Below is Chapter 3 of the Foresight Africa 2017 report, which explores six overarching themes that provide opportunities for Africa to overcome its obstacles and spur inclusive growth. You can also join the conversation on Twitter using #ForesightAfrica.

Regulatory environment and technological innovation in Africa: Any tension?

Why is regulating technology important? Are regulations and the regulatory environment likely to stifle innovation in Africa? What regulations are appropriate and even helpful for innovation? How can governments balance out regulations and entrepreneurship? Is there tension between the regulators and innovators in Africa?

So far, nothing can elaborate on these questions better than the development, success, and spread of digital financial services (DFS) in Africa. In particular, Kenya’s M-Pesa (as well as similar products in Kenya and Tanzania), a mobile phone-based banking product and later a technological platform, has pushed the frontier of innovation and financial inclusion without compromising financial stability. Kenya’s combination of a supporting policy environment with a sound regulatory and supervisory framework allowed space for innovators and entrepreneurs to introduce financial innovations and a diversification of products into the market. Regulators agreed with the innovators on prudent risk management, and the policy environment ensured a stable macroeconomic environment. These combined factors ensured Kenya’s success. These are major outcomes that form a strong base for lessons for 2017 in the African continent as well as for Kenya to sustain the frontier and move to the next level.

Indeed, countries that have embraced digital financial inclusion and created a regulatory yet innovation-friendly environment have provided the guidelines to proactively shape market outcomes.

Indeed, countries that have embraced DFS and created a regulatory yet innovation-friendly environment have provided the guidelines to proactively shape market outcomes. This lesson has allowed innovators to successfully introduce new products into the market with new delivery channels and methods. Those countries have raised their financial inclusion profiles and created vibrancy in the financial market and the totality of their economies. Thus, different countries in Africa that have provided better regulatory environments even at extremes—such as the Kenyan case of “test-and-learn” approach—have found great success. The case is different for those countries that have not embraced the digital financial revolution; often their constraints can be traced to their prevailing regulatory environment, but not their prevailing legal frameworks.

The M-Pesa revolution and resulting technological platform developed in four innovative and virtuous stages, spurred by a conducive regulatory environment. First, the mobile phone platform was used for money transfer between users and later for payments and settlement—these uses were made easier and a rollout more possible in 2006 when the Kenyan government amended the communication law to recognize electronic units of money. The practicality of transforming cash into electronic units of cash, storing it on a SIM card, and simultaneously loading it into a bank account led to the development of a transactions platform in the absence of a national payments and settlement law. Second, encouraged by regulators, virtual savings accounts were developed using the same M-Pesa technological platform—impacting the banking intermediation process.

Third, the development and application of information capital (credit scores) for participants in this technological platform arose as companies started using the M-Pesa payment data including travel and communication patterns to determine the risk profile of customers and offer them loans at affordable rates, eliminating information asymmetry inhibiting the development of credit markets in Africa. This development was supported by already-existing credit information bureaus and amendments on information sharing to the Banking Act. Finally, cross-border payments and international remittances based on the M-Pesa technological platform have become possible aided by the National Payments Act, which allowed for standalone payments and settlement units including foreign exchange remittances. Now, the M-Pesa technological platform has revolutionized financial inclusion in Kenya to reach over 75 percent of the population and increase financial access touch points: 76.7 percent of the population are within five kilometers of a touch point, and there are 161.9 financial access touch points per 100,000 Kenyans compared to 63.1 in Uganda, 48.9 in Tanzania, and 11.4 in Nigeria.

Going forward, what can regulators in Africa do to encourage the innovation revolution?

Products like M-Pesa cannot thrive if the regulators on both sides do not understand the potential of the innovations taking place to the totality of the economy as well as the risks.

Products like M-Pesa cannot thrive if the regulators on both sides do not understand the potential of the innovations taking place to the totality of the economy as well as the risks, and provide risk mitigation processes upfront—thus avoiding stifling emerging innovative products. Other countries in Africa that have followed similar paths even with different legal frameworks have been successful. Rules and guidelines should encourage prudent behavior by both the financial institutions and market participants. Regulators should manage the orderly entry and exit of financial institutions in the market, minimizing the potential for major disruptions in the financial system. This did not change when other regulators, like telecommunication (telco) regulators in Kenya, came to the scene; in that example, it strengthened the case for DFS and provided credibility with regulators working as a team.

So far, this pattern has worked well, but DFS platforms have brought other actors that are regulated differently into the marketplace, such as the fintechs and the telecommunication companies partnering with banks to provide access to financial services. What happens now, when such partnerships require different regulators and regulatory technology? In this case, regulatory technology must develop further, cope, and align with these new product designs and market actors. In the Kenyan case, M-Pesa is like a joint product between commercial banks and a telco (Safaricom), and other similar products have been developed and rolled out to the market in a similar way. These types of products sit in a commercial bank as a transactions platform and the telcos provide the technological transmissions of transactions to this platform. The regulators of banks and telcos then concentrate their efforts and guidelines along these shared responsibilities.

For further progress and increased uptake of transformative innovations in 2017 what is required is further improvement in the regulatory environment.

For further progress and faster financial inclusion in Africa in 2017—as well as increased uptake of other transformative innovations—what is required is further improvement in the regulatory environment, regulatory reforms as well as leveraging on successful cases to make the financial market more accessible, efficient, safe, and reliable to boost confidence and endogenously move financial inclusion to the next level. It is emerging in this way for example in East Africa.

The lessons are clear that a poor regulatory environment can be a major obstacle to innovations in the market and will constrain the speed of financial inclusion. In this regard, we can scheme out the role of regulations and what we may regard as a good regulatory environment. First, regulatory changes are needed to enable successful adoption and adaptation of innovations. In successful cases of DFS, regulators in telecos, central banks, and even competition encouraged adoption and use by steering a favorable environment for new products and enhancing their credibility. Second, the regulatory environment as well as frontier regulatory technology being adapted in the financial sector improved financial inclusion. The success of financial inclusion and accessibility to the financial market is compatible with the developmental role of regulators in Africa. Finally, related policies must open and even encourage and incentivize the consumer base to take up the new technology. In the Kenyan case, by bringing the financially excluded into the banking system, it has enhanced consumer protection and has created a better environment for monitoring anti-money laundering (AML) and combating the financing of terrorism (CFT). More importantly, it has created a better environment for monetary policy.

From this example, we can also provide a more global picture of the urgency of such innovations and their potential for transforming the lives of millions. A McKinsey Global Institute Report (2016), Digital Finance for All: Powering Inclusive Growth in Emerging Economies,1 recently recounted some of the achievements of this new technology:

- Digital finance has the potential to provide access to financial services for 1.6 billion people—more than half of whom are women-—in emerging and developing economies.

- It can increase the volumes of loans extended to individuals and businesses by $2.1 trillion and allow governments to save $110 billion per year by reducing leakage in spending and tax revenues.

- Financial service providers can benefit by serving $400 billion annually in direct costs while sustainably increasing their balance sheets by as much as $4.2 trillion.

- The overall boost to GDP in these economies can be $2.7 trillion by 2025, a 6 percent increase. The contribution would come from raised productivity of financial and non-financial businesses and governments with DFS.

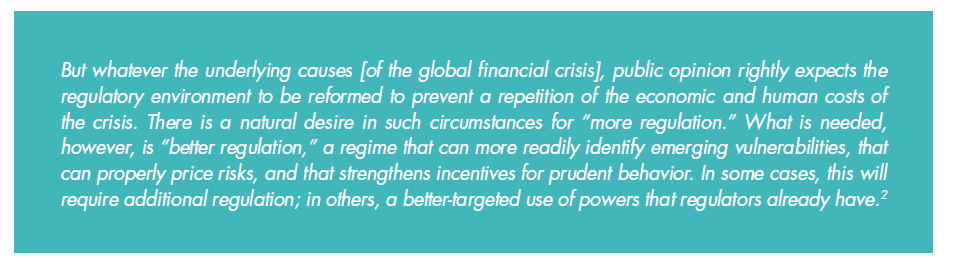

However, the fears of regulatory arbitrage, risks, and misunderstanding of how innovations are taking place continues to prevent so many African regulators from embracing DFS as well as creating an environment for other innovations in the market to thrive. The tension of regulation and innovation perhaps reigns even into 2017. What should be done? Going forward, how is the balance to be achieved? Nothing seems to explain this better than the words of the late Sir Andrew Crockett after the global financial crisis:

Institutions define the rules of the game, generating a set of dynamic principles to guide the market of dynamic innovators and entrepreneurs.

What results can we look for or showcase where the balance of regulation and innovation has been seen to work? Do we assume that in 2017 the regulators, especially in Africa, will acquire and adapt the frontier regulatory technology that will balance out and encourage innovation, innovative products, and entrepreneurship? The Kenyan case demonstrates that entrepreneurs and innovations will thrive with a supporting policy and regulatory environment. Its successes would not have been possible without the strong regulatory institutions as institutions have two important functions: First, they define the rules of the game, generating a set of dynamic principles to guide the market of dynamic innovators and entrepreneurs. Second, they define the appropriate incentives (as well as penalties). A combination of rules, dynamic guidelines, and appropriate incentives will encourage prudent behavior in the market and will support market development. In this regard, innovators and entrepreneurs will find it easy and rewarding to operate and thrive in such a market and a regulatory environment.

This synergy is what will support innovation in the market and attract new entrepreneurs. But there are two important caveats to watch for in 2017. Financial stability—like so many other important drivers of growth—cannot be sustained by regulations alone. Other internal and external factors, such as an unstable macroeconomic environment and threats of recession, can threaten success. Economic recession robs the economy of the supply of investment opportunities and the financial sector thrives on this dynamism to allocate financial resources to affect the investments. In addition, capping interest rates destroys the instrument that is used worldwide to price risk. In this case, domestic de-risking is bad for financial stability as well as encouraging innovation and entrepreneurs in the market. A regulatory approach and a regulatory environment that will encourage innovation and entrepreneurship is what African economies should strive to achieve in 2017 but also work on the pitfalls that can disrupt the process that will kill innovativeness and broad-based growth across sectors.

Related Content

2017

Additional Graphics

Author

-

Footnotes

- Manyika, J., Lund, S., Singer, M., White, O. and Berry, C. 2016. Digital Finance for All: Powering Inclusive Growth in Emerging Economies. McKinsey Global Institute. Available at: http://www.mckinsey.com/global-themes/employment-and-growth/how-digital-finance-could-boost-growth-in-emerging-economies.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).