Introduction

Last month, the Biden administration made headlines nominating Cornell Law School Professor Saule Omarova to serve as Comptroller of the Currency, a position from which she would oversee the National Banking System. Omarova’s nomination has drawn sharp criticism from the financial services industry, placing her alongside other Biden appointments within financial regulation such as chair of the Securities and Exchange Commission Gary Gensler and director of the Consumer Financial Protection Bureau (CFPB) Rohit Chopra. In each case, the appointments represent a sea change, embracing an approach to regulation that starkly differs from the priorities of the Trump administration. These existing appointments and nominations set the stage for the financial regulatory appointments that the administration has not yet made, including three vacancies on the Federal Reserve — the Fed Chair, Vice Chair for Supervision, and a member of Fed’s Board of Governors —and vacancies at the Federal Deposit Insurance Corp (FDIC), among others.

Debate over these key personnel focus on different visions of regulation, the rules political appointees write that apply to the entire financial system. These include what financial regulation should do about climate change, how it should support under-represented minorities, how it can ensure financial stability, and much more. But the biggest piece of the puzzle is still missing: these agencies and appointments also control the supervision of the financial system, not just its regulation. The difference between these two concepts is very important. If regulation sets the rules of the road, supervision is the process that ensures obedience to these rules (and sometimes to norms that exist outside these rules entirely). Regulation is the highly choreographed process of generating public engagement in the creation of rules. Supervision is the mostly secret process of managing the public and private responsibilities over the risks that the financial system generates.

Political groups organize in support or opposition of various regulatory nominees usually on the basis of the candidates’ perceived regulatory priorities. This is important, but this exclusive focus is a mistake. We, all of us, should pay far more attention to the candidates’ vision and philosophy of supervision. This part of the public vetting is all the more important given the culture of secrecy that surrounds bank supervision. If the public is going to have a say in the kind of supervisory system we should have, then the appointment process is likely the first and last chance to do it.

The question for senators who provide advice and consent necessary to obtain these jobs and for the general public in vetting these candidates for appointment should focus on how these nominees view the tradeoffs inherent in the supervisory process wholly independent of financial regulation. It should focus on what they will do—now—to maintain the culture of supervision or to change it.

What Supervision Means

The idea that supervision and regulation should receive separate priorities is not new. More recently, in contemporary debates, some view supervision as part of a long-standing settlement of monetary questions of special relevance during the Civil War, others as the implementation of regulatory priorities, others as a kind of regulatory monitoring. We view it differently. While many of these conceptions of supervision capture elements of what makes this mode of public governance so unusual, the full picture is more historically contingent and flexibly comprehensive. In our view, supervision is the management of residual risk at the boundary of public and private, the space where private banks and public officials sometimes spar, sometimes collaborate, over responsibility over the financial system. Because risks in the financial system are constantly evolving, supervision has done the same.

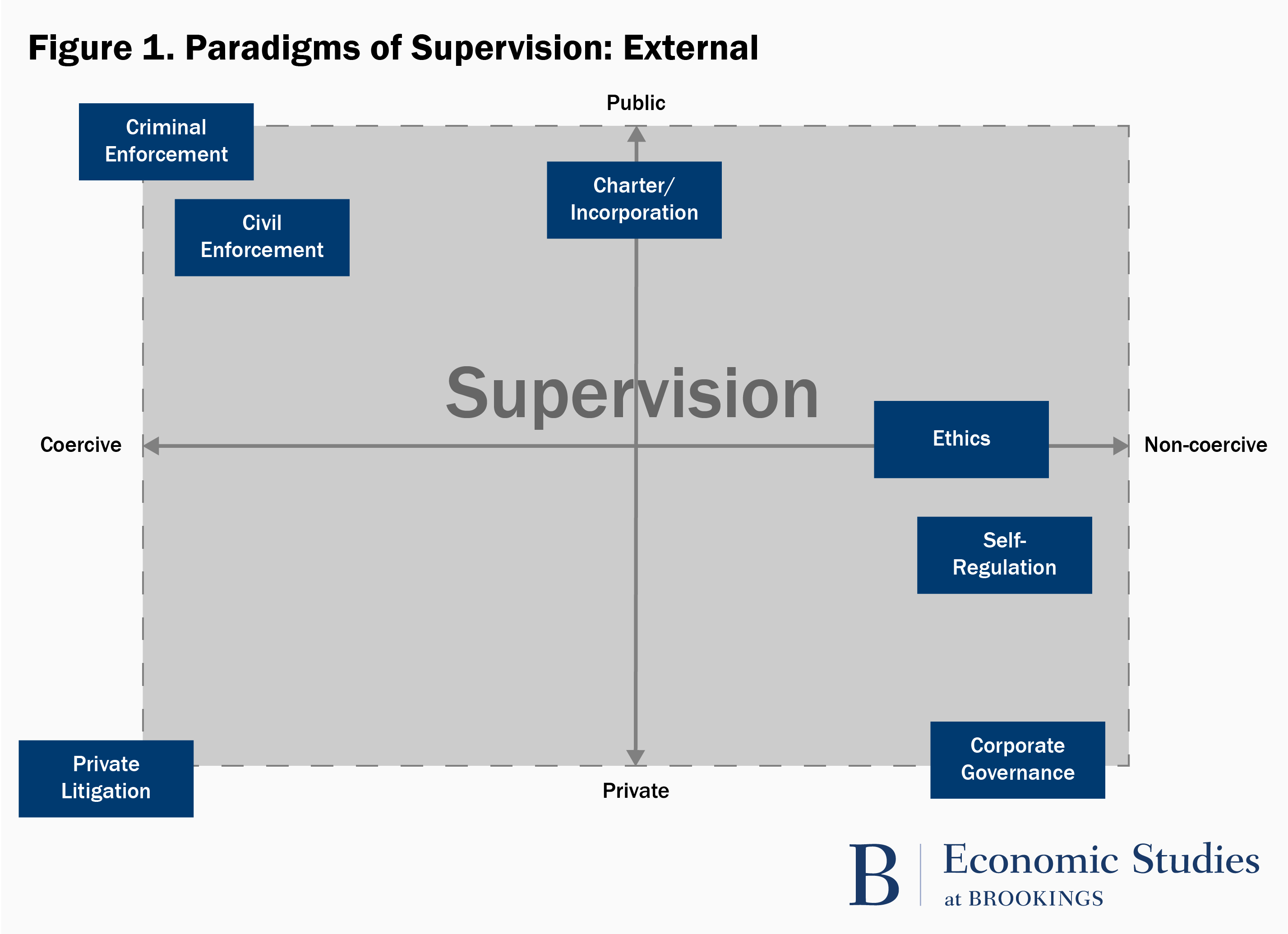

In our work on the history of bank supervision, we offer a typology that captures this range of functions. The typology has two parts. First, supervision functions as a distinct mechanism of legal obedience—a means by which government or private actors seek to alter bank behavior. These mechanisms can be displayed on two axes, between public and private mechanisms, which require the exercise of coercive and non-coercive power.

In this sense, supervision represents a choice for policymakers, distinct from other alternatives. It is a choice, as the graphic indicates, which authorizes government officials to exercise substantial discretion about how to alter behavior.

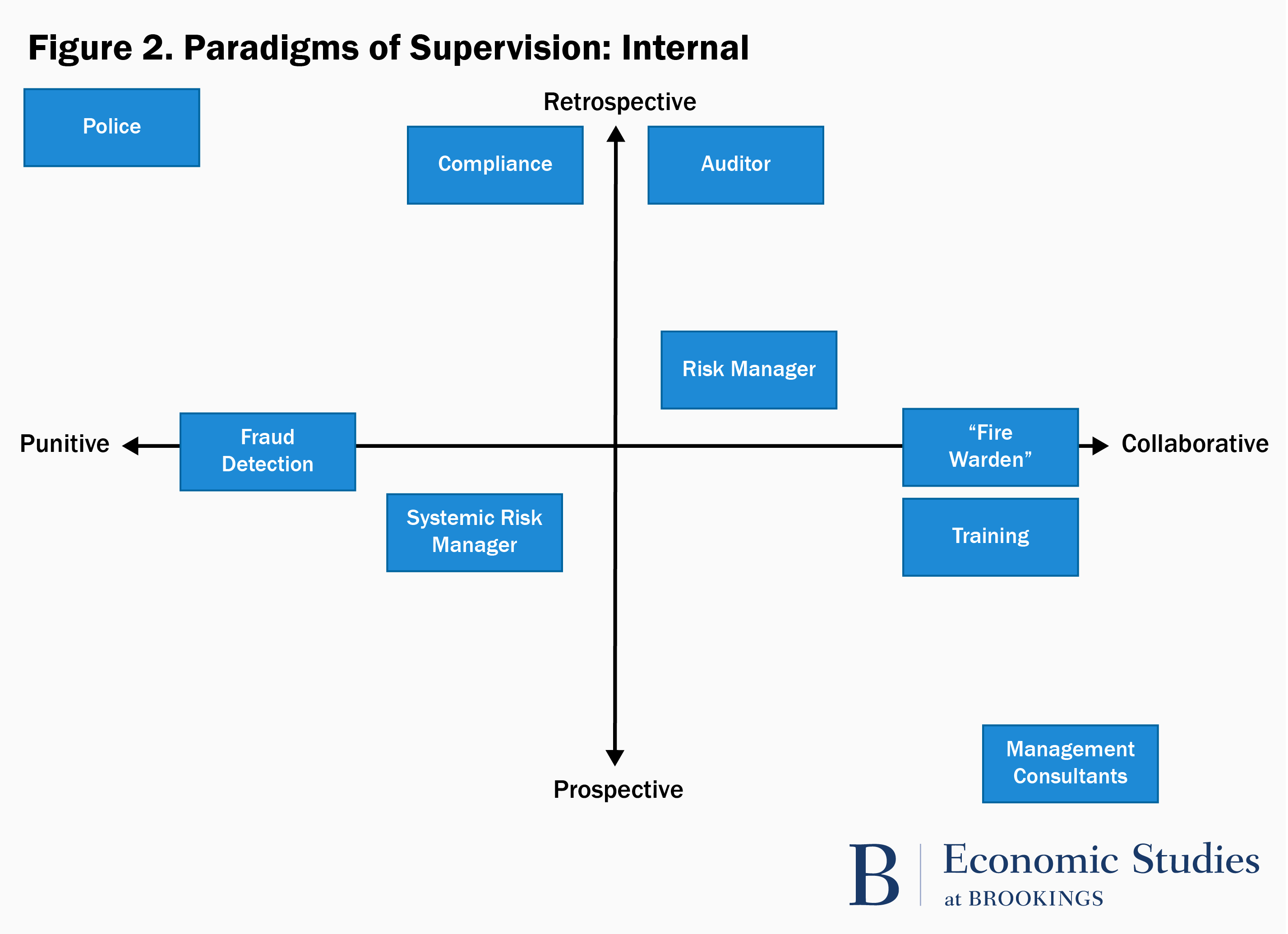

Relatedly, what supervision looks like on the ground depends almost entirely on what supervisors think they are trying to accomplish, self-conceptions that divide not only according to an external logic of coercion vs. non-coercion and public vs. private but also an internal one. These self-conceptions operate within a framework with axes spanning punitive to collaborative and from retrospective to prospective, as summarized in Figure 2.

Together, the two typologies indicate a range of possible supervisory actions (external) and the motivations behind such actions (internal). They imply constant trade-offs that supervisors must make as they share risk management responsibilities with participants in the private sector. Despite the extraordinary flexibility that this model of supervision permits, supervisors cannot hold all ground at once and be all things to all people. They must choose and in choosing navigate the often conflicting and sometimes contradictory policy goals placed by Congress on bank supervisors: between safety and soundness and firm competitiveness, between consumer protection and facilitation of financial innovation, between punitive and collaborative approaches, and many others.

When a new public official is appointed to lead one of the major elements of bank supervision, she inherits a toolbox with many different kinds of tools. Members of Congress should ask nominees which tools they prefer for which kinds of jobs, how they view these trade-offs and what they would prioritize, and how they think about alternatives. A short-hand method is to listen for the metaphors nominees use to describe supervision. Do nominees conceive of supervisors as cops on the beat? As fire wardens? As referees and umpires? As compliance officers? As management consultants? Are banks their customers? What tools will they use in accomplishing this vision? What flexibility will they use and under what circumstances?

Who Supervisors Are

Because supervision is fundamentally flexible and evolving, personnel decisions are vital. Supervisory officials—independent of legislative and regulatory processes—constantly reshape the methods, tools, and rationales of supervision in relation to their understandings of financial risk and their evaluation of relevant policy tradeoffs.

History provides rich examples of this process. Looking back to the nineteenth century, comptrollers, and later officials at the Federal Reserve and FDIC, created supervisory bureaucracies with little congressional guidance on how those bureaucracies should be structured. In doing so, they crafted supervisory tools, like standardized examination forms or “schools” of supervision complete with simulated banks getting practice exams, which guided frontline agency staff and bankers through the thicket of managing residual financial risk. Sometimes appointees proved too lenient or too eager to encourage bank chartering and growth at the expense of systemic safety. At other times they proved too harsh, making a theatrical display of cracking down on shoddy bank oversight and in doing so potentially undermining agency credibility with bankers who doubt supervisors’ intentions.

Two recent examples highlight the ways conceptions of supervisory purpose translate into agency action. First, the CFBP emerged in the wake of the 2008 financial crisis in part because existing supervisory agencies tended to sacrifice consumer protection. In its early years, the architects of the CFPB adopted Senator Elizabeth Warren’s “cop on the beat” approach, bringing enforcement lawyers to routine exams even when there was no enforcement action pending. Thus, while other agencies tended to have a collaborative and prospective view of consumer protection—identifying potential problems and helping bankers navigate past them—the CFPB was looking to punish past mistakes and ensure compliance in the future. Bankers struggled to reconcile the agency’s seemingly contradictory positions. The enforcement attorneys left the examination teams, but the tone set from the top continued to be decisively important. Under Democrat Richard Cordray, the CFPB leveled more than $5.5 million in fines a day compared to slightly less than $2 million per day under Trump appointee Kathy Kraninger. The CFPB used civil enforcement aggressively and then didn’t.

Second, the design and implementation of stress tests for the nation’s largest, most systemically important banks has also undergone significant change at the hands of Federal Reserve appointees Dan Tarullo and Randy Quarles. There is much that is purely regulatory about these changes—the pace of stress tests, the reliance on qualitative versus quantitative metrics. But stress tests are ultimately a supervisory activity leaving a huge amount of space for supervisors to shape individual responses to idiosyncratic factors. The question for a new head of an agency is not simply what regulatory rules will govern stress tests but how that official thinks supervisory interactions with individual banks through the stress test process should occur.

Finally, changes in the approach to and methods of supervision seldom spring fully-formed from the head of a Senate-confirmed nominee. Rather, supervisory officials must also develop plans for recruiting, training, and retaining a superb corps of supervisors who can be independent of banks but also expert at managing those relationships to alter bank behavior. In doing so, they face two challenges. First, political appointees necessarily take the helm of an unwieldy ship. Frontline supervisors are in place and working hard in offices across the country. They have methods, routines, and ingrained expectations developed over years of experience and training by distant political appointees whose visions and ideologies of supervision may have been repudiated by a recent election. Supervisory leaders must have a strategy for learning their agencies’ bearing and changing course as necessary. They must do so, secondly, while holding onto experienced staff who may be attracted to the lure of more lucrative private-sector jobs. Retaining and retraining staff is a signature challenge of bank supervision. Senators should inquire about nominees’ plans for doing so.

Ten questions policymakers should ask

If Biden administration officials and senators heed our calls to take supervision seriously, then there are a number of questions they should direct to candidates and nominees alike.

- What do you see as the purpose of supervision? What is the supervisory agency’s primary role? What, if any, secondary goals would you emphasize?

- How would you plan to balance the inherent trade-offs between these goals? How would this balance differ—if at all—from your predecessor?

- Which supervisory tools do you view as most important for accomplishing these goals? How would you use these tools differently than your predecessors?

- How do you plan to learn about the existing supervisory culture at your agency? How do you plan to realign that culture around your goals?

- How will you recruit, train, and retain supervisory staff?

- How will you organize your office such that regulatory and supervisory functions inform each other but do not absorb each other?

- How do you plan to work with other bank supervisory agencies—at the federal level, internationally, and in the states? Do you see these other agencies as competitors or collaborators?

- What is the relationship between supervision and enforcement in your agency? How will you manage the process through which supervisors learn sensitive information that may be relevant to an enforcement action but that may also be an opportunity to change bank behavior without enforcement?

- How will you ensure that bank supervisors do not unduly adopt the point of view of the banks supervised?

- How will you ensure that bank supervisors understand the point of view of the banks supervised?

Although regulatory issues such as climate change, federal bank chartering, diversity, and fintech dominate conversations about regulatory appointments, a lack of focus on supervisory issues comes at a great cost to public governance and financial stability. Fights over regulation that ignore supervision may obscure these critical issues more than they illuminate. Bank supervision is an unusual set of institutions, homegrown in the United States and refined by federalism, financial crisis, and historical accident. Supervision remains the most important tool in the federal administrative toolkit for changing the way we understand the business of banking. The process of public governance should give it its due.

The Brookings Institution is financed through the support of a diverse array of foundations, corporations, governments, individuals, as well as an endowment. A list of donors can be found in our annual reports published online here. The findings, interpretations, and conclusions in this report are solely those of its author(s) and are not influenced by any donation.

Sean Vanatta is a Lecturer in U.S. Economic and Social History at the University of Glasgow, and an un-paid member of the Federal Reserve Archival System for Economic Research (FRASER) Advisory Board. The authors did not receive financial support from any firm or person for this article or from any firm or person with a financial or political interest in this article. Other than the aforementioned, they are currently not an officer, director, or board member of any organization with an interest in this article.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).