Studies in this week’s Hutchins Roundup find that the removal of a personal bankruptcy flag from credit reports improves access to credit but has no effect on labor market outcomes, the Fed’s emergency lending during the financial crisis decreased short-term interest rates of some foreign banks, and more.

Bad credit reports have little effect on labor market outcomes

Credit reports are widely used in consumer lending decisions and increasingly in hiring decisions as well, but little is known about the consequences of a bad credit report. Will Dobbie of Princeton, Paul Goldsmith-Pinkham of the New York Fed, Neale Mahoney of the University of Chicago, and Jae Song of the Social Security Administration use the difference in the length of time a personal bankruptcy remains on the credit report under Chapter 13 versus Chapter 7 bankruptcies to estimate the causal effect of poor credit on outcomes. They find that the removal of a bankruptcy flag leads to large increases in credit scores and the magnitude of both credit card and mortgage borrowing, but has no effect on employment or earnings.

The Fed’s unconventional policies during the financial crisis spilled over across borders

During the global financial crisis, the Fed created so-called emergency liquidity facilities that provided last-resort lending to distressed U.S. banks and the U.S. subsidiaries of foreign banks. Thomas Kick and Michael Koetter of the Deutsche Bundesbank and Manuela Storz of the Frankfurt School of Finance and Management find a significant decline in the short-term deposit rates and funding costs of German banks with access to the U.S. liquidity facilities compared to German banks without access to these funding sources. Short-term loan rates charged to German corporations also declined but with a lag.

Flexible work arrangements are not always preferred by jobseekers

Alexandre Mas of Princeton and Amanda Pallais of Harvard use a field experiment to study how workers value alternative work arrangements. They conclude that most jobseekers are not willing to accept lower wages for either the ability to choose the days and time of work or the number of hours they work per week. However, the average worker is willing to take a 20% wage cut to avoid jobs that permit employers to schedule work outside of the traditional Monday to Friday 9 am to 5 pm hours. The authors also find that, although the great majority of workers do not value flexible scheduling, some workers—especially women with young children—do show a significant preference for working from home and having a regular schedule.

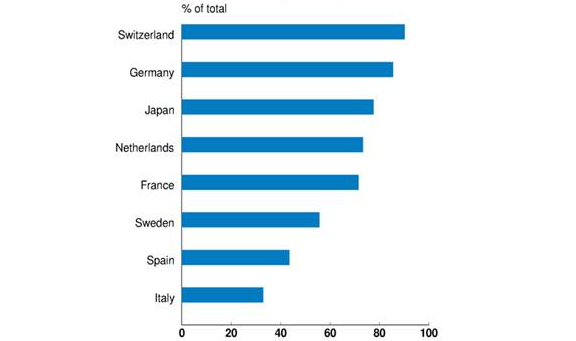

Chart of the week: A high share of government debt is trading at negative yields

Quote of the week: “Gone is the pre-crisis ideal of minimalist central banks with small balance sheets, narrowly defined objectives and tools, and a bias toward non-intervention,” says Bank of England official Minouche Shafik

“[First], broadening of our responsibilities and range of tools at our disposal has facilitated a more joined up approach to how we set monetary policy and pursue financial stability… Second, the increase in size of our balance sheet has been a necessity of the times we live in. Deep structural forces have combined to depress the level of interest rates at which the economy would be in equilibrium, obliging us to rely evermore on monetary policies that were once considered unconventional. This requires us to operate with multiple instruments in multiple markets meaning that our impact on the financial system – the central bank’s footprint – is larger. Third, we are aware that some of our policies have spillovers and side effects, but we take steps to address them where feasible to do so within our mandate. We know that a bigger footprint means we need to be mindful of our step. Finally, despite our bigger size, there are some things central banks cannot do. To generate sustainably strong growth over the medium term, monetary and financial stability policy must be part of a balanced package that also includes the government’s economic policies and, given strong global interconnections, international policy co-ordination.”

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Hutchins Roundup: Bankruptcy, emergency liquidity facilities, and more

Thursday, October 6, 2016