Studies in this week’s Hutchins Roundup find that fiscal consolidation via spending cuts is more effective, commodity price shocks increase the probability of banking crises, and more.

F

iscal consolidation via reduced spending

more likely to lower debt-to-GDP ratio than via higher taxes

Using a panel of 11 Euro area countries, Maria Grazia Attinasi of the European Central Bank and Luca Metelli, now at the Bank of Italy, find that the composition of fiscal consolidation – policies aimed at minimizing deficits – matters. Specifically, they find that a durable reduction in the debt-to-GDP ratio is more likely to be achieved if consolidation is implemented by reduced spending rather than by tax increases. Furthermore, delaying fiscal consolidation until a country confronts fiscal stress may result in a smaller reduction in the debt-to-GDP ratio for given consolidation effort.

Commodity price shocks undermine financial sector stability in developing economies

Using a sample of 71 commodity exporting emerging and developing countries, Tidiane Kinda, Montfort Mlachila and Rasmané Ouedraogo of the IMF find that negative commodity price shocks are associated with higher non-performing loans, higher bank costs and more banking crises. A fall of 50 percent in commodity prices, similar to the recent decline, results in an increase in non-performing loans of 3.6 percentage points, increasing the probability of banking crises.

Central bank communication has no effect on real economic variables

Applying computational linguistics to statements of the Federal Open Market Committee, Stephen Hansen of Pompeu Fabra University and Michael McMahon of University of Warwick find that in the last 18 years Fed communication on future interest rates has been much more important than the Fed’s assessment of current economic conditions. However, they also find that neither form of communication has particularly strong effects on real economic variables.

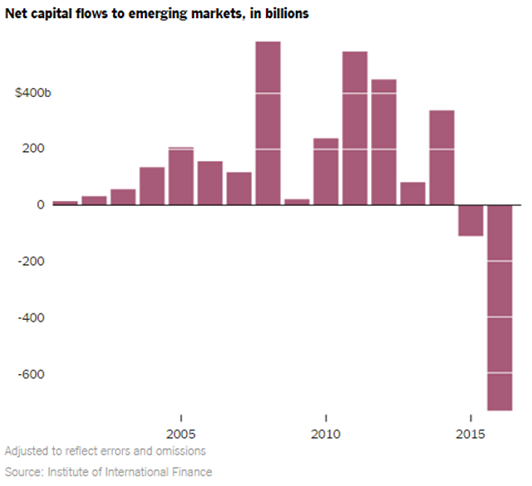

Chart of the week: Money is now flowing out of emerging markets

Quote of the week: “[I]n the aftermath of the Great Recession, there is some uncertainty about what the ‘normal’ level of interest rates is,” says Cleveland Fed President Loretta J. Mester

“We use the word ’normalization,’ but in the aftermath of the Great Recession, there is some uncertainty about what the ‘normal’ level of interest rates is. If productivity growth remains low and the potential growth rate of the economy over the longer run has moved lower, as many economists estimate it has, then the longer-run level of the fed funds rate consistent with price stability and maximum employment – the so-called neutral rate – would also be lower than it was in earlier periods. But estimates of long-run growth are imprecise and subject to revision, so this means there is considerable uncertainty around this neutral fed funds rate as well.”

— Loretta J. Mester, President, Federal Reserve Bank of Cleveland

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Hutchins Roundup: Fiscal consolidation, commodity price shocks, and more

February 11, 2016