On April 28, 2021, the Federal Open Market Committee (FOMC) reported that “inflation has risen, largely reflecting transitory factors.” The June, July, and September FOMC statements repeated this statement, even as inflation continued to rise. By late November, however, Chairman Jerome Powell suggested it was time to retire the “transitory” descriptor.

The description of inflation as “transitory” became highly politicized, especially as the term was adopted by members of the Biden administration. In May 2021, for example, Treasury Secretary Janet Yellen said: “I expect all of this to be transitory, and I think the economy’s going to get back on track. I don’t anticipate inflation is going to be a problem.” On Twitter, economists and commentators began using the hashtag #TeamTransitory to represent this administration-endorsed view of inflation. The opposing view, sometimes called #TeamPermanent or #TeamPersistent, was more often (though not exclusively) propounded by right-leaning economists and media.

To what extent did the #TeamTransitory versus #TeamPermanent debates shape and polarize the inflation expectations of the general public in 2021 and 2022? Consumer survey data show that Democrats’ inflation expectations remained virtually flat throughout 2021 and 2022, while Republicans’ expectations rose sharply. In other words, Democrats and Republicans sorted extensively into #TeamTransitory and #TeamPermanent.

As inflation began to rise in 2021, Fed officials monitored survey measures of consumer inflation expectations to gauge the extent to which inflation expectations were anchored and to calibrate their policy response. But there is no consensus about the usefulness of these survey measures—the extent to which they represent consumers’ “true” inflation expectations, and help predict future inflation. The growing partisan gap in survey-reported inflation expectations is reason to use caution when interpreting the survey data.

Data

The University of Michigan Survey of Consumers asks about inflation expectations over the next twelve months (short-run expectations) and over the next five to ten years (long-run expectations).

The Michigan Survey asked respondents about their political party affiliation sporadically in 2006 through 2016. Beginning in February 2017, partisan affiliation has been solicited every month. Respondents can report that they are a Republican, a Democrat, or an Independent/no preference. Only about 3% of respondents say that they don’t know or provide no response. Respondents who report an affiliation with the Republican or Democratic party are also asked if they are a “strong” or “not-so-strong” Republican or Democrat.

Partisan Expectations

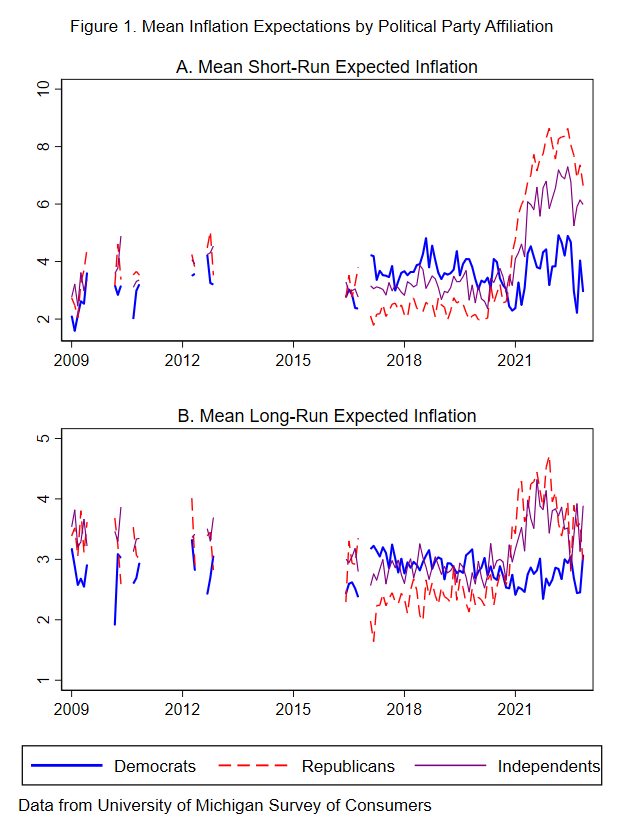

Figure 1 plots the mean short-run and long-run inflation expectations of Democrats, Republicans, and Independents from 2016 through 2022. As previous studies have found, consumers typically have lower inflation expectations when their preferred party is in control of the White House. This likely reflects many consumers’ tendency to associate “good times” in general with low inflation. During the Barack Obama presidency, Republicans had higher inflation expectations than Democrats. This partisan gap reversed when Donald Trump was elected. Democrats’ short-run inflation expectations were about 1.3 percentage points higher than Republicans’ throughout the Trump presidency. Their long-run expectations were about 0.5 percentage points higher.

When Joe Biden was elected, the partisan gap reversed again. And as inflation rose, the gap began to widen. By the end of 2021, the short-run inflation expectations of Republicans were 5.5 percentage points higher than those of Democrats. Long-run inflation expectations of Republicans were 2.1 percentage points higher than those of Democrats. Expectations of Independents remained in between those of Democrats and Republicans, but closer to those of Republicans, especially for the longer horizon.

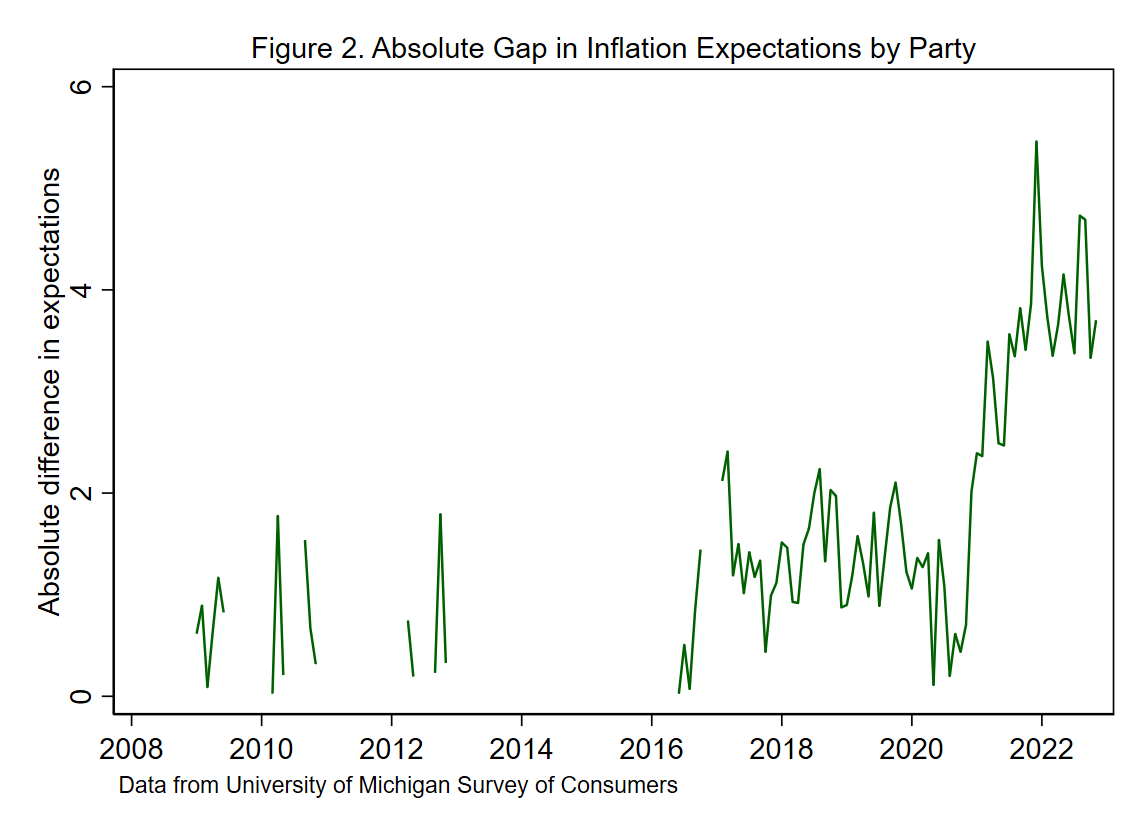

Figure 2 shows the magnitude of the partisan gap in short-run inflation expectations over time. The gap was less than two percentage points for most of the Obama and Trump eras, and for the start of the Biden era. But it has more than doubled in the last two years.

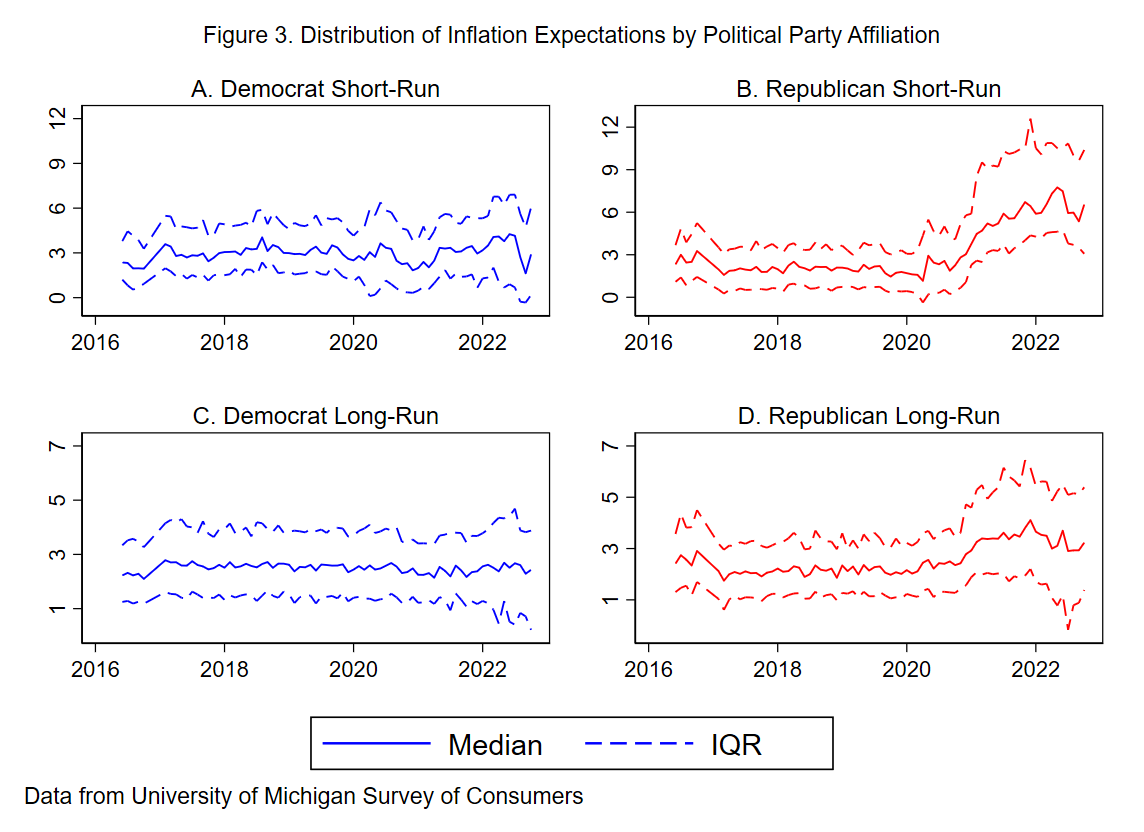

These growing partisan gaps are not driven by outliers. Rather, the entire distribution of Democrats’ inflation expectations remained virtually unchanged in 2021 and 2022, while the distribution of Republicans’ expectations shifted upward. Figure 3 plots the median and interquartile range of expectations (the middle two quartiles) by political party over time. For Democrats, no part of the distribution of expectations shifted upwards in 2021 or 2022, for either the short or long horizon. In other words, Democrats were nearly universally on #TeamTransitory.

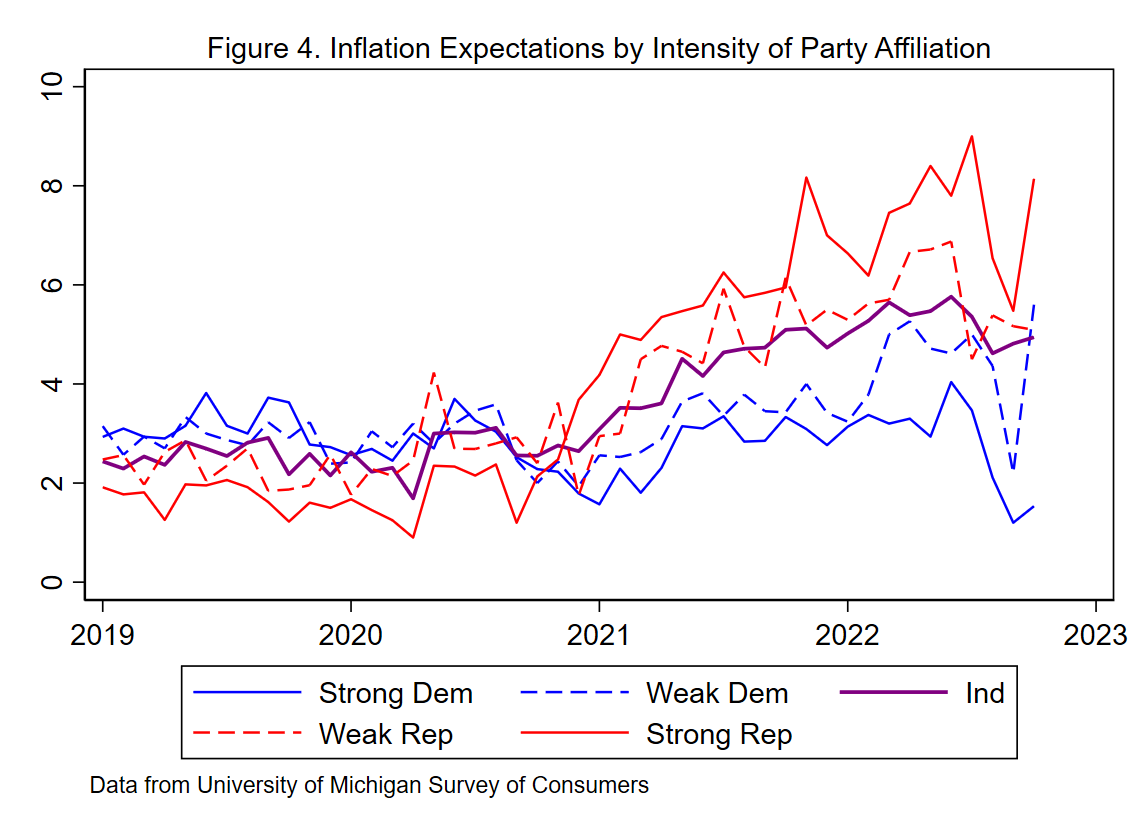

Figure 4 shows median one-year inflation expectations since 2019 by party affiliation and intensity. Before the Biden election, strong and weak Democrats had similar inflation expectations. The expectations of Independents and weak Republicans were also similar, and strong Republicans had slightly lower expectations. As the partisan gap widened during the Biden administration, gaps by intensity of party affiliation also widened. The expectations of Independents and weak Republicans remained similar, but strong Democrats’ expectations were more than a percentage point lower than weak Democrats’ expectations in 2022, and the gap between weak and strong Republicans’ expectations likewise expanded.

A Policy Challenge

If Democrats and Republicans really had such drastically different inflation expectations throughout 2021 and 2022, they should have made very different investment and consumption decisions. Future research could test whether this was the case. Alternatively, partisan survey respondents may be signaling their politics, rather than their true expectations, when reporting their inflation expectations. In this case, overreliance on survey measures of expectations could add noise to the policymaking process.

Related Content

2022

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Political party affiliation and inflation expectations

January 9, 2023