Following the release of the World Economic Outlook earlier this month, the International Monetary Fund launched its Regional Economic Outlook (REO) report for sub-Saharan Africa this week. The report attributed the accelerating gross domestic product (GDP) growth that sub-Saharan Africa experienced in 2017—from 1.4 percent in 2016 to 2.6 percent this year—largely to Nigeria’s resumption of oil production and drought recovery in Southern Africa, as well as modest improvements in the external environment. GDP growth in sub-Saharan Africa is projected to reach 3.4 percent in 2018, as external conditions continue to be favorable. Growth is strengthening globally, including in some of the region’s main economic partners, such as China and the euro area, which could promote greater trade with and investment in Africa. Furthermore, better financing conditions and investors’ appetite for yield have prompted Africa’s frontier economies (e.g., Côte d’Ivoire, Nigeria, and Senegal in 2017) to issue more sovereign bonds.

Still, the REO notes that vulnerabilities are high throughout the region. Public spending and mounting public debt are driving much of the growth in the region’s faster-growing economies, raising questions about debt sustainability as debt service costs are rising. In half of the continent’s economies, public debt now exceeds 50 percent of GDP. Moreover, 12 of the region’s low-income countries were in debt distress or at high risk of experiencing debt distress in 2016, up from seven in 2013. According to the REO, slow growth, the commodity price slump, fiscal deficits, and exchange rate depreciation have contributed to these rising levels of debt and debt distress.

Meanwhile, political uncertainty and delays in implementing policy adjustments to facilitate recovery from the commodity slump have led foreign currency reserves in many countries—especially commodity exporters with fixed exchange rate regimes—to dwindle, making the region susceptible to terms-of-trade shocks.

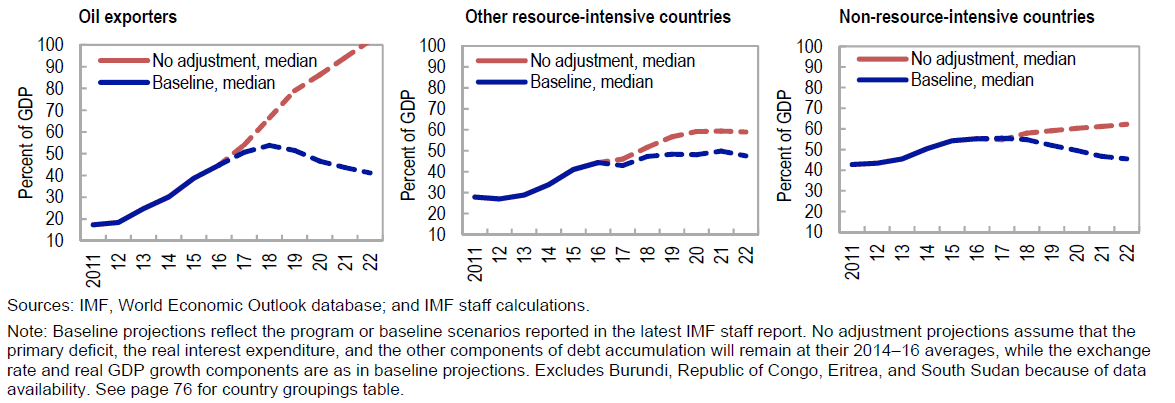

In this context, the report suggests two key policy priorities for sub-Saharan African countries: fiscal consolidation and economic diversification. Fiscal consolidation—periods of fiscal adjustment during which spending cuts are made or non-commodity revenue is mobilized to improve fiscal positions—is necessary, especially in oil-exporting countries as seen in Figure 1. The IMF suggests that fiscal consolidation should prioritize revenue mobilization and targeted cuts in recurrent spending—while preserving spending on critical infrastructure—as well as social spending to prevent strains on growth and maintain social safety nets to protect low-income households.

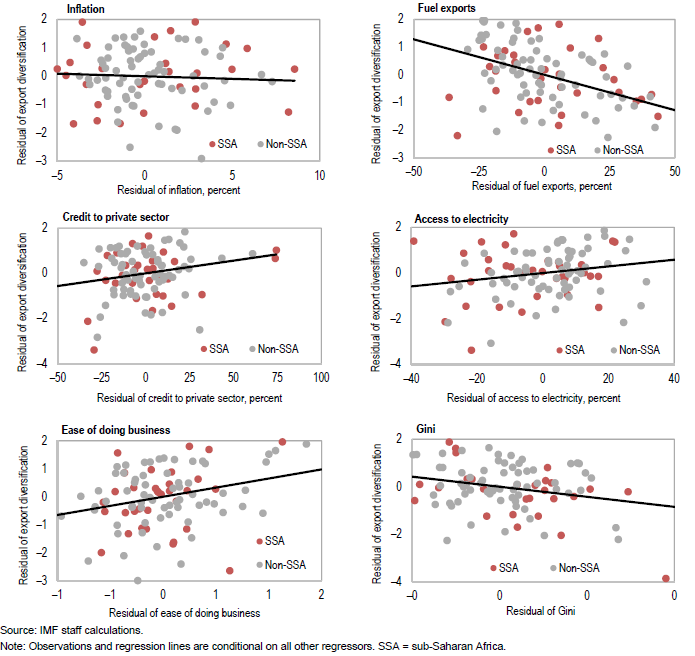

At the same time, the report highlights “a more diversified economy in terms of production and export structure are associated with higher growth outcomes.” Yet, there are many paths to structural transformation and export diversification. Using global cross-country data, the report finds that certain characteristics—including macroeconomic stability, access to credit, good infrastructure, a conducive regulatory environment, and a skilled workforce—are linked to higher economic diversification, whereas oil dependency is associated with less diversification (see Figure 2).

Furthermore, the report states, select African country case studies show that policies aiming to promote economic diversification are more likely to succeed when they leverage a country’s endowments and existing strengths, provide an enabling environment for private sector expansion, and help firms overcome specific challenges they face.

Related Content

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Figures of the week: The importance of fiscal consolidation and economic diversification in sub-Saharan Africa

November 3, 2017