This explainer was originally published in April 2018 by David Wessel and Michael Ng. It was updated in April 2022 to reflect changes to the yield curve.

Financial markets sometimes offer clues to the future direction of the economy because they reflect the views of so many investors who are putting money behind their forecasts. One gauge that often gets attention is the yield curve. You can hear Federal Reserve officials talking about it. You can see it in headlines in the financial press: “Why is the yield curve flattening and what does it mean,” “Economists Seek Recession Clues in the Yield Curve,” and “Inversion Confusion”.

Here’s a primer on what the yield curve tells us – and what it doesn’t.

What is the yield curve?

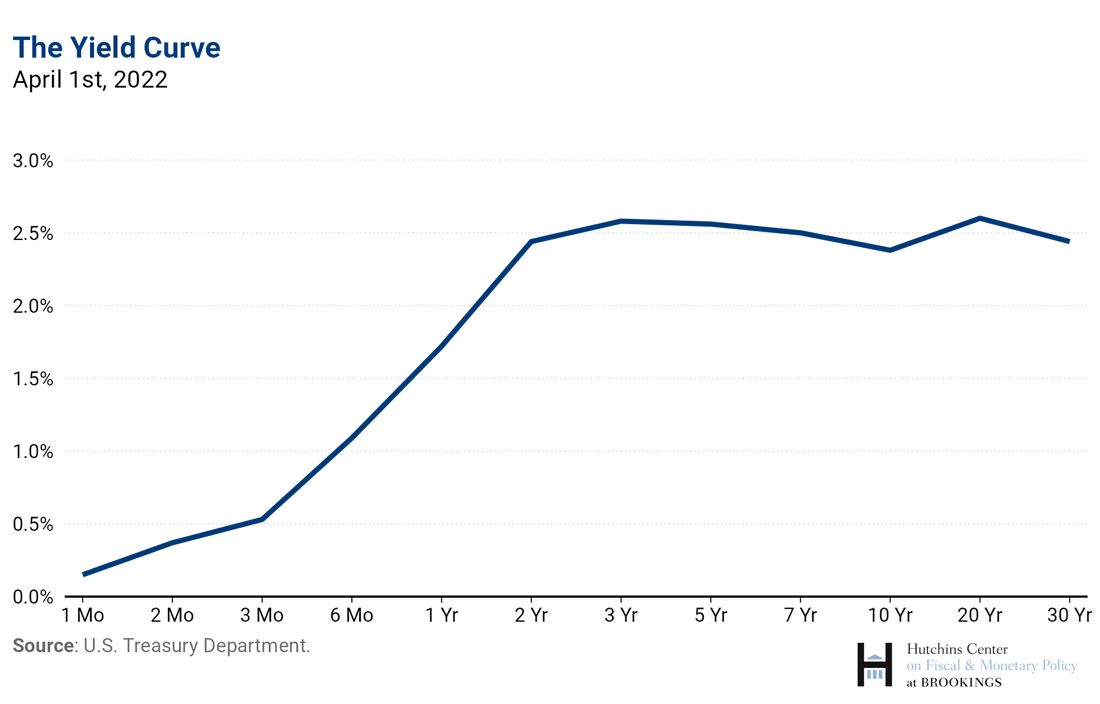

The yield curve is a visual representation of how much it costs to borrow money for different periods of time; it shows interest rates on U.S. Treasury debt at different maturities at a given point in time.

As the chart below shows, the yield on 30-day Treasury bills was 0.15% on April 1st, 2022, and the yield on 30-year Treasury bonds was 2.44%.

Why does the yield curve USUALLY slope upwards?

Lenders and bond investors who commit to tying up their money for longer periods of time take on more risk because it’s harder to forecast economic conditions – inflation, Federal Reserve policy, the global economy – over a decade than over the next week or month; as conditions change, so too will yields, so there’s a lot more uncertainty about potential gains and losses on longer-term investments than on short-term. The extra compensation that lenders and investors demand for making long-term loans is known as the term premium. With a positive term premium, the yield curve usually slopes upwards.

What else determines the slope of the yield curve?

Expectations for Fed policy

The Federal Reserve influences short-term interest rates across the economy by targeting the federal funds rate, the interest rate at which banks lend to each other overnight and a benchmark for other interest rates in the economy. The yield curve reflects market expectations about future Fed interest-rate moves. Increases in the Fed’s target for short-term rates usually – but not always – lead to an increase in longer-term rates. The average response to a December 2017 survey of 23 broker-dealers estimated that Fed rate increases explain about two-thirds of the decline in the yield curve’s slope between December 2015 and December 2017.

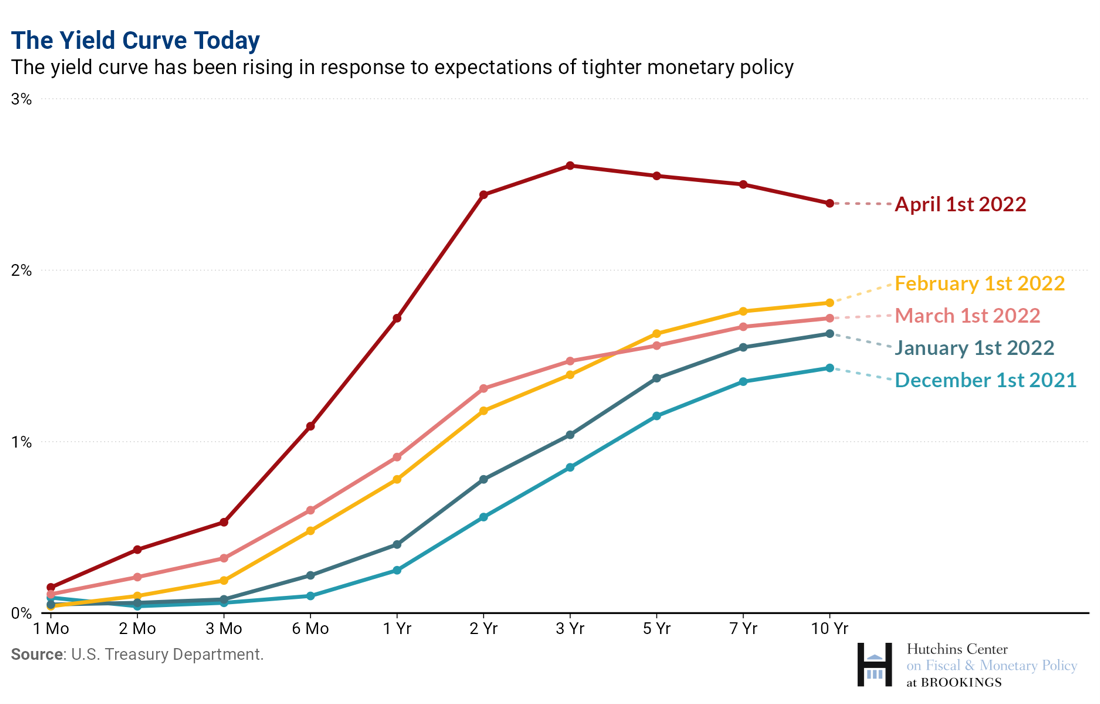

The Fed’s move in March 2022 to raise short-term interest rates from zero and its stated intention to keep raising them led to flatter yield curve, as the chart below shows. The reasons for this are not completely clear. It could reflect market expectations that the Fed will raise interest rates so much that it’ll cause a recession or a period of painfully slow growth in order to win the battle against inflation. And once the economy weakens enough to reduce price pressures, the Fed will back off to protect growth and employment.

Expectations for inflation

Inflation erodes the value of any promise to pay a fixed sum in the future, including interest payments on a bond or loan. Investors and lenders demand compensation for this by building an “inflation premium” into the interest rate on a loan or bond.

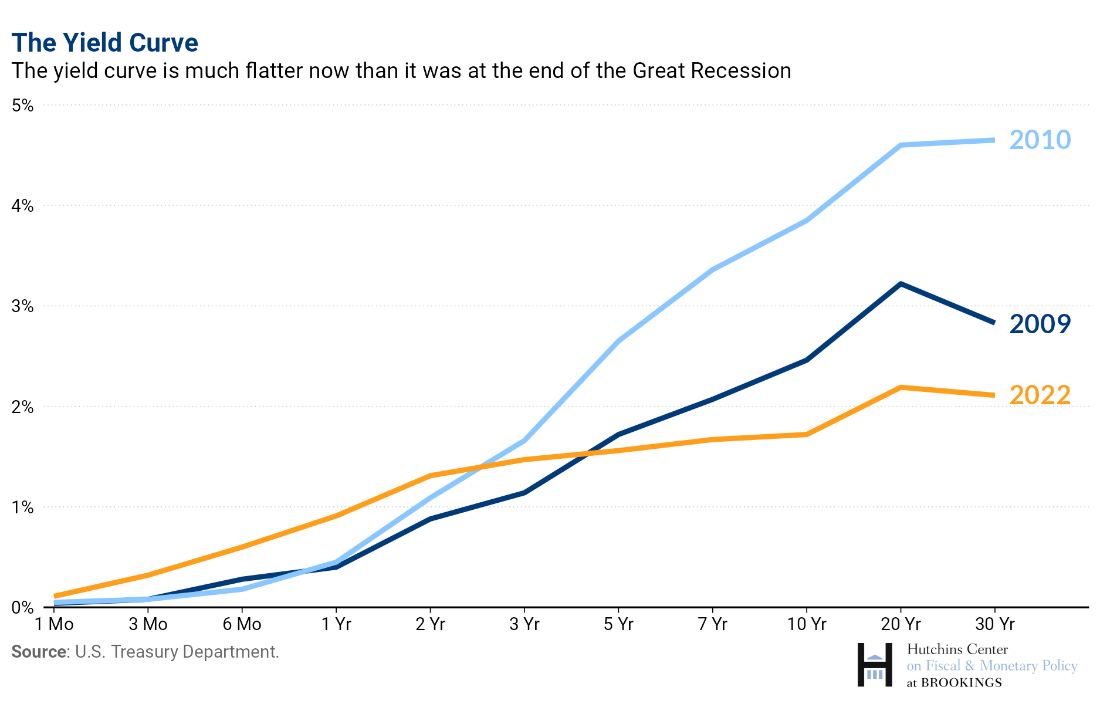

The term premium and expectations for Fed policy change over time. As they change, so does the difference between short- and long-term rates. This is illustrated in the chart below, which draws the yield curve at different points in time. Notice how the yield curve steepened going from 2009 to 2010 as investors built in their expectations of Fed tightening as the economy recovered from the Global Financial Crisis; it has flattened significantly since the end of the Great Recession in 2009 as the persistence of the extremely low rates of the 2010s changed expectations about where monetary policy would need to go in 2022 and beyond.

In early 2022, the yield curve shifted up as the Fed began to lift interest rates from zero and said it planned to keep raising them to thwart an unwelcome surge of inflation.

The term premium

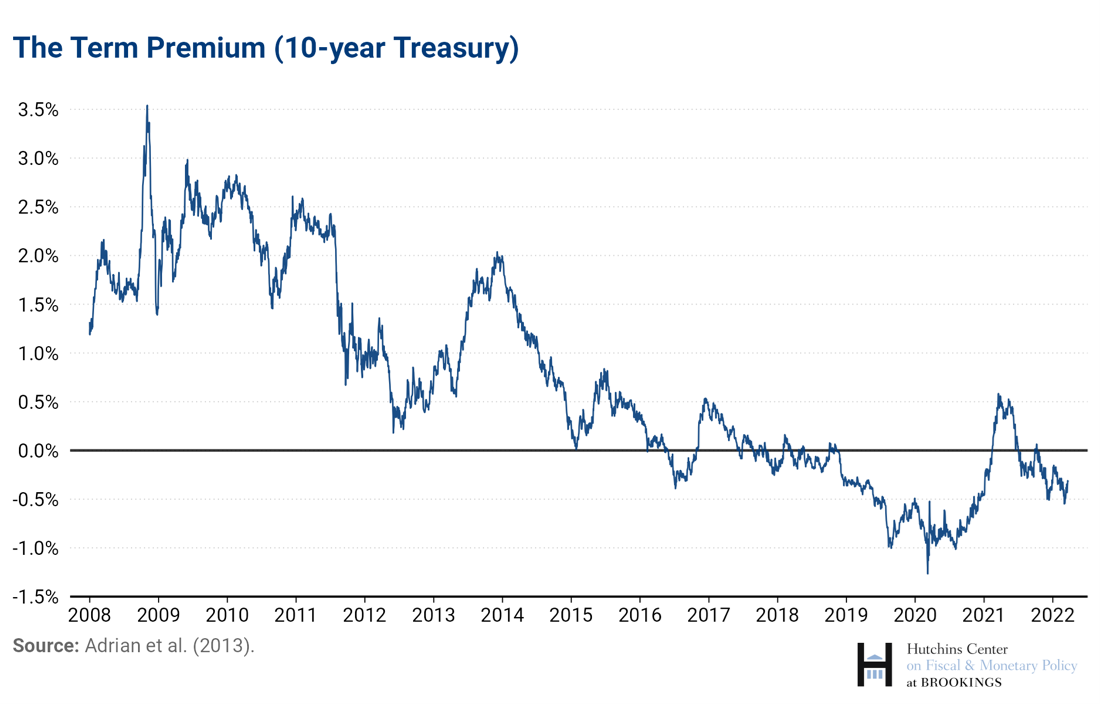

The term premium – that extra yield that investors demand for holding longer-term debt – has been quite low by historical standards in recent years. Estimates by the New York Fed show that the term premium on 10-year Treasury bonds has declined since the end of the Great Recession, as shown in the chart below.

When the term premium is small, investors are settling for a very low return for holding a longer-term bond. In some instances, the term premium can even be negative; that is, investors aren’t even getting fully compensated for expected inflation and the expected path of future Fed rate increases. When the Federal Reserve buys bonds in what’s known as quantitative easing, as it did during the Global Financial Crisis of 2007-9 and the COVID-19 pandemic, that tends to depress the term premium.

See Former Fed Chair Ben Bernanke’s discussion of term premiums in this 2015 blog post.

What is an inverted yield curve?

An inverted yield curve means the interest rate on long-term bonds is lower than the interest rate on short-term bonds. This is often seen as a bad sign for the economy. That’s because long-term rates might go down – inverting the yield curve – if markets expect that the economy will deteriorate and that the Fed will cut short-term rates in the future. (Recall that one factor that determines the yield curve is market expectations for future Fed policy.) Alternatively, markets could be anticipating very low inflation or even deflation in the years ahead, also negative for the economy. But those aren’t the only possibilities: An inverted yield curve could reflect a shrinking of the term premium.

One measure commonly cited by Wall Street analysts compares the yield on two-year and 10-year treasuries. On Friday, April 1, the yield on the two-year was slightly higher (2.44%) than the yield on the 10-year (2.38%).

Does an inverted yield curve mean there will be a recession soon?

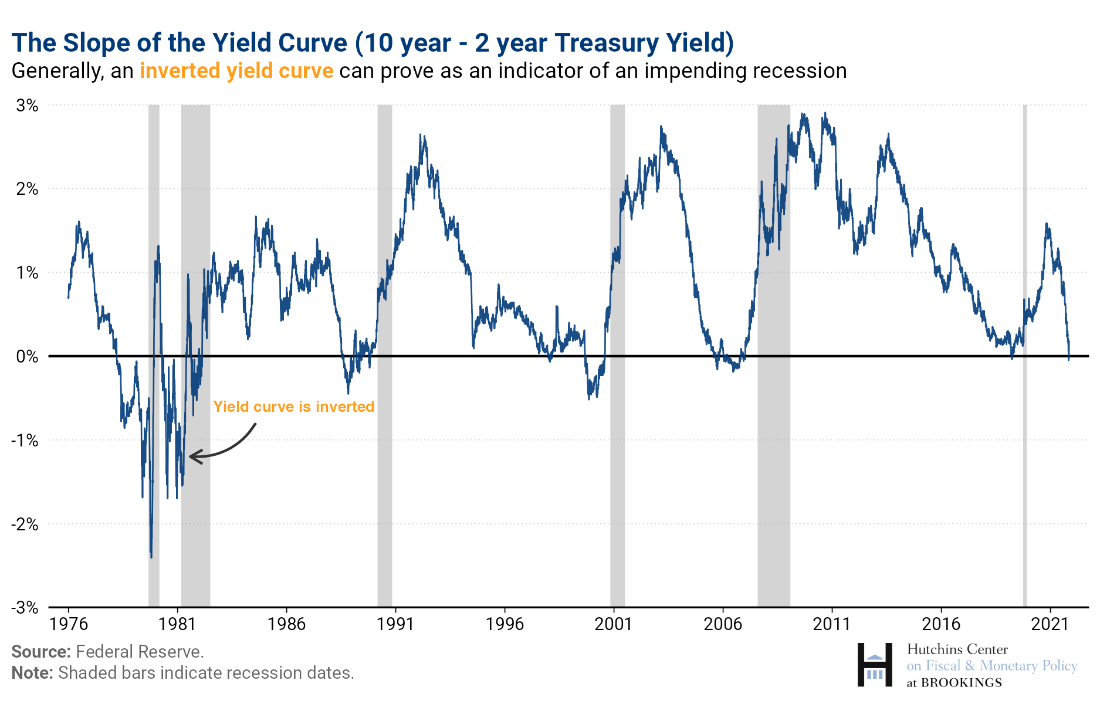

Often. The chart below shows the slope of the yield curve since 1976, measured as the rate on 10-year Treasury debt minus the rate on 2-year Treasury debt. When the line dips below zero, interest rates on longer-term bonds are lower than shorter-term bonds, i.e. an ‘inverted’ yield curve. Notice that every time over this period that the yield curve has inverted, a recession has followed.

The December 2017 Federal Open Market Committee (FOMC) minutes indicate that some committee members expressed concern that the flattening of the yield curve “could portend an economic slowdown, noting that inversions have preceded recessions over the past several decades, or that a protracted yield curve could adversely affect the financial conditions of banks….” (Banks, in general, profit more when long-term rates at which they lend are higher than short-term rates at which they borrow or pay on deposits.)

This time could be different, though, as other FOMC members argued at that same meeting, because term premiums are unusually low. Research by Fed economists argues that an inverted yield curve does increase the probability of a recession occurring relative to any given point in time, but controlling for the low levels of interest rates overall this probability is lower. The New York Fed estimates that as of March 2021 the probability of a recession in the next year based on the slope of the yield curve was only around 6%, compared to 40% right before the 2008 recession. Much of this relies on the case that with a very low term premium, the yield curve will naturally be flatter, and that relatively small increases in short-term interest rates relative to long-term rates could lead to inversion. Former Fed Chair and current Treasury Secretary Janet Yellen explained in December 2017:

“[T]there is a strong correlation historically between yield curve inversions and recessions, but let me emphasize that correlation is not causation, and I think that there are good reasons to think that the relationship between the slope of the yield curve and the business cycle may have changed. And one reason for that is that long-term interest rates generally embody two factors. One is the expected average value of short rates over, say, 10 years, and the second piece of it is a so-called term premium that often reflects things like inflation—inflation risk…[R]ight now the term premium is estimated to be quite low, close to zero, and that means that the yield curve is likely to be flatter than it’s been in the past. And so it could more easily invert. If the Fed were to even move to a slightly restrictive policy stance, you could see an inversion with a zero term premium. So I think the fact the term premium is so low and the yield curve is generally flatter is an important factor to consider.”

Although investors often compare the yields on two- and ten-year Treasuries, Fed economists Eric Engstrom and Steven Sharpe question the usefulness of that approach. Instead, they prefer looking at yields on Treasury debt with maturities of less than two years. Fed Chair Jerome Powell referred to this in March 2022 when he spoke to the National Association for Business Economics:

“Frankly, there’s good research by staff in the Federal Reserve system that really says to look at the short — the first 18 months — of the yield curve. That’s really what has 100% of the explanatory power of the yield curve. It makes sense. Because if it’s inverted, that means the Fed’s going to cut, which means the economy is weak.”

The Brookings Institution is financed through the support of a diverse array of foundations, corporations, governments, individuals, as well as an endowment. A list of donors can be found in our annual reports published online here. The findings, interpretations, and conclusions in this report are solely those of its author(s) and are not influenced by any donation.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

The Hutchins Center Explains: The yield curve – what it is, and why it matters

December 5, 2018