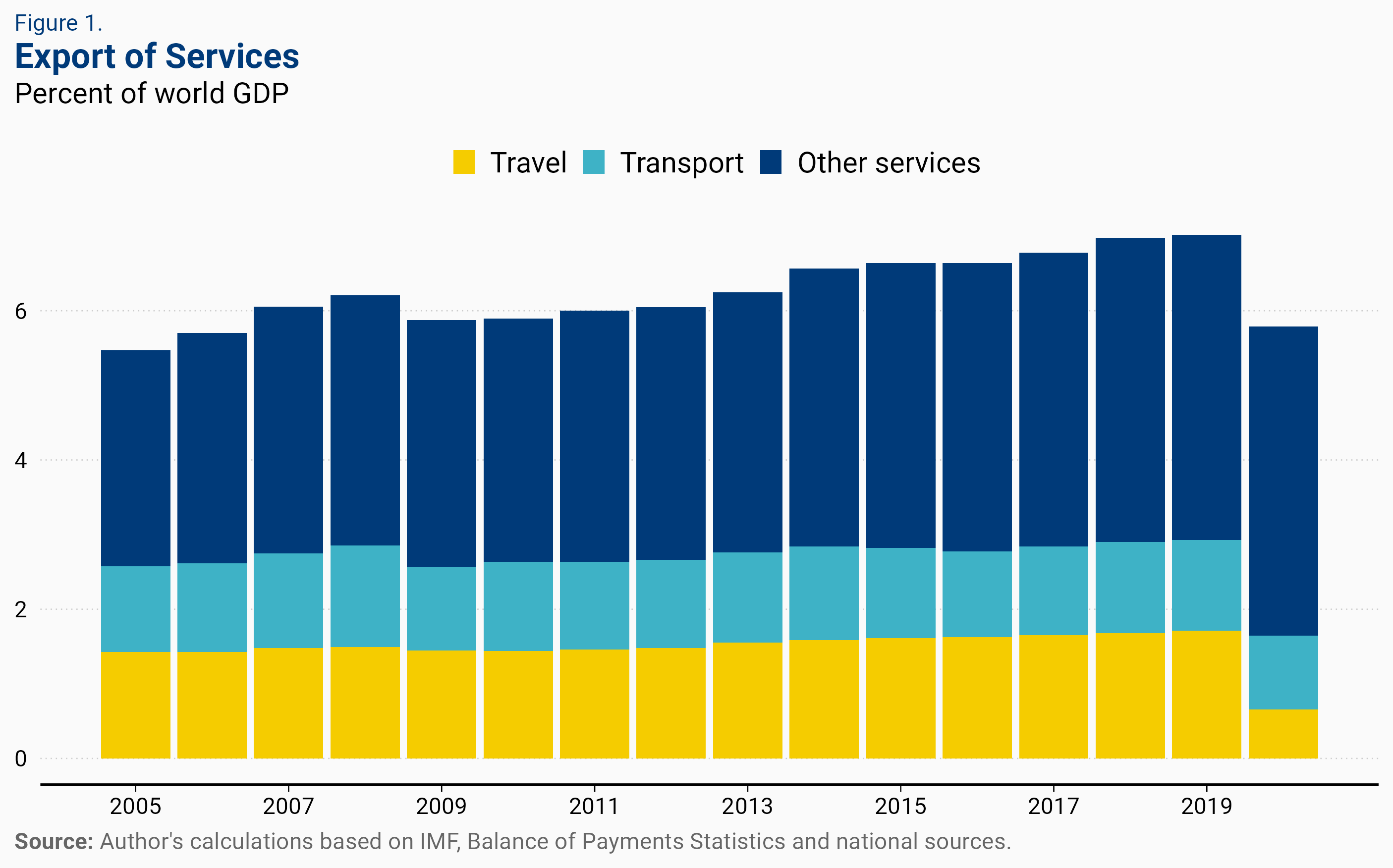

The COVID crisis has led to a collapse in international travel. According to the World Tourism Organization, international tourist arrivals declined globally by 73 percent in 2020, with 1 billion fewer travelers compared to 2019, putting in jeopardy between 100 and 120 million direct tourism jobs. This has led to massive losses in international revenues for tourism-dependent economies: specifically, a collapse in exports of travel services (money spent by nonresident visitors in a country) and a decline in exports of transport services (such as airline revenues from tickets sold to nonresidents).

This “travel shock” is continuing in 2021, as restrictions to international travel persist—tourist arrivals for January-May 2021 are down a further 65 percent from the same period in 2020, and there is substantial uncertainty on the nature and timing of a tourism recovery.

We study the economic impact of the international travel shock during 2020, particularly the severity of the hit to countries very dependent on tourism. Our main result is that on a cross-country basis, the share of tourism activities in GDP is the single most important predictor of the growth shortfall in 2020 triggered by the COVID-19 crisis (relative to pre-pandemic IMF forecasts), even when compared to measures of the severity of the pandemic. For instance, Grenada and Macao had very few recorded COVID cases in relation to their population size and no COVID-related deaths in 2020—yet their GDP contracted by 13 percent and 56 percent, respectively.

International tourism destinations and tourism sources

Countries that rely heavily on tourism, and in particular international travelers, tend to be small, have GDP per capita in the middle-income and high-income range, and are preponderately net debtors. Many are small island economies—Jamaica and St. Lucia in the Caribbean, Cyprus and Malta in the Mediterranean, the Maldives and Seychelles in the Indian Ocean, or Fiji and Samoa in the Pacific. Prior to the COVID pandemic, median annual net revenues from international tourism (spending by foreign tourists in the country minus tourism spending by domestic residents overseas) in these island economies were about one quarter of GDP, with peaks around 50 percent of GDP, such as Aruba and the Maldives.

But there are larger economies heavily reliant on international tourism. For instance, in Croatia average net international tourism revenues from 2015-2019 exceeded 15 percent of GDP, 8 percent in the Dominican Republic and Thailand, 7 percent in Greece, and 5 percent in Portugal. The most extreme example is Macao, where net revenues from international travel and tourism were around 68 percent of GDP during 2015-19. Even in dollar terms, Macao’s net revenues from tourism were the fourth highest in the world, after the U.S., Spain, and Thailand.

In contrast, for countries that are net importers of travel and tourism services—that is, countries whose residents travel widely abroad relative to foreign travelers visiting the country—the importance of such spending is generally much smaller as a share of GDP. In absolute terms, the largest importer of travel services is China (over $200 billion, or 1.7 percent of GDP on average during 2015-19), followed by Germany and Russia. The GDP impact for these economies of a sharp reduction in tourism outlays overseas is hence relatively contained, but it can have very large implications on the smaller economies their tourists travel to—a prime example being Macao for Chinese travelers.

How did tourism-dependent economies cope with the disappearance of a large share of their international revenues in 2020? They were forced to borrow more from abroad (technically, their current account deficit widened, or their surplus shrank), but also reduced net international spending in other categories. Imports of goods declined (reflecting both a contraction in domestic demand and a decline in tourism inputs such as imported food and energy) and payments to foreign creditors were lower, reflecting the decline in returns for foreign-owned hotel infrastructure.

The growth shock

We then examine whether countries more dependent on tourism suffered a bigger shock to economic activity in 2020 than other countries, measuring this shock as the difference between growth outcomes in 2020 and IMF growth forecasts as of January 2020, just prior to the pandemic. Our measure of the overall importance of tourism is the share of GDP accounted for by tourism-related activity over the 5 years preceding the pandemic, assembled by the World Travel and Tourism Council and disseminated by the World Bank. This measure takes into account the importance of domestic tourism as well as international tourism.

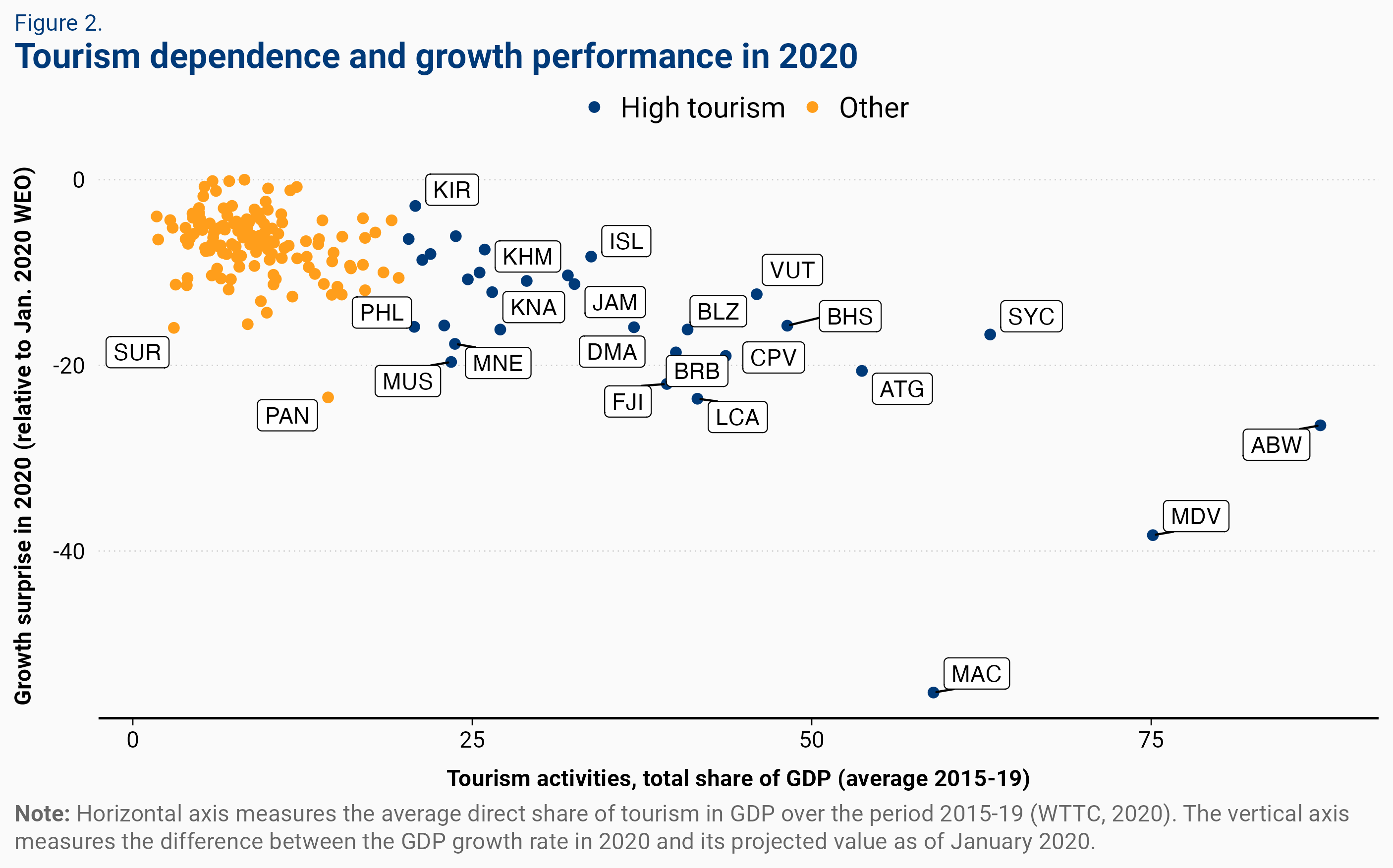

Among the 40 countries with the largest share of tourism in GDP, the median size of growth shortfall compared to pre-COVID projections was around 11 percent, as against 6 percent for countries less dependent on tourism. For instance, in the tourism-dependent group, Greece, which was expected to grow by 2.3 percent in 2020, shrunk by over 8 percent, while in the other group, Germany, which was expected to grow by around 1 percent, shrunk by 4.8 percent. The scatter plot of Figure 2 provides more striking visual evidence of a negative correlation (-0.72) between tourism dependence and the growth shock in 2020.

Of course, many other factors may have affected differences in performance across economies—for instance, the intensity of the pandemic as well as the stringency of the associated lockdowns. We therefore build a simple statistical model that relates the “growth shock” in 2020 to these factors alongside our tourism variable, and also takes into account other potentially relevant country characteristics, such as the level of development, the composition of output, and country size. The message: the dependence on tourism is a key explanatory variable of the growth shock in 2020. For instance, the analysis suggests that going from the share of tourism in GDP of Canada (around 6 percent) to the one of Mexico (around 16 percent) would reduce growth in 2020 by around 2.5 percentage points. If we instead go from the tourism share of Canada to the one of Jamaica (where the share of tourism in GDP approaches one third), growth would be lower by over 6 percentage points.

Measures of the severity of the pandemic, the intensity of lockdowns, the level of development, and the sectoral composition of GDP (value added accounted for by manufacturing and agriculture) also matter, but quantitatively less so than tourism. And results are not driven by very small economies; tourism is still a key explanatory variable of the 2020 growth shock even if we restrict our sample to large economies. Among tourism-dependent economies, we also find evidence that those relying more heavily on international tourism experienced a more severe hit to economic activity when compared to those relying more on domestic tourism.

Given data availability at the time of writing, the evidence we provided is limited to 2020. The outlook for international tourism in 2021, if anything, is worse, though with increasing vaccine coverage the tide could turn next year. The crisis poses particularly daunting challenges to smaller tourist destinations, given limited possibilities for diversification. In many cases, particularly among emerging and developing economies, these challenges are compounded by high starting levels of domestic and external indebtedness, which can limit the space for an aggressive fiscal response. Helping these countries cope with the challenges posed by the pandemic and restoring viable public and external finances will require support from the international community.

Related Content

Author

-

Acknowledgements and disclosures

The author thanks Manuel Alcala Kovalski and Jimena Ruiz Castro for their excellent research assistance.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).