuring that all citizens—regardless of circumstance—receive the basic services necessary to live healthy, safe, and productive lives, and now its role is more central than ever. While the way in which governments fund and deliver these services has varied historically over time , this has often been via public-private partnerships with private organizations, often nonprofits. In fiscal year 2019, for example, the U.S. Department of Health and Human Services contracted $26.5 billion worth of services from independent organizations. Such funding can sometimes be in the form of grants; however, most often the government contracts with the nonprofit sector using fee-for-service and fixed-cost contracts.

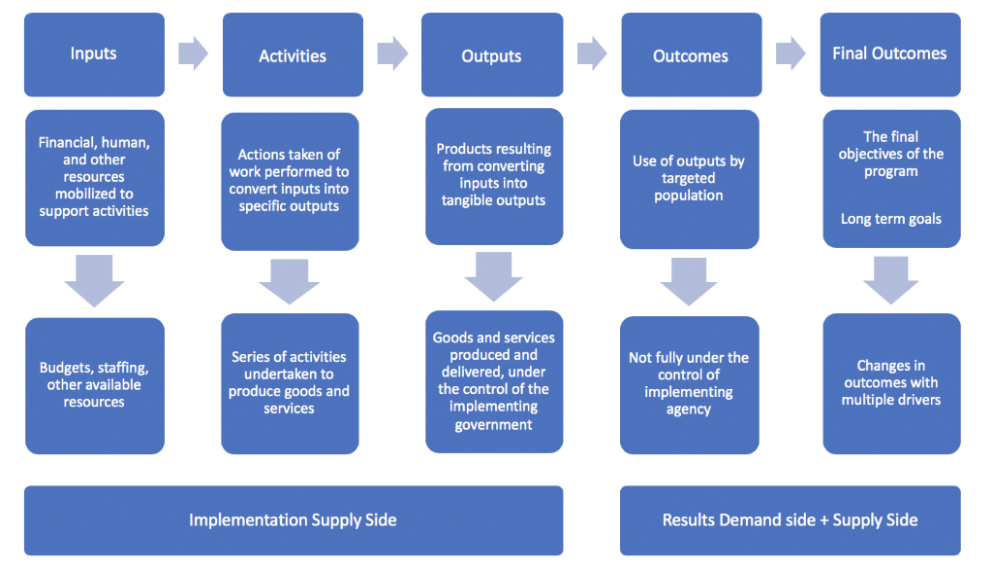

Traditionally, fee-for-service and fixed-cost contracting tie service provider payments to “inputs” or “activities,” based on a logic model or theory of change which proposes that those inputs and activities will lead to stated outputs, outcomes, and impact (see Figure 1). However, the outcomes and impact are not guaranteed to stem from the specific inputs, and therefore are not guaranteed to be achieved through the program.

Figure 1. The results chain

Source: Adapted from Gertler et al. 2016

The impact bonds model

Given the failure of many social programs funded through input- and activity-driven contracts to deliver the intended outcomes, the past two decades have seen a push toward contracts that provide incentives to deliver measurable results. These types of contracts—termed broadly results-based financing contracts—make payments contingent on the achievement of results. However, there are two challenges with some of the more basic results-based financing structures. First, results have often been measured in terms of outputs, which fall short of demonstrating outcomes and actual positive impact for beneficiaries. Second, more traditional results-based contracts typically require services be provided (and paid for) upfront, with governments or other funding entities only reimbursing the costs following completion of the program, and only if results are achieved. In public-private partnerships, which fund most social services through nonprofits, many organizations do not have the capital to forward-fund social service programs for several years, nor can they afford to take on the performance risk of an intervention which may not yield results, and therefore reimbursement. Impact bonds, a relatively new form of results-based financing, have shifted the focus further from outputs to outcomes (as do all forms of outcome-based financing), and have addressed the second challenge through the introduction of private investment capital.

In an impact bond, private investors (often impact investors) provide upfront capital for social services and are repaid by an outcome funder contingent on the achievement of agreed-upon results (see Figure 2). In a SIB, also called pay-for-success (PFS) in the United States and social benefit bonds (SBB) in Australia, the outcome funder is a government entity. In a DIB, this is usually a third party such as a donor—for example, USAID or a foundation—and is used primarily, though not exclusively, in low- or middle-income countries. A third type, environmental impact bonds (EIBs), which focus on environmental challenges, have thus far only seen governments as outcome funders but could theoretically also involve third-party payors. In addition, a few variations on the model, as well as tools to expand the model, have also come about in recent years; for example, investment funds and outcomes funds serve to scale the impact bond model by pooling investment capital and outcome funding respectively for outcome-based financing.

Figure 2. Impact bond mechanics

Because there is a cost to upfront capital and risk transfer, investors in an impact bond are eligible for a return on this investment. The achievement of outcomes—and level of that achievement—determines whether and how much of the principal investment and potential returns outcome funders pay out to investors, with more or better outcomes often resulting in a higher investment return. The expectation is that projects structured through impact bonds can achieve more or better social outcomes due to the hyper-focus on outcomes, the upfront capital investment, and engagement by investors, which allow for flexibility and innovation, as well as overall additional scrutiny on the project. In high-income countries, this is attractive to governments not only due to the outcome achievement but also due to the potential future cost savings provided by successful preventive interventions, which lead to lower usage or need for costly remedial services. In developing country contexts—and particularly in DIBs, in which the outcome payer is not the government—quantifying the value of interventions to each organization is much more complicated, and in these cases future savings are less likely to be at the fore.

|

Box 1. The landscape of impact bonds

According to the Brookings Global Impact Bond database, as of January 2021, over 200 impact bonds have been contracted in 35 countries, with about a quarter of these completed. The vast majority contracted are SIBs, and only 13 are DIBs. Globally, the key sectors are social welfare (70) and employment (64), and nearly 2 million total beneficiaries are served.

In the United States, 27 impact bonds have been launched in 14 states and the District of Columbia, with California, Colorado, and Massachusetts leading the way with four projects each. Over 750,000 Americans have benefited from impact bonds addressing issues ranging from homelessness to improving child welfare to reducing prison recidivism. Most recently, the cities of Atlanta and Washington, D.C. have launched EIBs, aimed at addressing environmental concerns in their cities and financing green infrastructure projects. |

Policy recommendations

In short, governments can no longer afford to fund programs that don’t yield positive outcomes for disadvantaged citizens, and that fail to serve all citizens equitably. Furthermore, the limited funding available to support low- and middle-income countries, which will suffer greatly from the global pandemic, must be spent wisely. Outcome-based or pay for success financing—including impact bonds— is a way to shift the focus from inputs to outcomes, strengthen entire systems of service delivery, and focus on hard-to-reach populations and environmental challenges. While impact bonds have now been contracted in over 35 countries, including 27 projects in the U.S., the market remains quite small (see Box 1). Where appropriate, federal, state, and local agencies should make a concerted effort to shift from the antiquated model of input-based funding toward paying for successful achievement of outcomes. The private sector and philanthropies can support this outcome-based financing model, which offers not only an opportunity for greater impact, financial returns, and system strengthening, but also the ability to recycle investments into further social good. Finally, multilateral and bilateral development agencies, including USAID, should concentrate efforts on effective spending through outcome-based mechanisms when appropriate and possible in developing country contexts.

Why impact bonds for building back better?

In the past decade of impact bond use, much has been written about their potential and observed benefits, including many studies by Brookings. In this literature, a number of claims were made about impact bonds, which we summarized as the 10 common claims in our seminal report on the tool in 2015. Several of those claims are particularly relevant for the consideration of impact bonds as a tool in rebuilding in a post-pandemic world, in which needs are great and funding is scarce.

Focus on outcomes. Impact bonds can ensure that limited funding is directed at programs that produce results, in the form of measurable outcomes for the populations they serve. The focus on outcomes allows for more flexibility and adaptability in service delivery than is often available in more traditional contracting. This is because with the traditional input- and activity-based contracts, these elements are often fixed to an original workplan and theory of change, and as such deviations in activities and inputs require extensive contract modification. With outcomes-based contracting, it is the outcomes that are fixed, and the inputs and activities needed to achieve those outcomes can more easily shift.

Crowd in private funding. As governments, donor agencies, and other funders face tremendous constraints on their budgets as a result of the pandemic, social services funding is needed immediately to rebuild the U.S. and other economies across the globe. Impact bonds provide a mechanism to address critical liquidity constraints and ensure that limited funding is spent wisely and only when outcomes are achieved. This is extremely attractive to governments and others who are currently scrambling to put Band-Aids on immediate, pressing issues, leaving little funding to invest in rebuilding. The prospect of achieving both a social and a financial return is alluring for traditional philanthropists who commonly make grants to nonprofits without much evidence of the outcomes to be achieved, nor the possibility of reusing that capital for further good. For impact investors, it provides an opportunity for concrete evidence of impact, as metrics and measurement are core to impact bonds.

Reduce government and donor risk. A product of the belt tightening that followed the 2008-2009 financial crisis, social impact bonds were proposed by early advocates as a method of transferring the risk of social programs from governments to investors, since governments only pay for successful programs. As the world once again finds itself amid a crisis, this risk transfer has renewed importance. Given the focus of most current impact bonds on the hard-hit social sectors of employment, education, and social welfare services, the tool can be used to target recovery efforts, with the government and private sector paying only for those interventions that are successful. The mechanism also has the potential to provide a testing ground for new interventions, different types of beneficiaries, or for programs to be scaled. For this scenario, impact-first investors are necessary, since often—and particularly with current constrained budgets—government will be unwilling to take on additional risk as will investors looking for a market return.

Strengthen systems by incentivizing collaboration, building a culture of monitoring and evaluation, and driving performance management. As the United States and the rest of the world build back their economies and society, they can build back better—and impact bonds can help. Three elements identified in our 10 common claims about impact bonds contribute to systems strengthening. First, the contractual arrangements and governance structure of impact bonds inherently incentivize collaboration among impact bond partners. Such cooperation can be seen between public and private partners (including third sector), across levels of government (federal, state, and local) and between sectoral divisions of government (such as departments of health and social welfare). During the COVID-19 crisis, it has become even more apparent that there is strong motivation to problem-solve and collaborate in impact bond-funded projects. Second, because impact bonds are focused on outcome achievement, they can build a culture of monitoring and evaluation across stakeholders, including government, investors, and service providers. This can translate into better data collection before, while, and after social services are provided, and can encourage the linking of existing systems of administrative data. Third, this approach drives performance management among service providers in impact bonds—it encourages providers to use the data to tailor services to beneficiary needs with the goal of achieving the best possible outcomes.

How to do it

Shifting from input- to outcome-based financing doesn’t happen overnight. Our research into the global impact bonds market has demonstrated that there are a number of fundamental factors to enable this change in funding and delivery. In this brief we emphasize three of these:

- Educate and build capacity.

- Utilize and develop legislation.

- Pool investment and outcomes capital.

Educate and build capacity

The most critical shift that is necessary to mainstream outcome-based financing into policymaking is a shift in mindset—paying for services that don’t deliver outcomes can no longer be the status quo. Part of this mindset shift requires an understanding of the importance of data. Our research has identified at least four types of data that are critical to impact achievement: data on real-time performance, data on longer term outcomes, data on the costs of service delivery, and data on the cost of inaction. Efforts in support of evidence-based programs in the U.S. and elsewhere must be accompanied by adaptive management—the flexibility and capacity to use real-time evidence to tailor services to the needs of beneficiaries so that outcomes are achieved. Outcome-based financing both requires this and can facilitate its development, but for it to occur, governments and service providers must build up capacity. This should occur through educating state, local, and federal policymakers, program officers of bilateral and multilateral development organizations, and service providers on outcome-based financing, including contracting, outcome measurement, and evaluation. Building on the examples of the U.K. and Portugal, establishing a central unit within the government that shares knowledge and provides capacity building would be the most efficient way to do this.

Past examples of capacity building and technical support in the U.S. are numerous and could be enhanced or replicated. For instance, the Social Innovation Fund (SIF), a program of the Corporation for National and Community Service with both public and private funding, helped develop the outcome-based financing sector by funding both project development and knowledge sharing. SIF provided grants to organizations to develop PFS projects in 2014 and 2016, as well as committed additional funding to support administrative data use in existing projects. Also, the Government Performance Lab at the Harvard Kennedy School of Government has provided technical assistance to state and local governments on nine PFS projects in the U.S.

Within multilateral and bilateral international organizations and development finance institutions, a mandate from leadership for intra- and interagency coordination and further capacity building is necessary. Although USAID and the World Bank, for example, have implemented some of these efforts, many have been bespoke, siloed within different parts of the institutions, or limited to specific funding rather than mainstreamed within the institutions across streams of funding.

Utilize and develop legislation

To bolster the use of outcome-based financing, existing legislation must be improved and new legislation should be considered. Currently, there are a number of legal or institutional barriers that can make it difficult or unattractive for governments to fund based on outcomes and for investors to invest in social services. For outcome funders such as governments, international organizations, and philanthropy, these barriers can include the inability to: commit funds into the future, pay returns to private investors, and harness savings accrued at different levels of government or in different sectors (the so-called wrong-pockets problem). For investors, tax policies can encourage or discourage investing in philanthropic ventures that lend a return.

While some legislative progress has been made to overcome the legal and institutional barriers to governments paying for outcomes, these policies have not yet been used to their full potential. For example, the $100 million Social Impact Partnerships to Pay for Results Act (SIPPRA), passed in the U.S. 2018, aims to support outcome-based financing and provide funding from the Treasury Department for feasibility studies for PFS projects, as well as pay for outcomes. Under this legislation, state and local governments can receive funding for programs that deliver pre-defined social outcomes and cost savings. The act also established the Federal Interagency Council on Social Impact Partnerships and the Commission on Social Impact Partnerships to provide support on project applications. Additionally, SIPPRA joined other federal efforts in the U.S. to enable the use of PFS strategies in conjunction with existing federal funding streams and legislation, such as the Every Student Succeeds Act, the Maternal and Early Childhood Home Visiting program, and the Department of Justice’s Second Chance Act. In addition, the Foundations for Evidence-Based Policymaking Act “requires the federal government to modernize its data management practices, evidence-building functions, and statistical efficiency to inform policy decisions.”

New legislation that prioritizes evidence-based policymaking and outcome-based financing—including PFS—appears to be on the horizon already. Proposed in January 2021, the bipartisan Revitalize and Expand SNAP Education and Training (RESET) For America’s Future Act would “provide new resources for state and local governments through the Supplemental Nutrition Assistance Program Employment and Training (SNAP E&T) program” and “substantially increase federal reimbursement for programs and services that are rigorously proven, rigorously evaluated for the first time, or include a contract that ties at least 20 percent of funds to positive outcomes—such as improved future earnings.”

For U.S. and global investors, legislation—including tax policies—can either incentivize or disincentivize investment in social services. Impact bonds, which are essentially a type of investing as they offer both a social and a financial return, can be particularly complex from a tax perspective. To help incentivize investment, the U.S. National Advisory Board on impact investing proposed 17 actions to increase impact investing both in the U.S. and globally. These include such actions as clarifying standards for program-related investment and mission-related investment, removing investment constraints in terms of size and length, supporting community development finance institutions (CDFIs), and encouraging public-private investment capital funds for global development. Further legislation that encourages investment by foundations, high-net-worth-individuals, and development finance institutions (DFIs) could greatly help rebuilding efforts post-pandemic through outcome-based financing.

Pool investment and outcomes capital

The design and negotiation of bespoke impact bond deals have taken a lot of time and resources from all parties involved. Though some of these burdens would be alleviated through capacity development and legislation, creating economies of scale by pooling both investment and outcome-funding capital would lead to further efficiency.

Outcomes funds pool several different impact bond agreements through streamlined and shared contract templates, metrics, and evaluation systems. These funds lower transaction costs by spreading them across more and larger projects and, in theory, can also lead to launching projects in less time. While outcomes funds first began in the U.K. in 2012, they have since spread globally, and are particularly on the rise in the developing world. Despite their global uptake, the model has not yet been widely used in the United States and presents an opportunity for rapid expansion of impact bond or PFS projects. Social Finance U.S., an intermediary advisory organization, has helped create outcomes funds using an outcomes rate card, but these projects have not yet been fully realized. State governments could use outcome funds to launch similar programs in different municipalities, the federal government could use them to launch programs targeting similar challenges across states, and USAID could participate in global outcomes funds.

There is also potential to capitalize on economies of scale in raising and managing investment capital. Most impact bond projects have raised investment capital directly from banks, private individuals, foundations, and other impact investors. However, this capital typically can’t be raised until the project has been well developed, with outcome funding committed and clear estimates of the risk profile of the intervention. Through dedicated investment funds, market efficiencies could be unlocked. While these funds have taken off in the U.K. and are gaining traction in the U.S., they have largely been driven by impact investing firms. There are multiple roles for the government in expanding this space. The first is through improved tax policy incentives and other legislation as described above. In the international sphere, DFIs such as the U.S. Development Finance Corporation (DFC) can pool investment funds globally to achieve high impact at scale across multiple projects.

Conclusion

Outcome-based or PFS financing, including impact bonds, have the potential to play an important role in building a more prosperous and equitable society in the aftermath of the global pandemic. By focusing on outcomes and tapping into private capital, impact bonds guarantee that outcome funders—including governments, foundations, and international organizations—only pay when agreed upon metrics have been achieved. Furthermore, they can strengthen systems of social services delivery by incentivizing collaboration, improving monitoring and evaluation, and encouraging adaptive management. In addition, they have the potential to contribute directly to economic recovery because they are well-suited to finance programs such as job training (or retraining) and housing, mental health, and substance abuse support that may be particularly needed in the wake of the crisis.

Seeding and institutionalizing an outcomes-focused mindset at all levels of government, among international agencies, and within nonprofit service providers is a daunting task. However, we believe that this is the only way forward for social programs that are falling short of achieving outcomes, especially for the disadvantaged populations hardest hit by the pandemic. Our recommendations to educate and build capacity, utilize and develop legislation, and pool investment and outcomes capital should be a fundamental part of the effort to build back stronger societies in the U.S. and across the globe. When implementing these and other policy recommendations put forth by our colleagues elsewhere in this series, the cost-effectiveness of programs must be considered alongside the cost of inaction: What is the cost to society of failing to intervene?

In addition, we must consider how to address not only the inequalities that the pandemic has exacerbated, but also how to avoid building back a world which replicates the same inequalities that previously existed. Recovery efforts taken by the United States government going forward must seek to help women, people of color, immigrant and refugee populations, and other historically marginalized groups. This will be the only way to truly strengthen the fabric of this nation and make it more resilient to future shocks.

Related Content

Authors

-

Acknowledgements and disclosures

The authors would like to thank Emily Markowitz for excellent research assistance and Katherine Portnoy and David Batcheck for editorial contributions to this publication.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).