With vaccination rates increasing and COVID-19 case rates declining, there is an urgency to get back to normal.

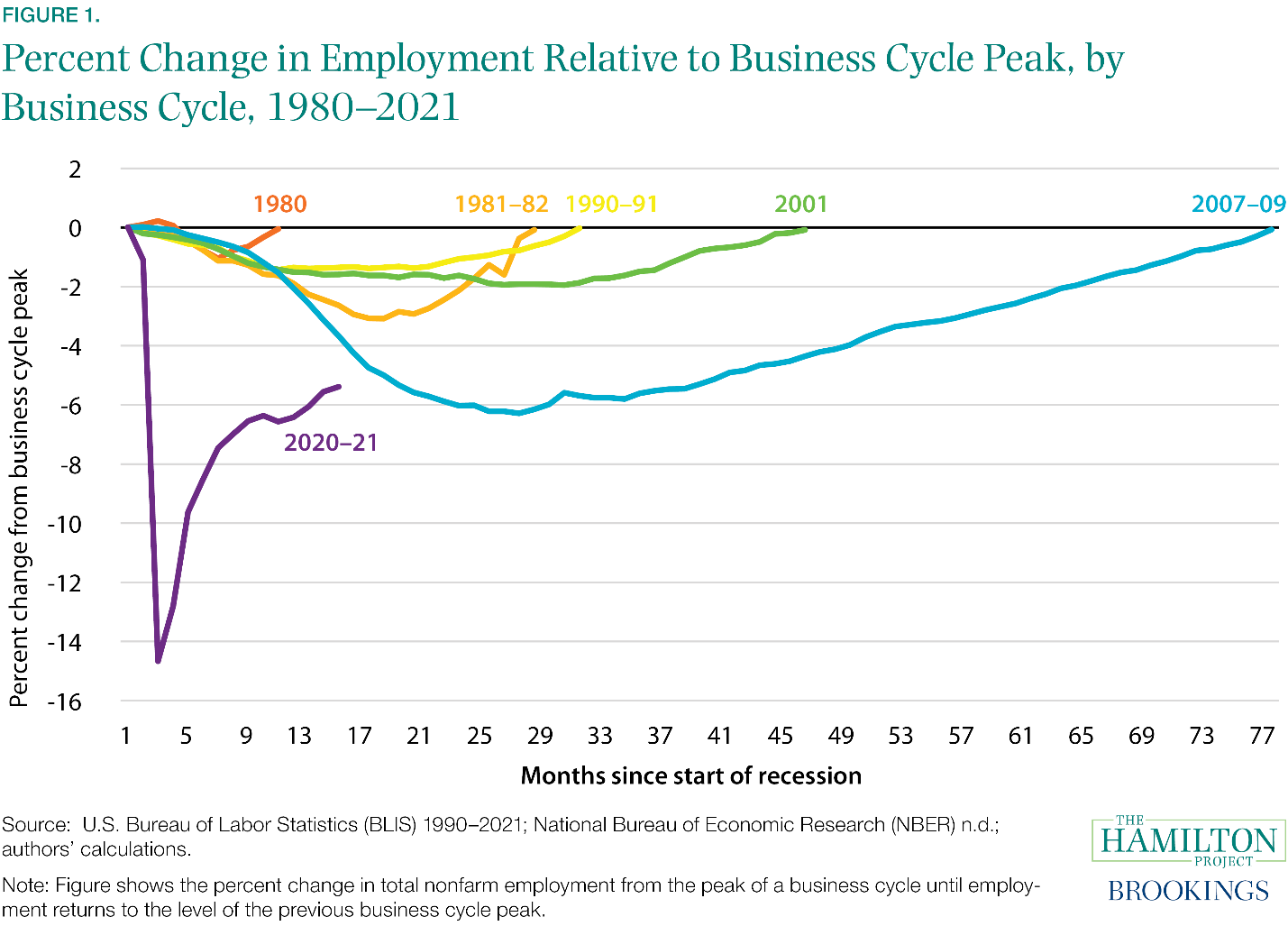

The April 2021 employment report was a timely reminder that not everyone will experience the recovery from this crisis the same way – or quickly. The post-pandemic shortfall in employment was over 10 million jobs relative to where the labor market would be in absence of the recession. Despite the relatively large average gains over February and March (653,000 jobs created), net employment gains slowed in April, surprising most observers (see figure 1). While any single monthly estimate is noisy, the last month’s news from the labor market seemed inconsistent with what we have seen in consumer spending; indeed, total vehicle sales were higher in April than in the last 16 years.

In the May 2021 employment report to be released tomorrow, which will provide information on the health of the labor market in mid-May, we expect to see continued improvement across several margins. We expect flows into employment to be strong and we will be looking at whether flows out of employment begin to taper (in line with the decline in new unemployment insurance claims). We will focus closely on rates of labor force participation to see if constraints holding back labor supply continue to ebb. Finally, we will look closely at measures of labor demand such as hours worked and overtime, as well as wages, to see what steps firms are taking to attract workers across sectors.

In this analysis, we outline factors that we think have slowed and will continue to slow net employment gains as the post-COVID economy reconstitutes itself. We note evidence of substantial churn in and out of jobs, including workers leaving what may have been temporary pandemic-related jobs: people leaving employment without moving immediately into a new position reduces net employment gains in a given month. We then describe some of the broad factors that may be holding people back from participating in the labor force, including fiscal policy. As an example of one factor having a significant effect on a narrower group, we show that caregiving responsibilities are dampening the labor supply of mothers whose youngest or oldest child is between the ages of 5 and 12 in states with a higher degree of elementary school closures.

Changing composition of work

The employment report released in early May showed a remarkable amount of churn in the labor market in April. Generally speaking, when we talk about the change in employment in any given month – for example April saw an increase of 266,000 – that number is the net of big flows in and out of employment. In April 2021, 6.6 million people went from being employed to unemployed or out of the labor force, while 6.7 million moved from unemployment or nonparticipation to employment. Those numbers sound big, but how big are they are relative to the last few months and relative to more normal times? The flow out of employment is higher than since December 2020: The average from January 2021 to March 2021 was 6.3 million. So, 300,000 more people left employment in April 2021 than on average over the preceding three months.

And, what were those outflows like pre-pandemic? In April 2019 and indeed on average over that whole year – 6.1 million people flowed out of employment. Think of the difference of 500,000 this way:

If employment had been as “sticky” in April 2021 as it was pre-pandemic, and flows into employment were as we observed them (considerably higher than pre-pandemic), the increase in employment might have been more like 800,000 – close to consensus expectations for April.

So, how do we interpret this increase in the flow out of employment? We have circumstantial evidence that it represents a transition from a pandemic labor force to a post-pandemic labor force.

New business formation was extraordinarily strong during the pandemic even as hundreds of thousands of businesses failed.

In 2019, Census reported that about 110,000 applications a month were filed among new business likely to employ people. Applications fell off notably early in the pandemic. Then, in July 2020, they spiked at over 190,000, and have averaged about 150,000 since. It stands to reason that many of these applications have reflected short-term business ventures dedicated to pandemic-related activity.

In addition, the changing composition of consumer demand suggests we are beginning to transition to a post-pandemic economy. For example, sales at grocery stores surged for months at the beginning of the pandemic but were much softer in March and April 2021. Meanwhile, restaurants saw very large increases in sales in those two months relative to 2020. The changing composition of demand will no doubt bring along with it a changing composition in the demand for workers. As some sectors try to rebound quickly and others fall back closer to pre-pandemic levels, the large swings in which sectors have vacancies may slow down job finding rates. As dynamic as the US labor market is, we should expect some bumps in the road as we transition to the post-pandemic economy.

The share of workers quitting jobs every month is quite high, suggesting the vacancies workers have been filling were not long-term matches.

The dynamism in the US labor market is evident in the percentage of workers who are quitting their jobs. From the fall through March 2021, that percentage has been back to pre-pandemic levels (2.4 percent), when the labor market was quite strong. Workers appear to be moving from job to job, trying to keep up with the changing composition of labor demand and trying to find a better, more productive match.

Factors holding back labor supply and employment gains

Participation in the labor market (those who are working plus those who are unemployed and actively seeking work) has recovered somewhat from pandemic lows but remains weak. An open question is how much stronger employment gains would be if participation were higher – or whether we would just see more people being categorized as unemployed instead of out of the labor force. Strong wage gains in some sectors and for some groups as well as a lot of anecdotal reporting suggests that certain firms are having a difficult time finding workers. Three questions emerge:

For how long might the large compositional issues described above lead to flows out of employment?

Fiscal support in the form of unemployment insurance benefits and other increases in transfers may be affecting the transition described above. Two potential channels could be at work, although we have no evidence suggesting either is currently a significant factor. First, layoffs by firms are likely facilitated by firms’ knowledge that most laid off workers will qualify for expanded unemployment insurance. Second, some workers quitting their jobs for “good cause” may also qualify for such benefits, making them more likely to quit and look for a better match. On the one hand, the availability of UI benefits means that workers will have time to find a good labor market match (and perhaps take a needed moment after a very difficult year). Indeed, the pandemic laid bare some of the worst aspects of working in certain sectors, giving workers an impetus to change industries. So, the recovery might be slower by a few months as a result but ultimately result in a more productive economy. On the other hand, the longer this transition takes and workers remain without employment, the more skills and labor force attachment deteriorate.

To the degree reduced labor force participation is holding back the recovery, how much of that is due to factors unique to coming back from a pandemic-caused recession?

Fiscal support is helping people prioritize their health over labor market income—certainly one of the goals when the support was put in place. That dampening effect on labor market participation should dissipate as we continue to vaccinate the population and beat back the pandemic.

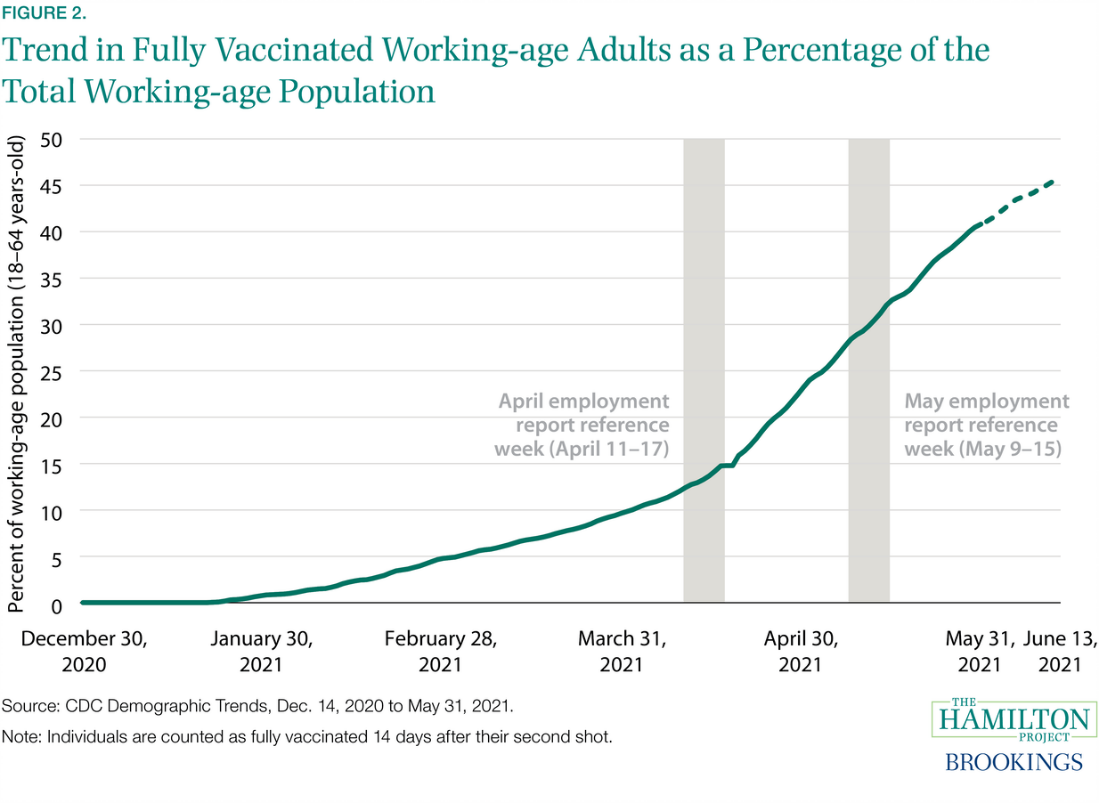

From mid-April to mid-May 2021 the share of working age Americans (18-64 years old) who were at least two weeks past their final COVID vaccination dose more than doubled; but still only about 3 in 10 had achieved full immunization by that time (see figure 2). We find that employment as a share of the population has grown faster in states with faster improvement in working-age vaccination rates. States that lag behind on working-age vaccination rates will likely slow the recovery in the national labor market.

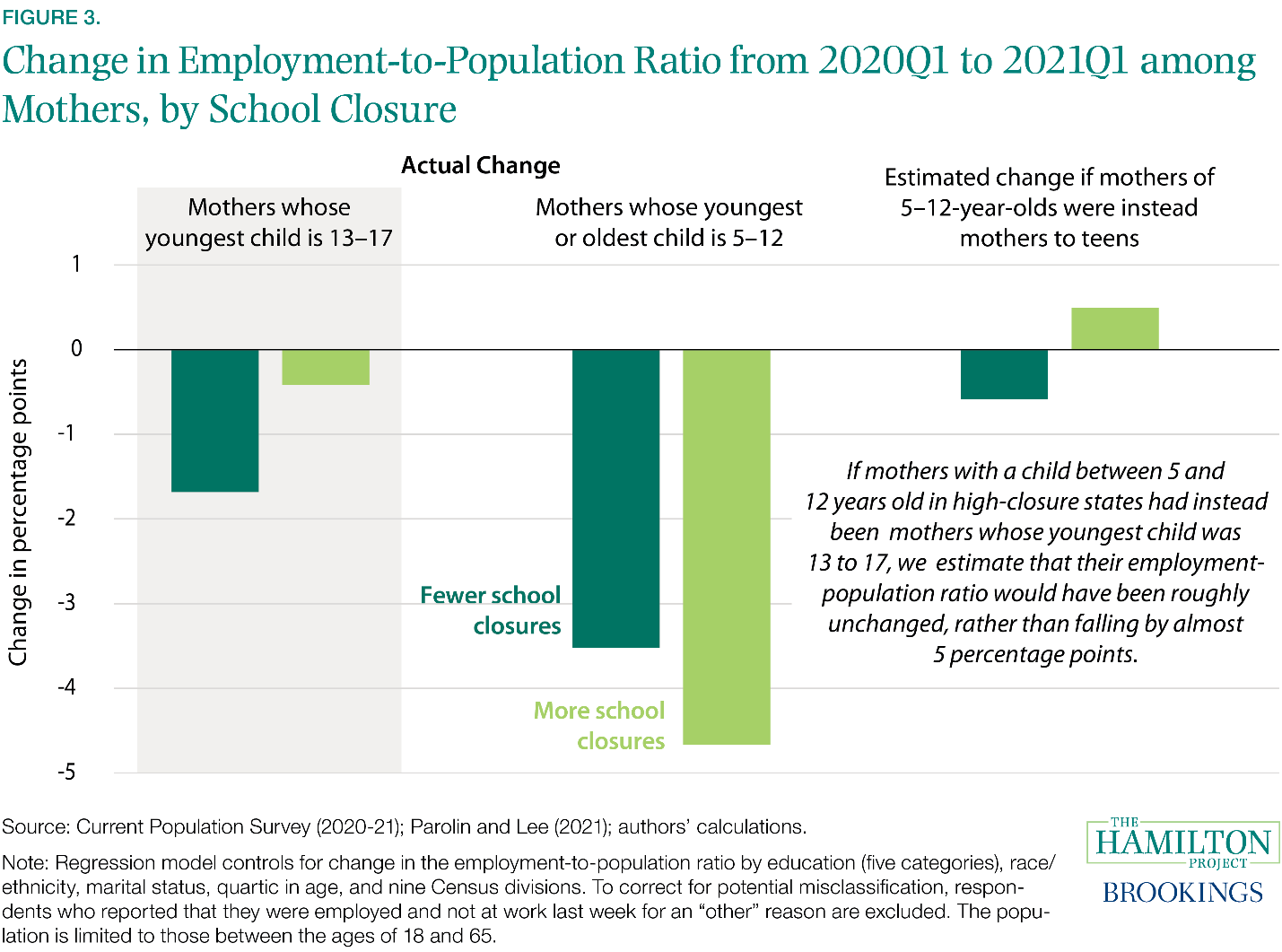

Other factors unique to the pandemic are having acute effects on relatively narrow groups. For example, the employment-population ratios of mothers of elementary school age children – the demographic likely bearing the brunt of school closures – fell more than that of other mothers and their employment rates continue to lag behind others through the beginning of 2021. To be sure, the portion of the labor force pre-pandemic comprised of mothers with elementary-school aged children is small enough (at only 9 percent) that these relatively large declines do not account for much of the weakness in labor force participation and employment in aggregate. Consequently, addressing child care will not come close to – on its own – making up lost ground in labor force participation. In addition, some explain this finding by examining the industries in which these mothers typically work, since their employment tends to be concentrated in industries that saw relatively large declines in employment. Nonetheless, the challenges for these parents are acutely felt and solvable.

We find that in states with relatively high levels of elementary school closures, the nearly 5 percentage point drop in the employment-population ratio for mothers with children age 5 to 12 is more than fully accounted for by having elementary school age children instead of teenagers (figures 3). We use school closure data to group states into those with population-weighted high and low closure rates. We then – looking at whether a mother’s oldest or youngest child is between the ages of 5 and 12 and school closure rates – examine the declines in the employment-to-population ratios from the first quarter of 2020 to the first quarter of 2021 (after adjusting for the misclassification errors that were particularly significant early in the pandemic and accounting for mother’s age, level of education, race/ethnicity, marital status, and region). We note that in high-elementary-school-closure-states, the recovery in the labor market for mothers of teens is almost complete, whereas that for mothers of teens in low-closure-states lags. In both types of states, we find that employment outcomes were statistically significantly worse for mothers having a youngest or oldest child 5 to 12 instead of the youngest being a teenager.

However, we find a larger (as shown in the figure) and more statistically significant effect (not shown) in states with more closures: if mothers of 5-12 year olds in high-closure states had instead been mothers to teens, we estimate that their employment-population ratio would have been roughly unchanged rather than falling nearly 5 percentage points.

What role has fiscal policy played and will continue to play in supporting or stalling the recovery?

Much has been written about whether the generous unemployment insurance benefits are temporarily slowing the job finding rate exclusive of any concerns about health risks, child care issues, or other factors making it challenging to work right now. Analysis by economists at the San Francisco Fed finds that the effects are modest. As mentioned above, one consequence of that effect could be a greater loss of skills and labor force attachment—along with bottlenecks in hiring. However, another effect could be better and ultimately more productive labor market matches, particularly in states where the labor market recovery has been slower. Regardless – any effects of expanded unemployment insurance benefits on labor supply will dissipate quickly as the benefits expire nationally in early September and before then in an increasing number of states. Indeed, policymakers should be on high-alert for whether the expiration of those benefits results in extraordinary financial hardship for some workers unable to find jobs.

Conclusion

There are many signs that the U.S. labor market is on the mend. For example, the average net increase in payroll employment from February to April was over 500,000. Initial unemployment insurance claims continue to decline. The number of unemployed people per job opening has fallen sharply. Teens are working in the labor market at higher rates than at any time in the past decade.

Nonetheless, policymakers must be vigilant — continuing to increase easy access to vaccines and helping to make working safe and rewarding. Expanding the Earned Income Tax Credit for childless adults will help to draw in labor market participants from the sidelines. School and child-care reopening will help those groups acutely affected. Still, the labor market recovery will undoubtedly be uneven. Some people and some sectors will continue to require fiscal support before we emerge from the crisis.

Authors

-

Acknowledgements and disclosures

The authors thank Stephanie Aaronson, Kathryn Edwards, Jason Furman, Este Griffith, Melissa Kearney, Gray Kimbrough, Michael Madowitz, Kriston McIntosh, Ryan Nunn, and Heidi Shierholz for conversations about these issues and thoughtful comments. Sara Estep provided superb research assistance.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Examining the uneven and hard-to-predict labor market recovery

June 3, 2021