My recent piece, “Student loan forgiveness is regressive whether measured by income, education or wealth: Why only targeted debt relief policies can reduce injustices in student loans,” prompted several questions. Here are my answers to some of them.

You say that to consider student loans without considering the value of the education, the human capital, is like measuring a home-owning family’s wealth by counting only its mortgage and not the value of its house. But a homeowner can sell a house for cash quickly. One can’t sell one’s college education for cash similarly or pledge it for a loan. Is the comparison meaningful?

The objective of measuring wealth is to compare the relative economic wellbeing of different households. Who is better off and who is worse off? True, one way having assets can make you better off is that you get to spend it—pulling cash out of your bank account, or selling stocks or your home.

But the reason people own houses isn’t only that they can sell them in the future; it’s because they get to live in them—and derive a daily stream of value from having a safe place to sleep and enjoy life. Likewise, the reason stocks and bonds have value is that they provide the owner with a stream of income in the form of dividends or interest payments.

The same is true of educational investments. People invest in a college, graduate, or professional degree because it helps them earn more, avoid unemployment, and enjoy a higher quality of life. For young Americans aged 25-34, the increase in pay a college graduate earns compared to someone without a degree is at an all-time high (as I discuss more below).

Indeed, the value of postsecondary degrees in the labor market is a key reason why Americans line up at good-quality colleges. Harvard collects roughly $1.9 billion each year in tuition, mostly from high-income families. Those parents could have passed along that money to their kids, but instead, they bought something many times more valuable.

While you can’t sell your degree, that doesn’t make it worthless. Social Security recipients can’t sell their benefits, nor can beneficiaries of defined-benefit pension plans. But a worker with a $20,000 annual pension or Social Security payment is vastly better off than the apparently “wealthier” worker with $20,000 in a 401k.

So when it comes to assessing who benefits from student debt cancelation, the right concept of wealth to use is the lifetime economic resources of the borrower—not just what assets they can to sell but how much income the assets produce over time. And well-educated borrowers earn a lot of income from their degrees.

Your calculations rely on the typical or the average borrower, but doesn’t it matter what the degree is in? Some degrees have much higher pay off in the job market than others. And, is the return on college education in the form of higher wages so certain?

There is a lot of variation in the outcomes of students and student loan borrowers based on where they went to school, their family background, the programs they studied, the jobs they pursue after college, whether they can find work at all, and other factors.

I took that into account in my analysis by grouping individuals based not only by race and educational attainment, but also by income: some college students (or high school graduates or professional degree recipients) have lower-than-average-income careers, and some higher. As a result, some individuals are assumed to have gotten very little from their college careers (other than debt), but others gained a lot. (Indeed, the highest income high school graduates earn more than some of the lowest-earning better-educated groups.) But, on average, most individuals with a college or graduate degree earn much more than individuals without a college degree. College graduates are high in the income and wealth distribution, and so are student loan borrowers.

Is the fundamental problem that college simply costs too much, and we should bring it down so students don’t have to borrow so much?

Making college more affordable would help. But an important part of the increase in debt isn’t just the cost of college, but the fact that many more lower income students and nontraditional students are attending college without the same resources as “traditional” students. Moreover, this increase in attendance disproportionately occurred at lower-quality colleges that don’t provide the same increase in earnings. That means that more students would have borrowed, even absent the increase in tuition, and more would have struggled with repayment even if their balances were lower. And the same is true at graduate programs. Addressing the fundamental problem requires a combination of making college and graduate school cost less, increasing aid for lower-income students, and improving the quality of undergraduate and graduate programs to make sure students and taxpayers get their money’s worth.

Can’t we as a nation afford free college, just as K-12 education is free because of its benefits to society?

I prefer to frame this question as “What do we as a nation want to pay for?” rather than “What can we afford?” Even the most progressive policymakers define “free college” as undergraduate tuition and fees at public universities. Because this definition excludes graduate and professional degrees, tuition and fees at nonprofit and for-profit schools, and expenses for room and board and other living expenses, it does not cover the vast majority of the costs of postsecondary education and more than half of all student debt. One reason for the limited scope is that most of the benefits of postsecondary education aren’t public benefits to society at large, but private benefits to the student in the form of higher income and quality of life.

You are very focused on the well-off who will benefit from loan forgiveness—the doctors and lawyers. But if across-the-board loan forgiveness is the cleanest and most politically possible way to relieve the stress on low- and middle-income borrowers struggling under the weight of their student loans, can you see the merit of this argument?

Yes, I’m very focused on well-off Americans disproportionately benefiting from federal policies. Inequality in income and wealth has surged over time (especially across educational lines). Federal tax and spending policies have contributed to this inequity, for example, by cutting taxes on high-income groups. When it comes to student loans, the budget and distributional implications are enormous. Widespread student loan forgiveness would rank among the largest transfer programs in American history. Forgiving all student debt would be a transfer larger than the amounts the nation has spent over the past 20 years on unemployment insurance, the Earned Income Tax Credit, or food stamps. And in contrast to those programs, which serve deeply poor families, beneficiaries of student debt forgiveness would be higher income, better educated, and whiter than beneficiaries of just about all other programs designed to reduce economic hardship and promote economic opportunity.

For all other significant spending programs, we enhance their efficacy by targeting the aid to those who need it. There is no doubt the Department of Education could do the same for student loan forgiveness. They know your family income and assets from your aid application, they know whether you borrowed to get an undergraduate degree or for an Ivy League law school, they know whether you struggled with your loan since leaving school, and they know (or could know) how much you earn in the labor market after graduation. It doesn’t need to be any harder to target debt relief to those in need than it is to implement widespread forgiveness.

Is it true that the really rich don’t have student loans because they didn’t need to borrow to pay their tuition? Or that financial aid is only for low-income students, so that only low-income students have student loans?

There is no income or asset test for federal student loans—any student is eligible. In fact, loans can only be used for tuition, fees, and living expenses that are not covered by grant aid, which means that higher-income students attending more expensive schools get to borrow more. And graduate students can borrow the full cost of attendance.

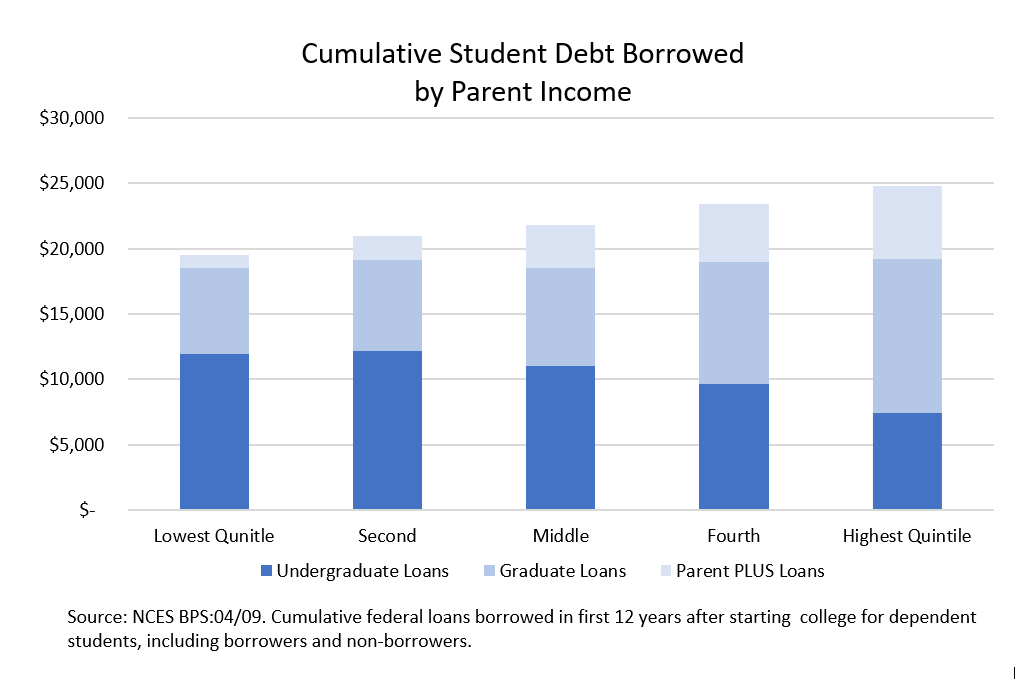

The result of universal loan eligibility and the fact that students from high-income families are more likely to go to college or graduate school means that students from high-income families borrow more in student loans than other groups.

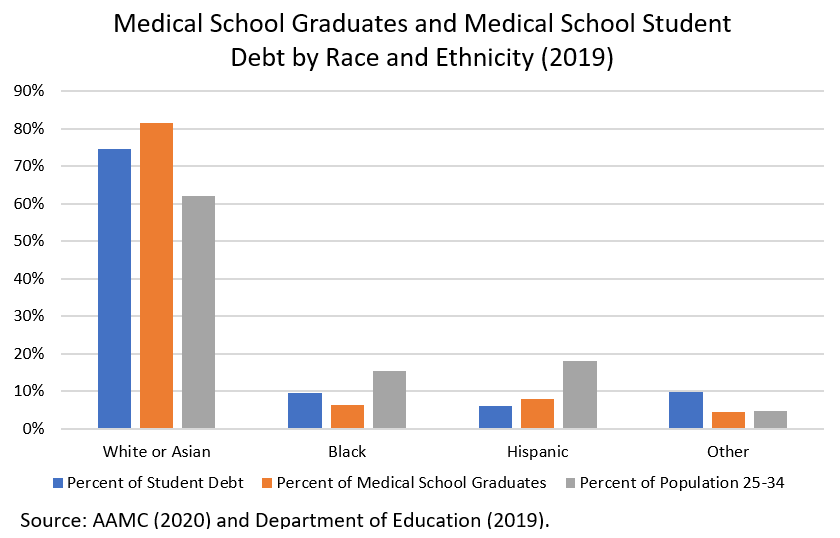

According to the Association of American Medical Colleges (AAMC), 91 percent of Black medical school students graduate with student debt, and those borrowers owe a median amount of $230,000. In contrast, 71 percent of white graduates borrow and owe $200,000. Doesn’t that mean that forgiving student debt is progressive and closes racial wealth gaps?

No, forgiving student debt of doctors is regressive and increases racial wealth gaps. According to the AAMC, white or Asian medical school graduates owe 8 times the total amount of student debt as do Black medical graduates because white and Asian Americans are more than three times as likely as Black Americans to go to medical school. While Black medical students owe more than their white peers, the major source of inequity in medical school debt (like student debt more generally) is who gets to enroll in the first place; according to the Digest of Education Statistics, while 82 percent of new doctors in 2018 were white or Asian, only 6 percent were Black, and 8 percent Hispanic.

While doctors owe huge amounts of student debt (a median of around $200,000 each), that doesn’t mean they need a taxpayer-financed bailout. Doctors are the highest paid profession in the U.S. and in every single U.S. state. More than a quarter of all doctors are in the top 1 percent of the income distribution, and more than 50 percent of doctors are in the top 2 percent. In 2017, the average income of physicians was $343,000; even in the lowest paid specialty (primary care), physicians earn $243,400. Over the course of their careers, the average physician will earn $9.6 million.

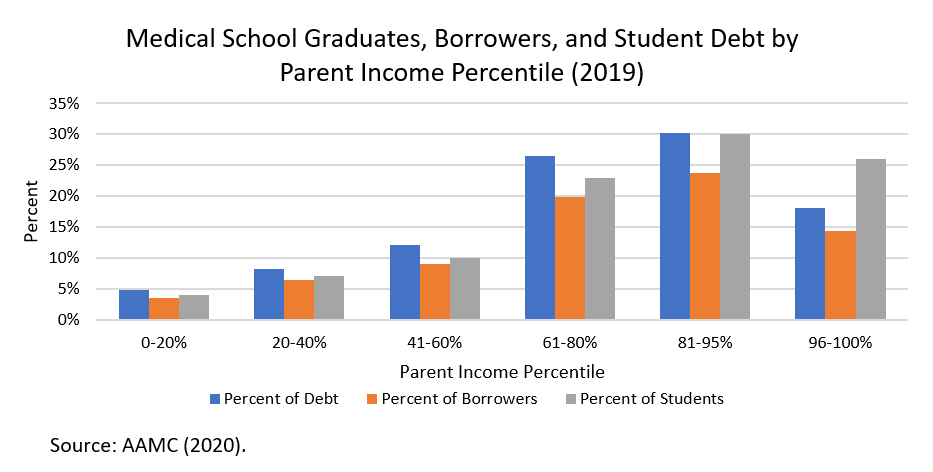

Not only are doctors high income after medical school, but they mostly grew up in higher-income households. As the figure below illustrates, 26 percent of all medical school graduates were born to parents in the top 5 percent of the income distribution and 30 percent were born into parents in the 81st to 95th percentiles. The fact that there are so many rich kids in medical school means that students in the top 5 percent of the income distribution represent 14 percent of all borrowers and 18 percent of all medical school student debt. Doctors who grew up in the top 5 percent of the income distribution and who are virtually assured to remain in the top 5 percent as adults owe 40 percent more student debt than all medical school students who grew up in the bottom 40 percent of the population. Surely there are Americans in deeper financial need and who are more deserving of support from taxpayers.

Today’s students aren’t getting the same return on their college as previous generations, so isn’t it wrong to assume that they’ll have the same boost to lifetime earnings as older Americans did?

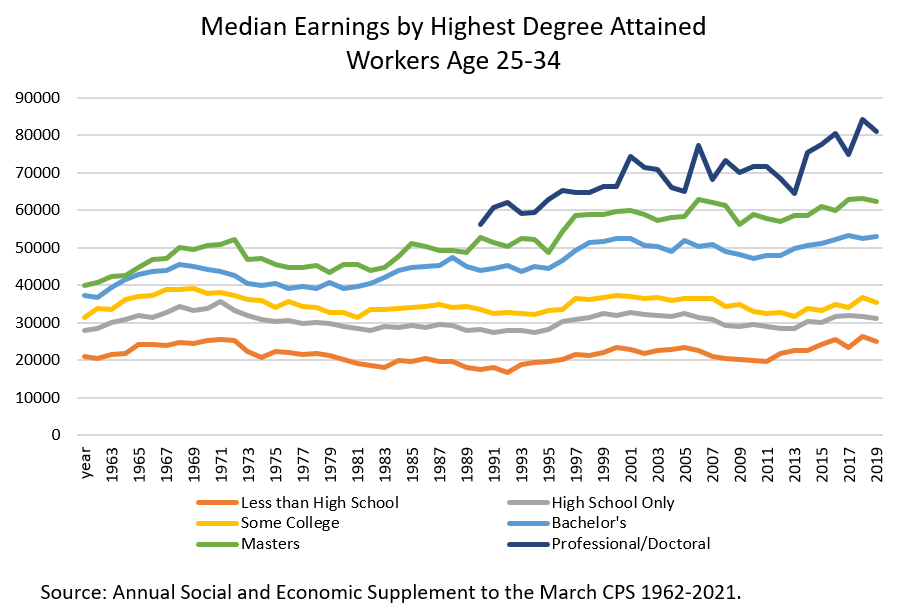

The economic benefit to a college degree has, in fact, never been larger. The figure below shows the median annual earnings of Americans aged 25 to 34 by the highest degree attained from 1961 to 2020 (adjusted for inflation). The annual earnings of well-educated Americans—those with a doctoral or professional degree, a master’s degree, or a bachelor’s degree—have never been higher. Likewise, the earnings gap between college-educated individuals and those with only a high school diploma has never been larger.

And the prospects for future gains for better-educated young Americans remain strong. The following chart shows the median annual earnings by age for individuals with and without a college degree in the 1990s compared to the 2010s (roughly before and after the increase in student debt). There has been almost no increase in the typical earnings of Americans without a college degree over this time period (at every age, Americans with “No Degree” earn about the same today as they did in the 1990s). But the typical earnings of college-educated Americans have increased substantially at every age, relative to both the 1990s and 2000s. And the typical earnings of better-educated individuals grows quickly each year after they leave school. Looking at the data on the economic outcomes of Americans, the group that needs the help aren’t the nation’s doctors, lawyers, graduate-degree holders, and better-off college graduates—it’s those who haven’t completed a degree or never had the chance to go to college in the first place.

The Brookings Institution is financed through the support of a diverse array of foundations, corporations, governments, individuals, as well as an endowment. A list of donors can be found in our annual reports published online here. The findings, interpretations, and conclusions in this report are solely those of its author(s) and are not influenced by any donation.

Related Content

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Responses to reader questions about my report “Student loan forgiveness is regressive”

January 31, 2022