Health Care Policy

High air ambulance charges concentrated in private equity-owned carriers

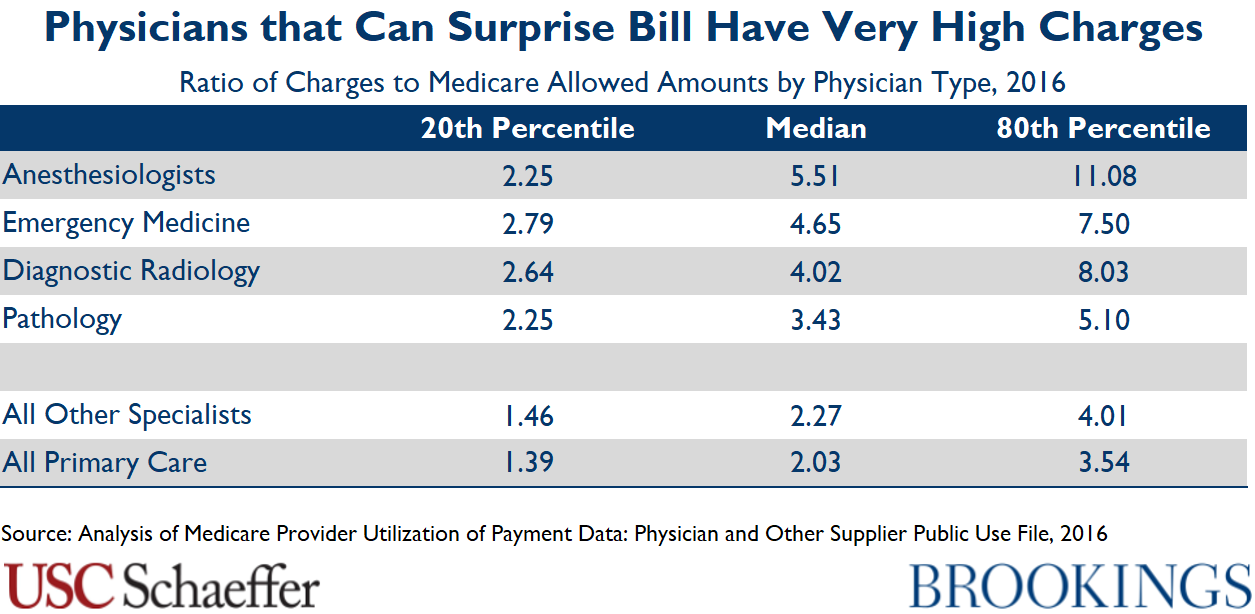

Surprise out-of-network bills arise when a consumer receives care from an out-of-network provider in a situation she cannot reasonably control, such as being treated by an out-of-network anesthesiologist at an in-network hospital. These bills are common for emergency and ancillary care — studies suggest that about 20 percent of emergency department visits and 10 percent of elective inpatient care stays involve at least one out-of-network provider.

Surprise billing reflects a market failure: patients do not choose their emergency and ancillary physicians, so the flow of patients these physicians receive depends on the hospital in which they practice, not the prices they charge or whether they join insurer networks. As a result, they have an out-of-network billing opportunity not available in other specialties, and many leverage that option not only to send large surprise bills, but also to demand very high in-network payment rates when they do enter insurers’ networks.

Federal and state policymakers are considering steps to end surprise billing, but leading proposals often do not go far enough to reduce excess spending. In fact, some proposals intended to address surprise billing could actually end up increasing spending on the services most vulnerable to surprise bills. On the other hand, well-crafted proposals can both protect patients from surprise bills and bring down premiums.

2019

2016