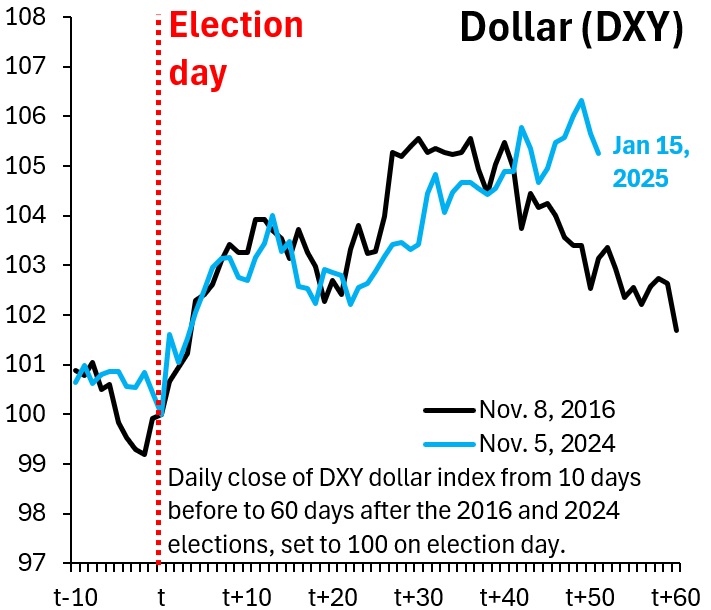

In the immediate aftermath of the U.S. election, we reviewed global markets for signs that tariffs were getting priced. At the time, the dollar had risen meaningfully, but that rise looked like it was driven by expectations of faster U.S. growth, not by markets putting meaningful probability on additional tariffs. This picture has grown even more pronounced since then, with the dollar rising further, but not versus currencies that would be most impacted by China tariffs, such as the Chinese yuan or Japanese yen. The conclusion remains, therefore, that markets price little tariff risk.

We review the various moving parts of a tariff confrontation between the U.S. and China. A lot of this comes down to game theory, with China’s most potent weapon being depreciation of the yuan as an offset to additional U.S. tariffs. Such a depreciation could weigh on the S&P 500, causing spillback to the United States in the form of tighter financial conditions. The incoming administration may try to preempt this via sector-specific tariffs or—if it goes the path of a universal tariff—by phasing in such a tariff and making it conditional on certain benchmarks China must meet. Either way, given how little is priced, it seems likely that market volatility will rise in the months ahead.

Markets price little tariff risk

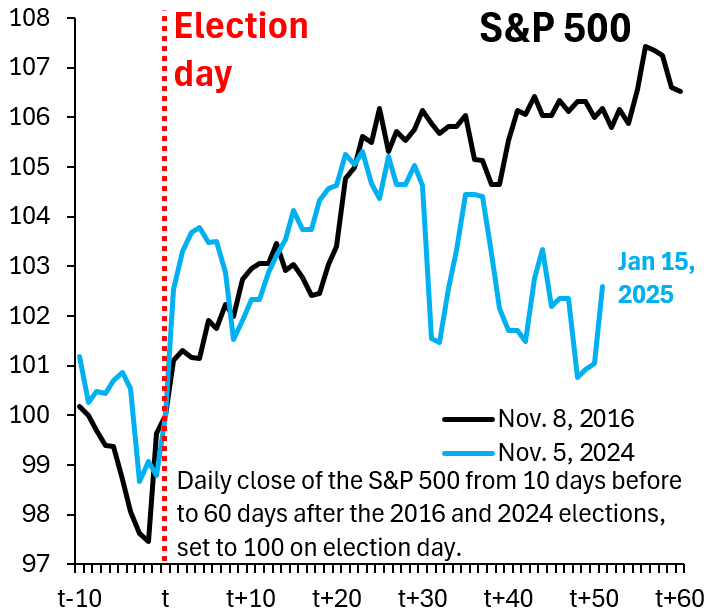

The dollar has risen substantially since the election (Figure 1), outperforming U.S. equities, which have lagged increasingly (Figure 2). The growing wedge between the dollar and S&P 500 lends itself to the interpretation that markets put a meaningful weight on tariffs. After all, many of the companies in the S&P 500 are multinationals that would be adversely impacted by escalating trade tensions between the U.S. and China. However, that conclusion is misleading.

Figure 1. Daily close of DXY dollar index from 10 days before to 60 days after the 2016 and 2024 elections, set to 100 on election day

Source: Bloomberg

Figure 2. Daily close of S&P 500 from 10 days before to 60 days after the 2016 and 2024 elections, set to 100 on election day

Source: Bloomberg

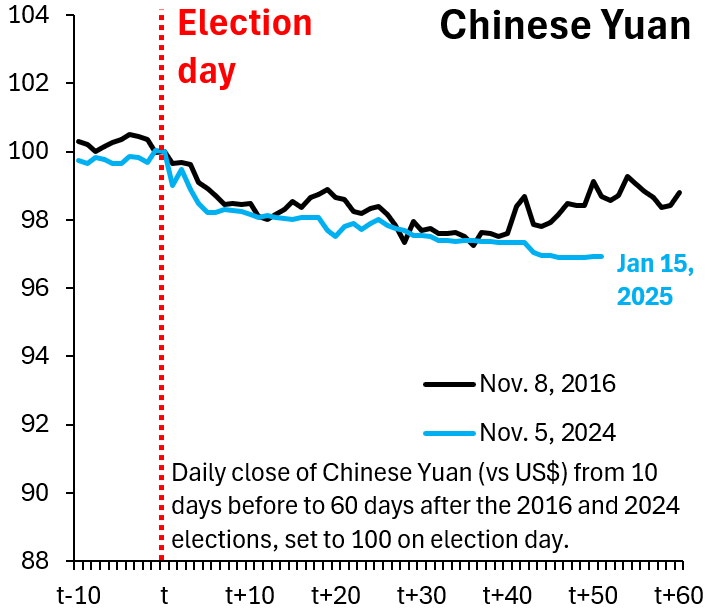

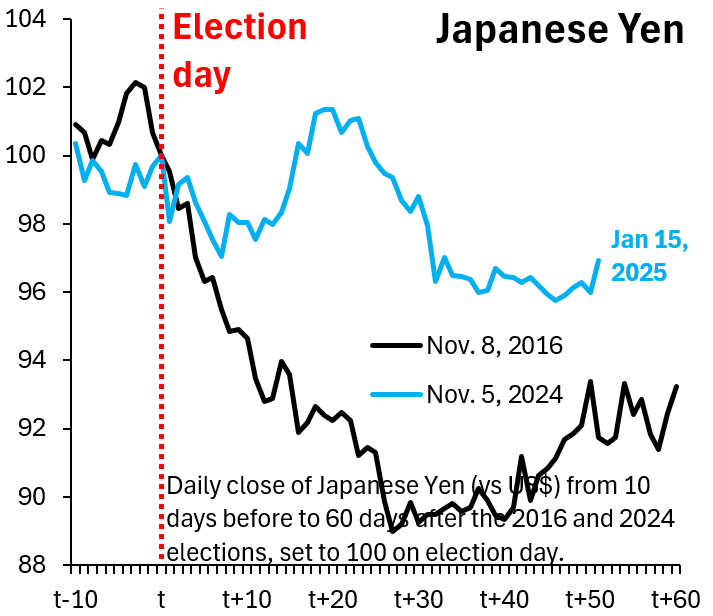

This is because the rise in the dollar is primarily against the euro and the British pound, while it has risen only modestly against China’s yuan (Figure 3), which has essentially been in a holding pattern since the election. Of course, some say that the yuan is subject to official intervention and may thus not be a good gauge for market positioning on tariffs. However, the Japanese yen sends the same signal. Japan would be severely impacted by additional U.S. tariffs on China, given that the resulting yuan depreciation would cause the yen to rise in trade-weighted terms. Such a rise would necessitate—in turn—a yen depreciation. Overall, it remains the case that markets are looking through tariff risk.

Figure 3. Daily close of Chinese yuan (vs. US dollar) from 10 days before to 60 days after the 2016 and 2024 elections, set to 100 on election day

Source: Bloomberg

Figure 4. Daily close of Japanese yen (vs. US dollar) from 10 days before to 60 days after the 2016 and 2024 elections, set to 100 on election day

Source: Bloomberg

How will China react to further US tariffs?

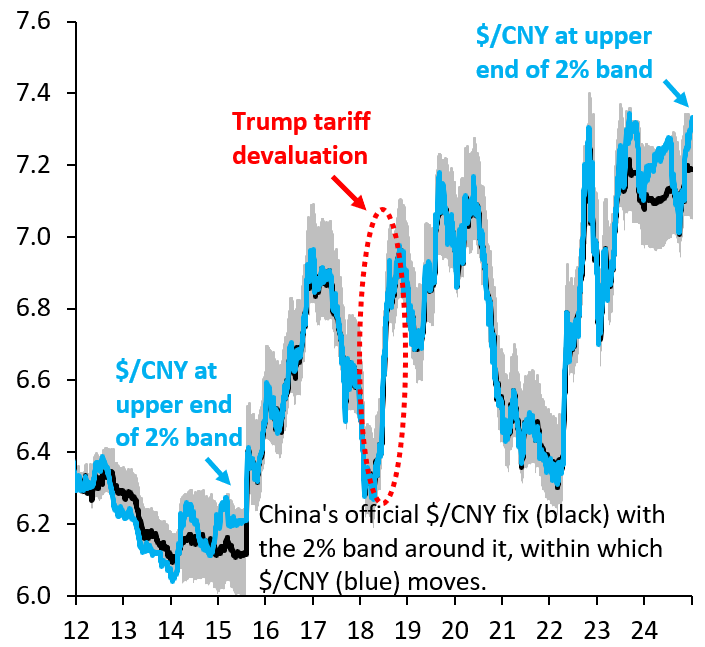

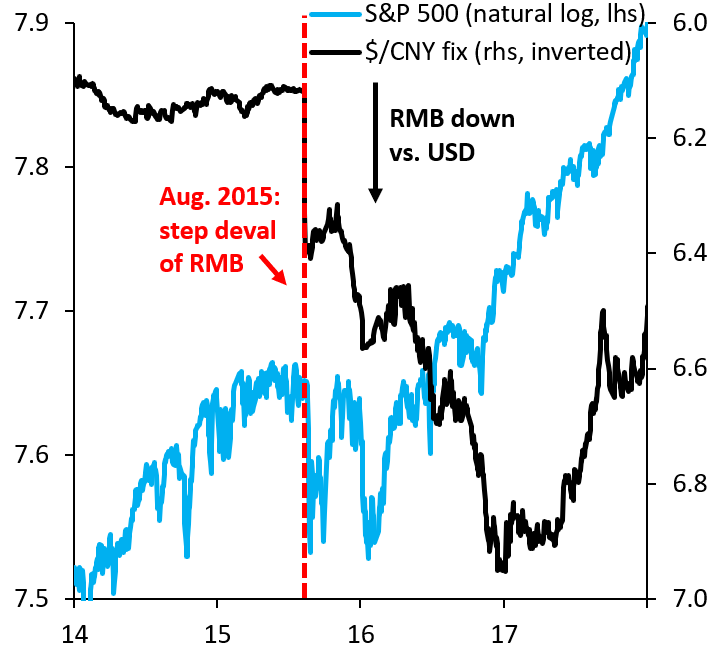

China’s most potent weapon in an escalating trade dispute is depreciation of its currency as an offset to U.S. tariffs. There is a precedent for this from 2018. Back then, the U.S. tariffed approximately half of all imports from China at a 25% rate, making the average tariff rate 12.5%. The yuan fell by almost that amount against the dollar in the months following tariff announcements (Figure 5), making for a de facto full offset via depreciation. 2018 ended with a sharp fall in the S&P 500 and prior instances of yuan depreciation—such as in August 2015 (Figure 6)—have also sparked declines in U.S. equities. Yuan depreciation therefore not only has the advantage of protecting China’s export sector from tariffs. It also harbors the potential for spillback to the U.S. by weighing on equities and thereby tightening financial conditions, something the incoming administration may not be happy to see.

Figure 5. China’s official $/CNY fix (black) with the 2% band around it, within which the $/CNY (blue) moves

Source: Bloomberg

Figure 6. Effects of the August 2015 step devaluation of the yuan

Source: Bloomberg

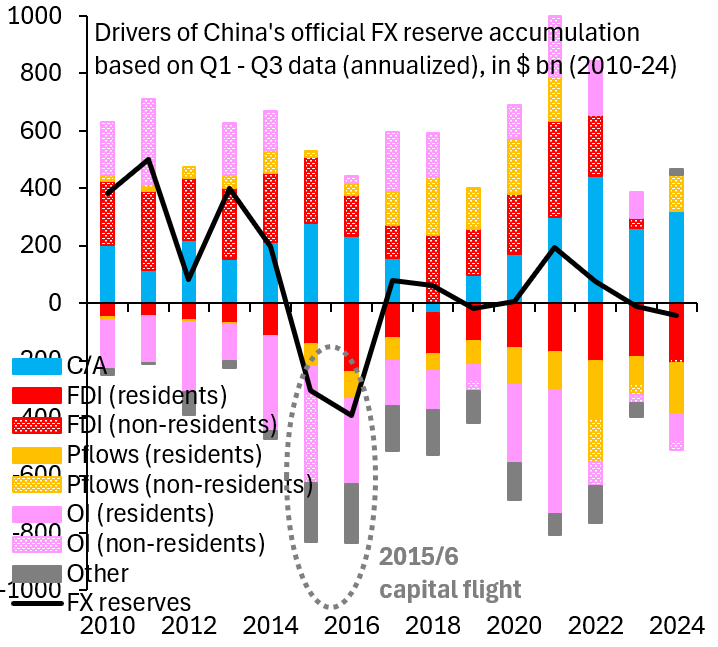

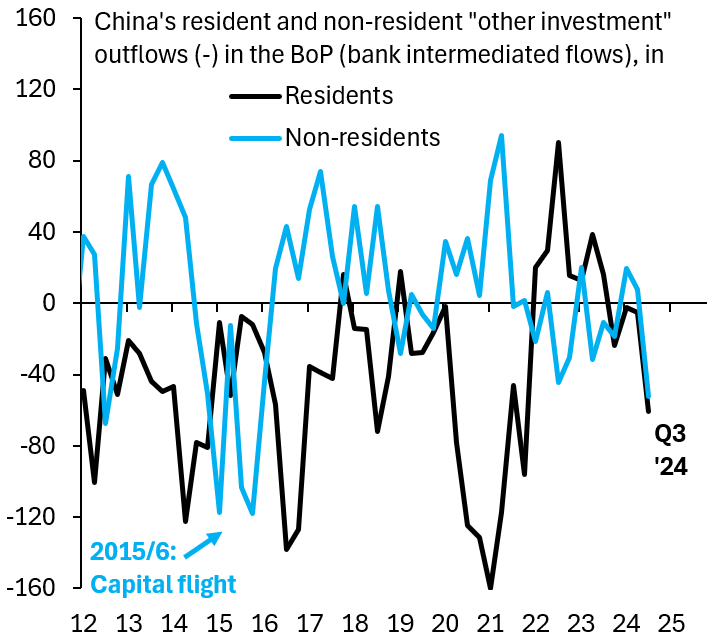

It is not clear if China’s leadership is willing to let the yuan fall substantially, especially if U.S. tariffs are large. The rigidity of the yuan against the dollar in recent years suggests China’s leadership may be averse to such a tactic, perhaps because it sees a stable yuan as a symbol of Chinese strength. Proponents of a large, up-front yuan depreciation will no doubt point to capital flight in 2015/6, when China fought yuan depreciation, which fanned capital flight as it allowed depreciation expectations to build in China’s asset-rich middle class (Figure 7). Indeed, there are some indications that such capital flight is building again. Nonresident other investment flows—bank intermediated carry trades—saw unusually large outflows in 2024 (Figure 8), reminiscent of 2015, when the carry trade similarly unwound. There is no sign that resident outflows are happening in any material size at this stage, but those also took longer to materialize during the 2015/6 capital flight episode.

Figure 7. Drivers of China’s official foreign exchange reserve accumulation based on Q1-Q3 data (annualized) in billions of dollars (2010-24)

Source: Haver Analytics

Figure 8. China’s resident and nonresident ‘other investment’ outflows (-) in the BoP (bank intermediated flows)

Source: Haver Analytics

The incoming U.S. administration may well try to preempt a large fall in the yuan by imposing sector-specific tariffs or—if it resorts to universal tariffs—phasing those in, with upward steps in the tariff rate linked to performance benchmarks on China. Regardless, the fact that markets price little tariff risk means coming months may well be volatile.

Related Content

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

China, tariffs, and Trump 2.0

January 16, 2025