Tax dispute resolution is a central component of the effective operation of any modern tax system. So, in 1997, Uganda established the Tax Appeals Tribunal (TAT) to provide taxpayers with access to an independent and impartial tax dispute resolution process. Its founders intended for the tribunal to improve voluntary tax compliance, ensure that everyone is treated equally under the law, and prevent a high amount of taxes from being held up in disputes.

Performance of the Tax Appeals Tribunal

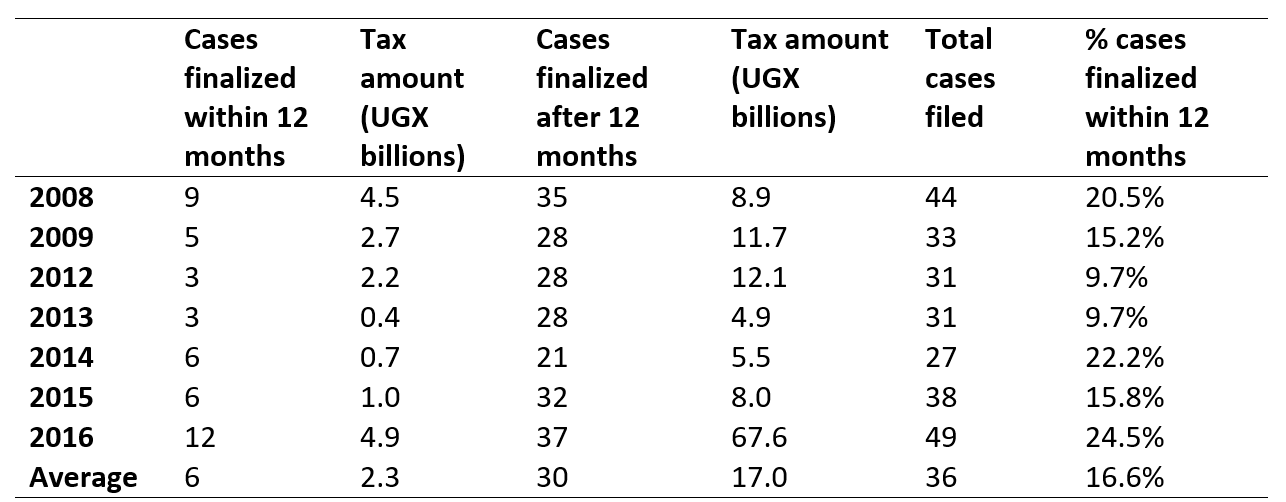

The implementation of the tribunal has run into several challenges that have inhibited its effectiveness. An estimated 1.1 trillion Ugandan shillings (UGX) ($297 million), an amount greater than the national budget allocation to the country’s agriculture sector, was held in dispute in 2017. Our recent study reveals that tax disputes have been resolved rather slowly, resulting in a backlog of outstanding disputes (Table 1). For instance, out of an average of 36 cases lodged from 2008 to 2016, only six disputes, worth UGX 2.3 billion ($621,621), were finalized within a year of filing.

Indeed, until a 2017 Supreme Court ruling reinforcing the TAT’s authority, disputing taxpayers were circumventing the tribunal and going directly to the High Court, where appeals ultimately go anyway, where there is no requirement for paying the 30 percent of the tax assessed (discussed below) in order to ask for a review, and where damages can get rewarded (they cannot at the TAT).

Several factors contribute to the high number of incomplete tax disputes, including a lack of performance targets (for example, a minimum number of cases to be finalized within a particular time) for the tribunal members, limited staffing, and the rigid requirement that a TAT ruling must be made by a member equivalent to a High Court judge. This restriction essentially requires the presence of the TAT chairperson for each and every hearing for a ruling to be made. This complication does not exist in other African countries like Kenya and Rwanda where any three members of the tax court can at any one time constitute the court for purposes of hearing a dispute. The requirement in Uganda not only delays dispute resolutions but could also lead to potential biases in decisions according to those familiar with the process.

Table 1: Tax dispute applications finalized by TAT

Source: Author’s computation using administrative data from TAT (UGX 3,700 = $1)

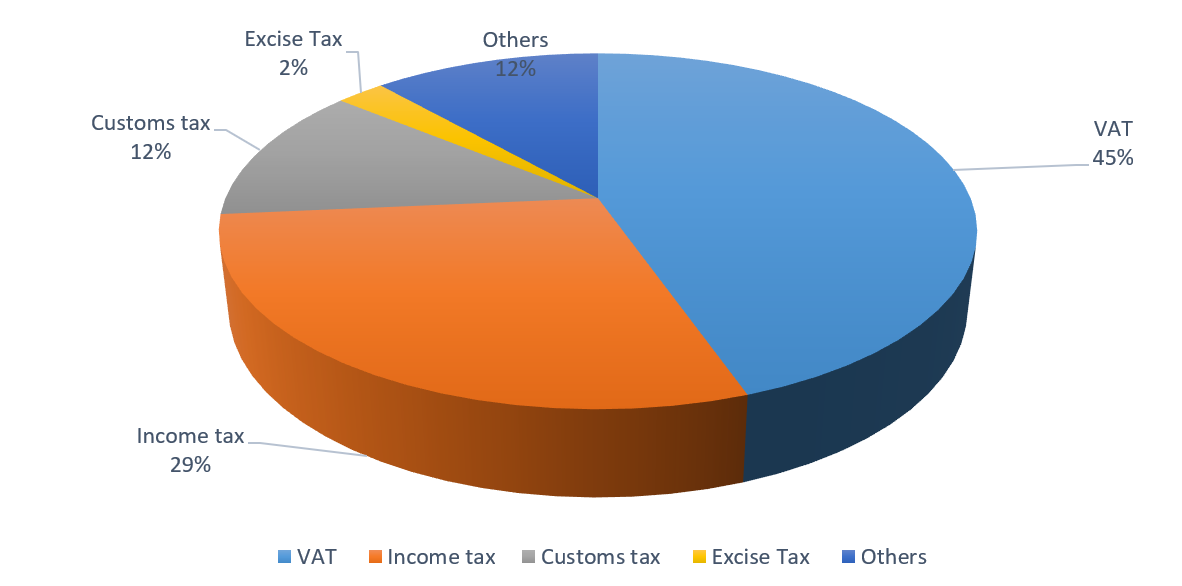

The value-added tax (45 percent) contributed almost half of all disputes in Uganda from 2008- 2016 (Figure 1). It was closely followed by income tax (29 percent) and customs tax (12 percent). The large share of both VAT- and income tax-related disputes is attributed to the granting of ad hoc tax exemptions, as well as continuous yearly adjustments of both VAT and income tax by the government to close revenue leakages and increase revenue scope. These acts are also too broad, which causes undue complexity and disputes.

Figure 1: Share of tax dispute applications lodged at TAT by tax head (2008-2016)

Source: Author’s computation using administrative data from TAT

Notably, while small taxpayers contribute a large share to the tax base in developing countries, the majority of tax disputes in Uganda are filed by the large taxpayers, implying that small taxpayers are unable to overcome the high barriers to accessing tax justice there. Indeed, small taxpayers are often unable to pay the mandatory 30 percent of the tax assessed or that part of the tax assessed not in dispute, whichever is greater as specified in the TAT Act. Second, they lack the necessary requirements for a formal TAT hearing. These include books of accounts, certificates of business registration, and representation by a tax lawyer. In addition, small taxpayers fear approaching the tax court because of the belief that the revenue agency may harass them.

Besides barriers for small taxpayers to access tax courts, tax disputes are commonly settled through mutual consent or withdrawn by taxpayers due to the lengthy legal bureaucratic process. Specifically, about 25 percent of the tax disputes lodged at TAT are either withdrawn or settled through mutual consent by applicants. This scenario is unlike in developed countries such as Australia, where only 6 percent of tax disputes are finalized by mutual consent. Currently, mediation as an alternative dispute resolution mechanism is not an option in dispute settlement at TAT. The large share of cases finalized through mutual consent and/or withdrawn suggests aggressive assessments and tax audits undertaken by Uganda Revenue Authority (URA) in order to meet annual revenue targets.

Facts of contestation in tax disputes

Ascertaining the facts that culminate in tax disputes is important for policy as it enables government to devise a joint solution for cases with similar causes. A critical review of 37 randomly selected finalized tax disputes spanning a period of 17 years reveals that the majority of tax disputes emanate from tax exemption-related issues (11 cases), and excessive and/or aggressive assessment by the URA (9 cases).

The major issues challenged at TAT as far as tax exemptions are concerned relate to ad hoc amendments of the VAT and Income Tax Acts that limit tax benefits to some taxpayers and/or items while denying others or granting different exemptions to items within the same sector of the economy. In addition, tax exemption-related disputes also originate from a lack of uniformity between tax exemptions and investment incentives offered to investors by Uganda’s investment agency, the Uganda Investment Authority. By minimizing ad hoc tax exemptions and limiting annual amendments that target the VAT and income tax laws, the government can minimize tax disputes. This goal can also be accomplished by streamlining tax incentives and exemptions for investors.

Considering extreme assessments by URA, disputes arise out of disagreements in the method of computation of penalties between taxpayers and URA. Additionally, taxpayers contest dismissal of their applications by courts (TAT and the High Court) due to inability to pay the mandatory 30 percent of the tax assessed or that part of the tax not in dispute whichever is greater, as stipulated in the TAT Act.

Gaps in the Tax Appeals Tribunal Act affecting tax dispute resolution

Our research highlighted three major key barriers to efficient operation of the TAT.

First, as we note above, the requirement for a taxpayer lodging a notice of objection to an assessment to pay 30 percent of the tax assessed or part of the tax assessed not in dispute, pending final resolution of the objection, creates a major barrier for many taxpayers in accessing the tribunal. (Despite a challenge in the Supreme Court, this fee still stands.) Importantly, this requirement not only affects taxpayers’ cash flows but tempts URA to raise excessive assessments in a bid to achieve their annual revenue collection targets.

Related Books

Second, the tribunal has no powers to award damages to successful parties. The tribunal currently only has powers to award costs. For a successful taxpayer to get damages, one must first file a fresh suit in the High Court for that purpose. This constraint is often a reason that taxpayers file tax-related matters to the High Court instead of the tribunal.

Third, the tribunal is unable to refer tax disputes for mediation. Mediation is important as it allows for faster and more amicable resolutions of disputes. It is therefore prudent that an amendment providing for mediation is added to the TAT Act as is in other courts of law.

Finally, the TAT Act is silent about the judicial responsibilities of the registrar. Therefore, amendments to the TAT Act are required to expressly enable the registrar to discharge judicial powers such as handling interim orders and taxing costs.

Policy recommendations

In light of these barriers, to improve and quicken tax dispute resolution, we recommend that the Ugandan government address the following three areas:

- Mediation as an alternative dispute resolution mechanism needs to be introduced in tax dispute settlement at TAT to reduce the escalating number of tax disputes finalized beyond 12 months of lodgment. Mediation allows for a faster and more amicable resolution of disputes.

- The government needs to minimize the frequency of amendment of tax laws especially VAT and income tax to reduce the undue complexity of tax laws that leads to disputes.

- The current jurisdiction of the tribunal should be widened to enable the tribunal to award damages to successful parties. This adjustment would eliminate the need for a successful party to file fresh suits in the High Court for purposes of obtaining award of damages.

Note: This blog reflects the views of the authors only and does not reflect the views of the Africa Growth Initiative.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Boosting domestic revenues through Tax Appeals Tribunals: Lessons from Uganda

May 15, 2019