Almost two years into the COVID-19 pandemic, supply chain disruptions are being felt acutely by producers and consumers around the world. Many are wondering whether this will provide a further impetus to realignments in global production. The pandemic has already had major impacts upon global foreign direct investment (FDI) flows, which plummeted by 35 percent in 2020.

Yet, the Western Balkan economies emerged less affected by this shock than other regions. Investment flows to the region contracted by only 12 percent in 2020, compared to a 73 percent decline in the EU. The region is experiencing a strong recovery in the current year, with FDI inflows to the Western Balkans growing by 20 percent year over year in the first half of 2021, beyond even 2019 levels. Some of this FDI may have been postponed investment that investors hesitated to undertake during the initial months of the pandemic, but the increased FDI inflows may also point to the region benefiting from potential nearshoring.

Is nearshoring really happening in the Western Balkans?

Nearshoring and reshoring trends in investment were already gaining traction in Europe before the pandemic and have been reinforced by the global supply chain and production disruptions it has caused. Unprecedented global shipping delays, rising labor costs in East Asia, and shifts in production technologies have prompted multinational firms to reduce overdependence on single locations for production and make their global value chains more resistant to external shocks. All these factors could point towards potential investments to diversify supply chain risks and bring production capacities closer to the European market. Given the Western Balkan economies’ geographic and cultural proximity to EU member countries; its well-educated, young, and multilingual workforce; and the relatively lower wages, the region is well positioned to benefit from potential nearshoring, as argued in the new Regular Economic Report on the Western Balkans.

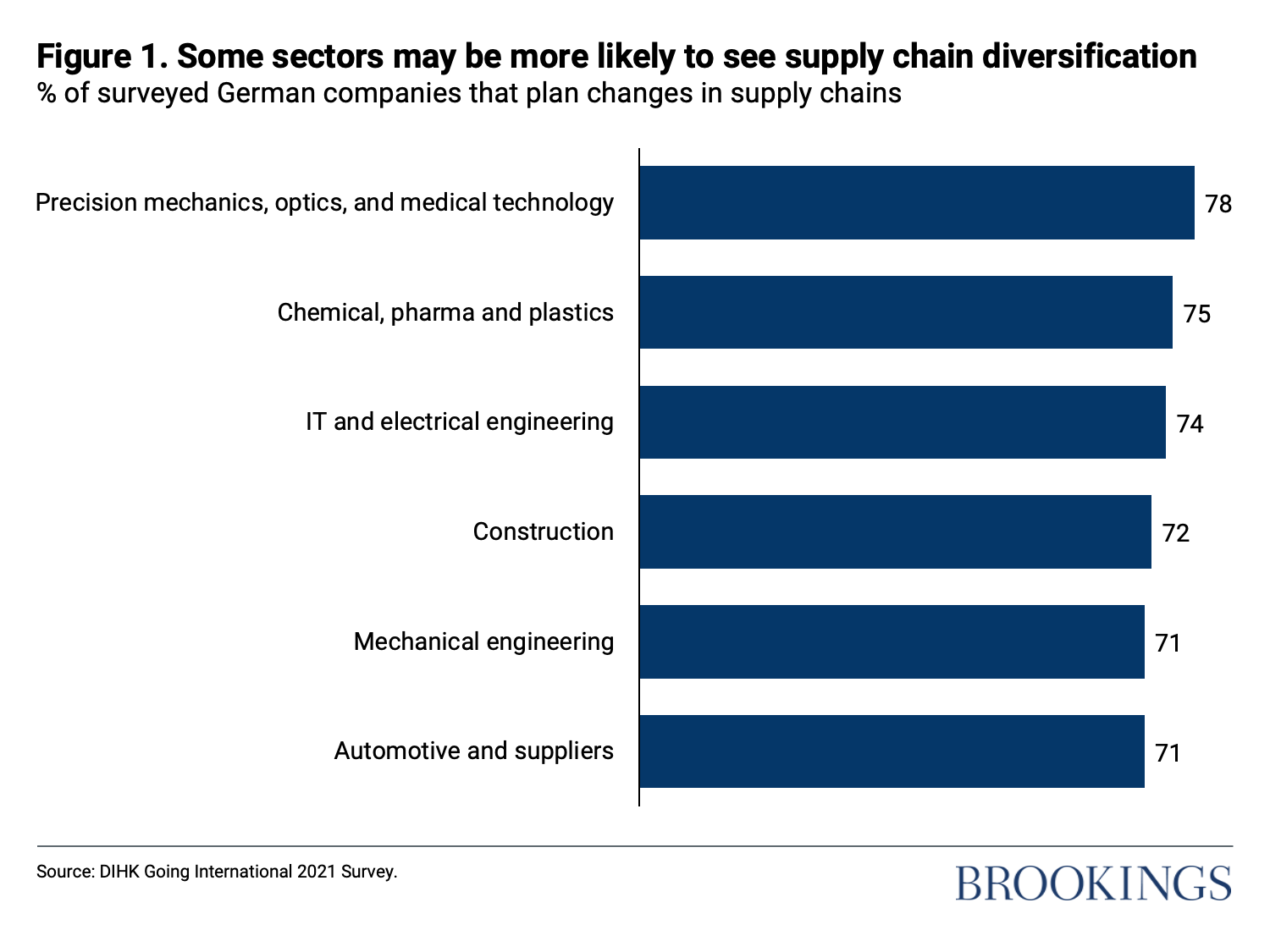

In fact, there are initial signs of nearshoring taking place in the region, including Italy’s fashion brand Benetton shifting production capacity from Asia to Serbia and Croatia amid soaring shipping costs and increasing lead times, and Japan’s Nidec Corporation announcing a $1.9 billion investment in Serbia to produce electric vehicles for the booming EU market. Evidence from business surveys paints a more nuanced picture of the likelihood and scale of potential nearshoring. While one survey finds significant potential for supply chain diversification, particularly in sectors such as precision mechanics, optics, medical technology, chemicals, pharmaceuticals, plastics, IT, electrical engineering, and automotive industries, other recent surveys point to limited evidence of significant changes to global value chains to date. As the pandemic is still not over and uncertainty remains, many companies may prefer to avoid disruptive and costly relocations at this stage. However, multinational firms do have a stronger appetite to reduce dependence on single or dominant source countries, and the longer that supply chain disruptions continue the more motivation they will have to diversify sourcing or turn to nearshoring. For the Western Balkans, given the relatively small size of their economies, even small-scale nearshoring could have a significant impact.

Proactive policy measures are needed to leverage the opportunity

To take full advantage of potential nearshoring opportunities, the region needs to implement ambitious reforms to strengthen its investment competitiveness. This includes addressing key binding constraints that hamper FDI, most notably shortages of skilled labor, inadequate infrastructure, and unpredictable governance. Governments need to reform their education systems, improve their regulatory environments, and enhance firm capabilities including improving access to finance for SMEs and developing domestic suppliers to FDI.

Related Books

Next, governments in the Western Balkans need to embrace proactive policies to attract investments in sectors with the potential for nearshoring. This will entail articulating the region’s value proposition to investors in those sectors and implementing targeted outreach programs aimed at investors in both the currently successful sectors and those with identified potential.

Finally, close alignment of the Western Balkans growth strategies with the EU’s Green Deal and the European Industrial Strategy will be needed to foster investments, particularly in green and sustainable sectors, as well as in key sectors supporting strategic European value chains.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Can COVID-19’s supply chain disruptions help Western Balkan competitiveness?

December 20, 2021