This paper is part of the Fall 2024 edition of the Brookings Papers on Economic Activity (BPEA), the leading conference series and journal in economics for timely, cutting-edge research about real-world policy issues. Its conference draft was presented at the Fall 2024 BPEA Conference on September 26-27, 2024. (Drafts, presentation recordings, and slides are available via the link.) Submit a proposal to present at a future BPEA conference here.

Final version posted: June 2025

Download final paper with discussion comments and conference discussion summary

Information provided to Congress about the economic and budgetary effects of proposed legislation could be expanded and improved if further investments were made in modeling and experience at Congress’ nonpartisan agencies, according to a paper discussed at the Brookings Papers on Economic Activity (BPEA) conference on September 26.

The paper discusses dynamic scoring—the inclusion of additional economic feedback effects when estimating the budgetary impact of legislative proposals. It examines the trade-offs that arise when considering why, when, and how dynamic scoring could be used more extensively, and how those trade-offs differ across policy areas.

The authors—Douglas Elmendorf of Harvard University, Glenn Hubbard of Columbia University, and Heidi Williams of Dartmouth College—note that Congress in recent years has asked the Congressional Budget Office (CBO) and the staff of the Joint Committee on Taxation (JCT) to provide more dynamic analyses that incorporate additional economic feedback effects.

“The agencies have responded by drawing on an expanding body of research to produce innovative analyses, improve their modeling tools, gain experience, and publish reports regarding their methodologies and results,” they write “This work has reinforced the value of the agencies providing unbiased and evidence-based analyses of the effects of potential policies on labor, capital, productivity, and other economic outcomes.” However, estimates of these additional economic feedback effects are very rarely included in the formal cost estimates provided to Congress for specific pieces of legislation, the authors note.

In “Dynamic Scoring: A Progress Report on Why, When, and How,” the authors explain that dynamic estimates are often asserted to take more time and work than is feasible given the deadlines required by Congress. But, they write, “CBO and JCT have invested—to their credit—in the tools and experience needed to produce dynamic estimates, and those investments have reduced to some extent the additional time and work needed to generate such estimates.” The authors add that “further targeted investments could make more progress along these lines.”

Dynamic scoring also involves confronting uncertainties inherent in estimating additional economic effects. For at least some important effects that are excluded from non-dynamic estimates, CBO and JCT can draw on substantial bodies of evidence and receive professional feedback on their use of the evidence, according to the paper. Moreover, including these additional economic effects could reduce the risk of bias in estimates.

The economic changes stemming from legislative proposals are often small relative to the size of the economy, the authors acknowledge. However, the budgetary effects of those changes can be large relative to other budgetary effects of legislative proposals, and understanding the magnitude of economic effects can be useful to policymakers regardless of whether the effects are large or small.

“If Congress has better information about the sign and magnitude of economic effects, that’s the win,” Hubbard, a past chair of the White House Council of Economic Advisers, said in an interview with The Brookings Institution.

Elmendorf, a past CBO director, said in an interview that Republicans and Democrats have differed historically over when to use dynamic scoring, with Republicans favoring dynamic scoring of tax cuts and Democrats pushing for dynamic scoring of spending programs. But, given the advances in dynamic analysis in recent years, there is a chance now for movement toward its broader use, he said.

“Congress has to want this. It is not up to CBO and JCT,” he said.

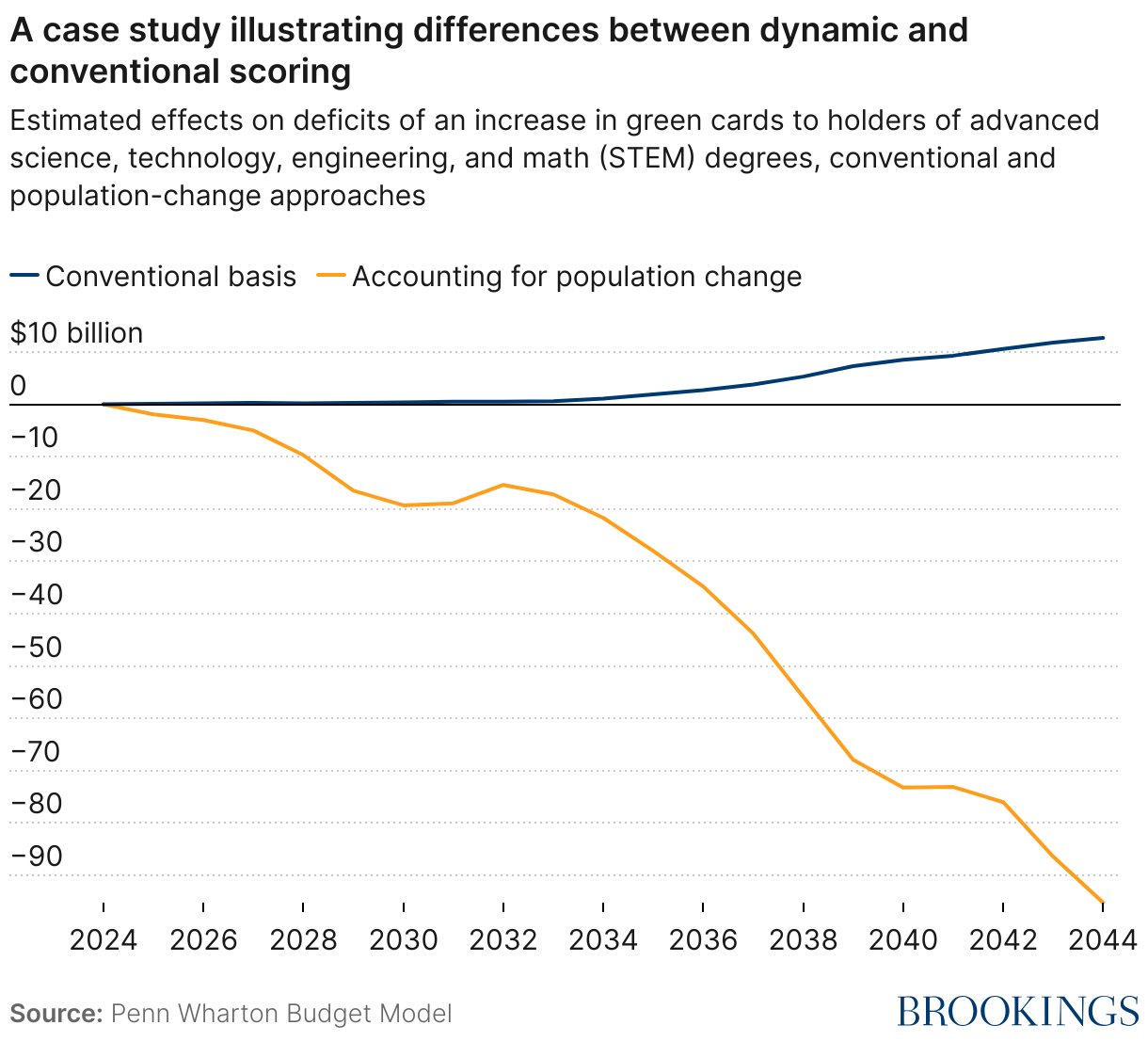

The paper presents case studies of some areas where dynamic scoring could provide more information at this time and other areas where it cannot yet provide more information, given the state of modeling and the research literature. The case studies cover immigration policy, research and development spending, and federal permitting of infrastructure investments. For example, the difference between conventional and dynamic estimates of changing the authorized number of high-skilled immigrants is “especially stark,” they write, because conventional estimates do not include the effects on federal revenue of the change in population or other economic effects.

Authors

Authors

Discussants

Citations

Elmendorf, Douglas, Glenn Hubbard, and Heidi Williams. 2024. “Dynamic Scoring: A Progress Report on Why, When, and How.” Brookings Papers on Economic Activity, Fall: 93–134.

Hoagland, G. William. 2024. “Comment on ‘Dynamic Scoring: A Progress Report on Why, When, and How’.” Brookings Papers on Economic Activity, Fall: 135–142.

Lucas, Deborah. 2024. “Comment on ‘Dynamic Scoring: A Progress Report on Why, When, and How’.” Brookings Papers on Economic Activity, Fall: 142–155.

-

Acknowledgements and disclosures

Heidi Williams wrote this paper while she was a visiting scholar at the Congressional Budget Office (CBO), where she is currently a consultant. The authors did not receive financial support from any firm or person with a financial or political interest in this paper. Deborah Lucas, one of the discussants, is a former employee and current consultant for CBO.

For valuable conversations and comments, the authors are grateful to Alexander Arnon, Alan Auerbach, Jan Eberly, Theresa Gullo, G. William Hoagland, Douglas Holtz-Eakin, Deborah Lucas, Donald Marron, Dylan Matthews, Alexander Mechanick, Benjamin Page, Kent Smetters, Jón Steinsson, Caleb Watney, David Weiner, David Wessel, and staff members of CBO and JCT. The case studies the authors discuss draw on collaborative work with Arnon, Gullo, Page, Smetters, Weiner, Matthew Esche, Zachary Liscow, and Jeremy Neufeld. The authors are solely responsible for the contents of the paper, and the views expressed here should not be attributed to any of the individuals acknowledged or any institution with which the authors are currently or formerly affiliated.

David Skidmore authored the summary language for this paper. Chris Miller assisted with data visualization.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).