Uncertainty about business prospects is a fact of life for any business. When deciding whether to recruit new workers or invest in a new technology, businesses do not know if this will result in greater sales and profits, because of factors outside their control. Instead, they forecast future sales revenue (and other performance metrics) and take account of the uncertainty around those forecasts. They think through situations where things may turn out worse than the forecast, leaving them with too many workers and idle investments—or the opposite when things turn out better. Only after weighing these scenarios can firms decide whether to hire those workers or invest in that technology.

When facing high uncertainty, firms usually also have the option to wait and see to avoid making mistakes. This option is most attractive when the business environment is highly unpredictable and the decision is costly to reverse, such as when it is costly to fire workers or to resell machinery and equipment. But it is also costly in itself: waiting means delaying or cancelling some projects that would have been profitable. In theory, such delays can have major economic consequences. They might lower a country’s productivity if many businesses end up operating at a suboptimal scale or with suboptimal technology. This issue is potentially more serious in developing and emerging economies, where inadequate business investment and technology adoption often drag down productivity and economic growth.

Measuring uncertainty

In practice, however, economists struggle to understand how uncertainty impacts businesses and the macroeconomy. Part of the reason is that standard measures of uncertainty like stock market volatility and forecaster disagreement do not capture uncertainty at the level of individual businesses; that is, the uncertainty businesses managers perceive around their forecasts of future sales and performance. Only recently have researchers made substantial progress in directly measuring this subjective uncertainty at the firm-level. The state-of-the-art methodology uses surveys of business managers that elicit a series of scenarios about future own-firm outcomes and a probability for each scenario. This combination of scenarios and probabilities allows researchers to construct measures of business forecasts and business uncertainty as perceived by each individual manager.

So far, most efforts to measure subjective business forecasts and uncertainty have been limited to a handful of high-income countries like the U.S. and U.K. But new data collected by the World Bank shows that a simplified version of this state-of-the-art methodology also works well in developing and emerging economies. This is an important development because many researchers have believed that it would be difficult to conduct this sort of survey in developing countries, where businesses and their managers can be less sophisticated. The new World Bank data refute those concerns and reveal systematic differences in the way business managers perceive uncertainty across countries that have different income levels.

The data in question come from the World Bank’s Business Pulse and Enterprise Surveys, which were created to track the impact of the coronavirus pandemic on the private sector. Both surveys include a module that elicits a central, optimistic, and pessimistic scenario for future own-firm sales alongside probabilities for each scenario. Over 23,000 businesses across 41 countries in Eastern Europe, Asia, Africa, and Latin America participated between April 2020 and March 2022. The countries covered span a wide range of income levels, from Madagascar at the low end to Poland at the high end.

Stylized facts

As it turns out, measures of business sales forecasts and uncertainty constructed from these World Bank data capture a lot of information about the business outlook that managers are privy to, as the following stylized facts show.

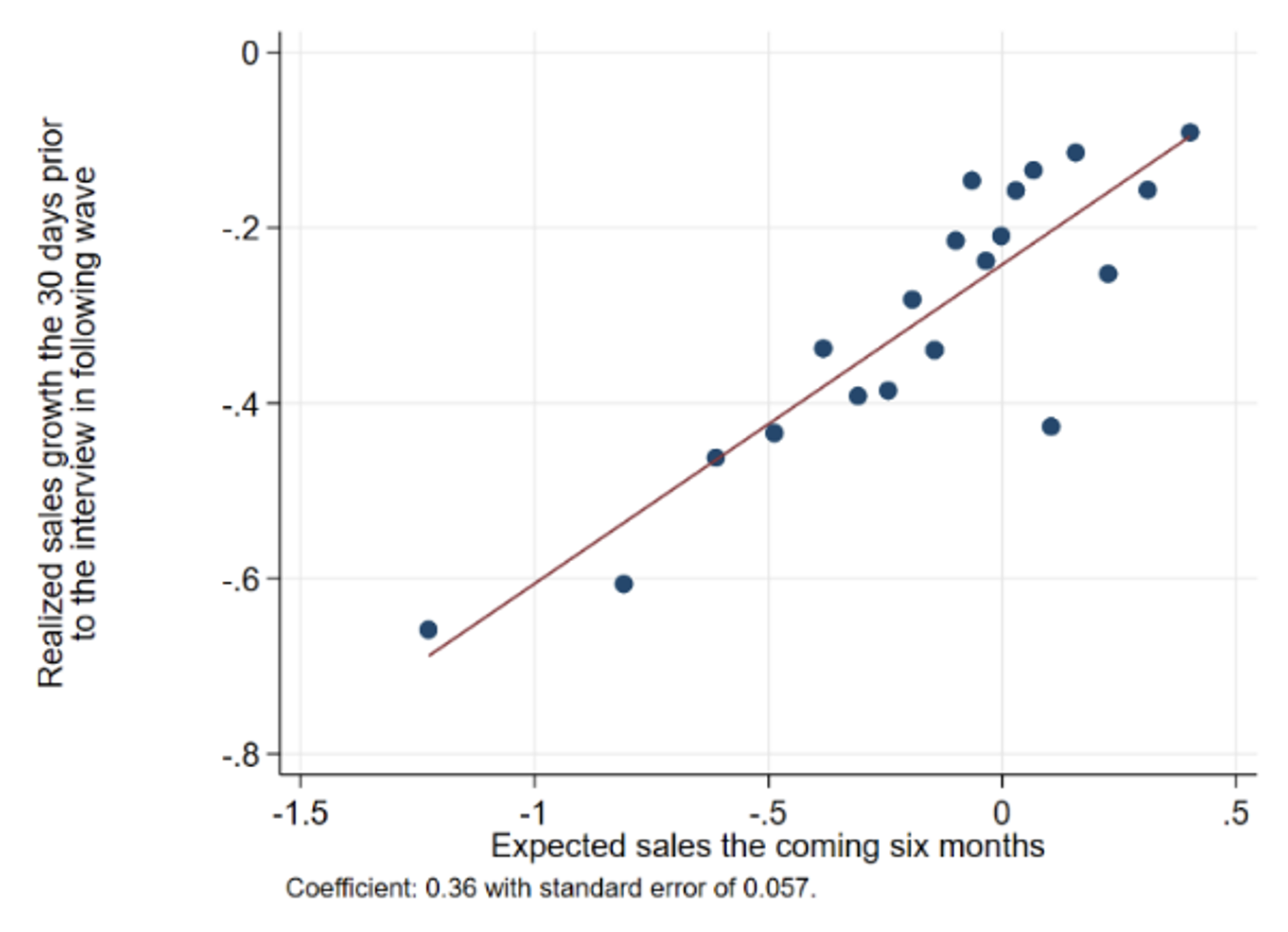

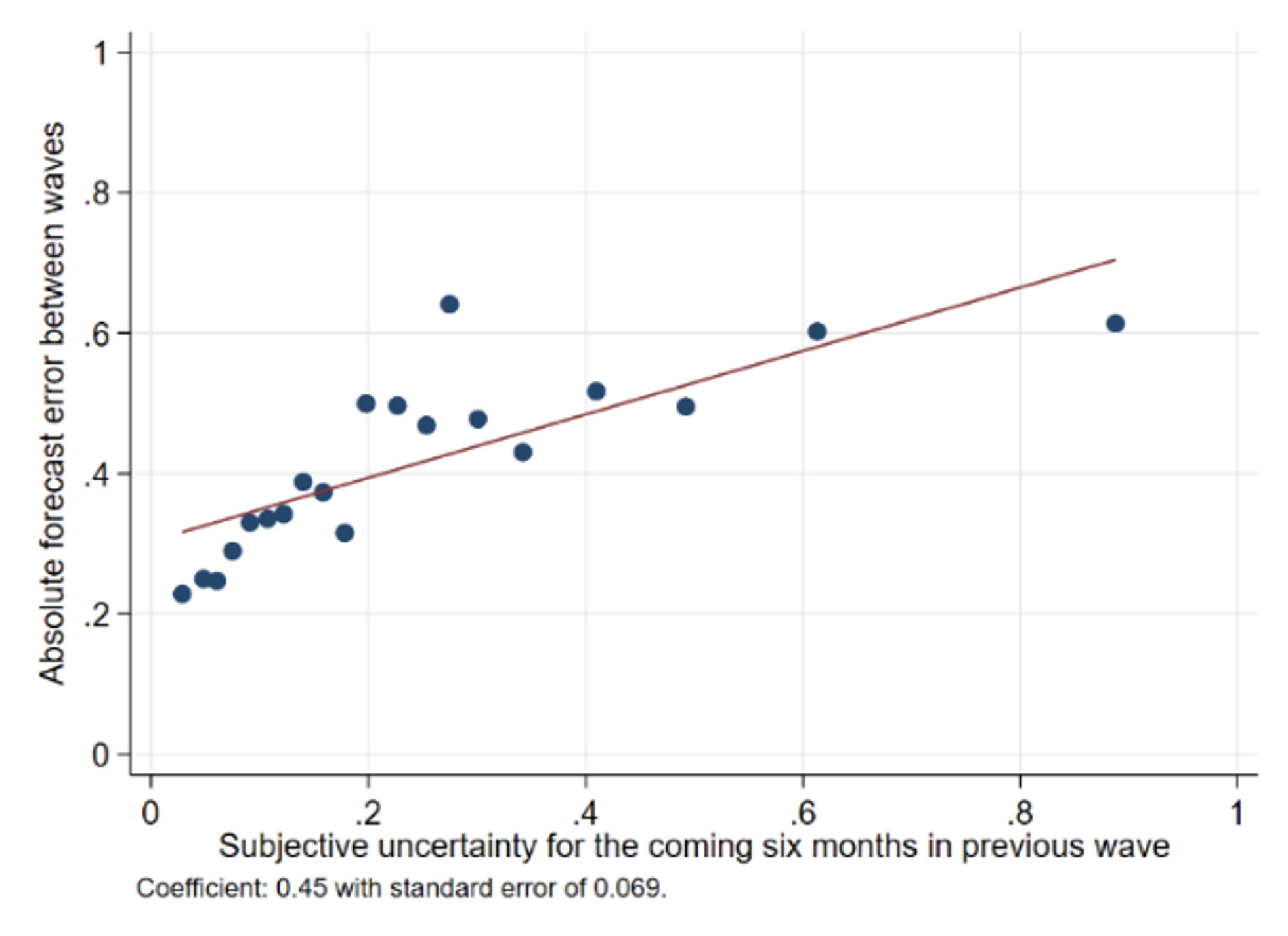

First, forecasts for future sales predict actual future sales as reported in follow-up survey interviews (Figure 1). Second, managers who express higher uncertainty at the time of the forecast tend to make larger forecasting mistakes (Figure 2). This second fact says that the survey-based measure of business uncertainty captures the degree of unpredictability or volatility of firms’ sales, and mirrors similar results from survey efforts in advanced economies.

Figure 1. Sales forecasts predict actual sales

Notes: Binned scatter plot of realized sales in the follow-up interview against sales expectations (forecast) for the next six months on the horizontal axis. Realized and expected sales are both expressed relative to 2019 levels.

Notes: Binned scatter plot of realized sales in the follow-up interview against sales expectations (forecast) for the next six months on the horizontal axis. Realized and expected sales are both expressed relative to 2019 levels.

Figure 2. Firms reporting higher uncertainty make bigger forecasting errors Notes: Binned scatter plot of the absolute error between sales expectations (i.e., forecasts looking six months ahead) and realized sales in the follow-up interview, against subjective uncertainty about six-months-ahead sales. Realized and expected sales are both expressed relative to 2019 levels.

Notes: Binned scatter plot of the absolute error between sales expectations (i.e., forecasts looking six months ahead) and realized sales in the follow-up interview, against subjective uncertainty about six-months-ahead sales. Realized and expected sales are both expressed relative to 2019 levels.

Related Books

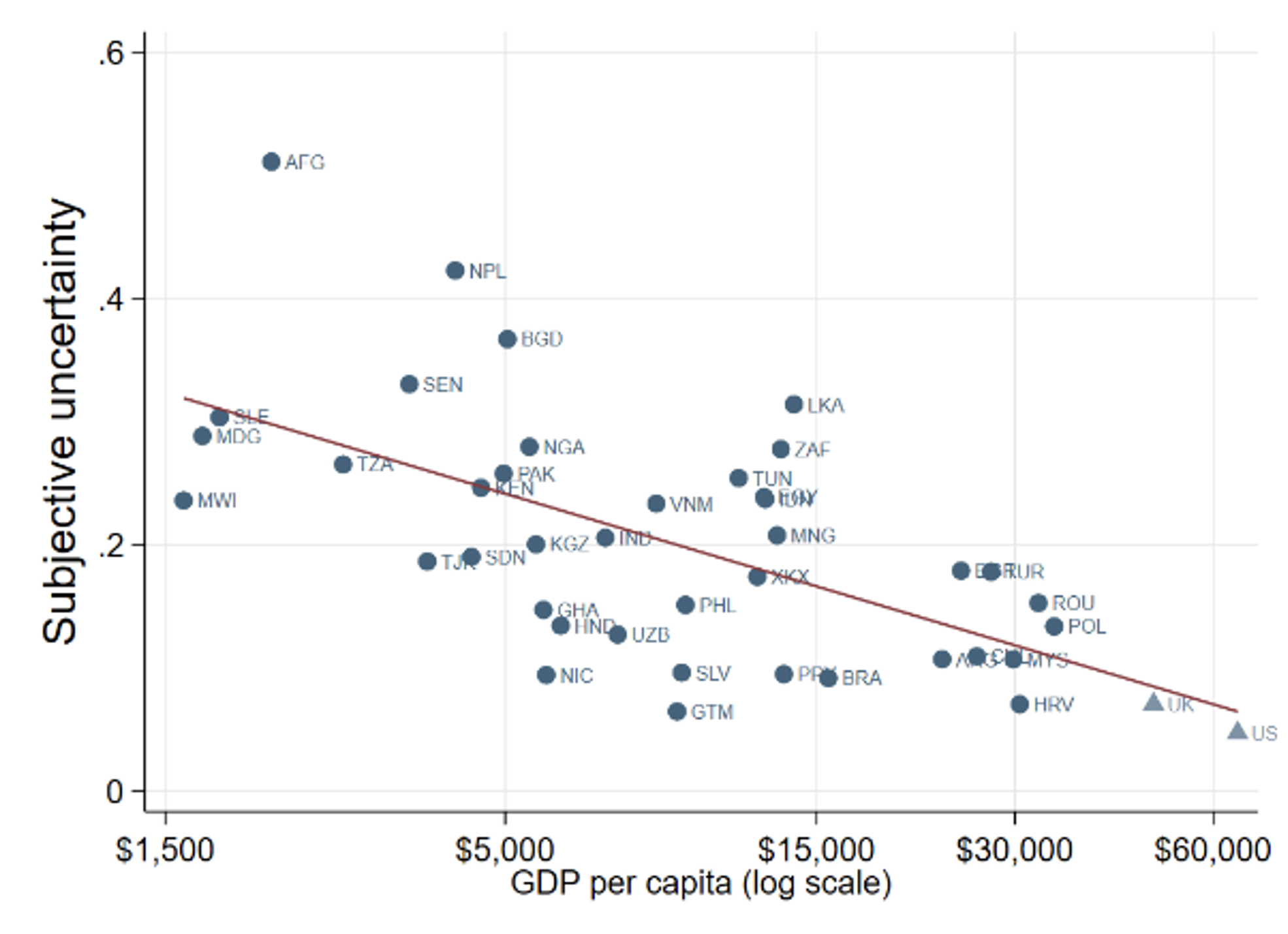

Second, there are systematic differences in business uncertainty across countries at different levels of development—a new stylized fact. Businesses in poorer countries, i.e., those with lower levels of GDP per capita, tend to have higher levels of uncertainty on average (Figure 3). Prior research had shown that employment, sales, and investment data are more erratic in lower-income countries. But now it is clear this is not due to low-quality or noisy data. Instead, business managers actually perceive uncertainty to be three to six times higher in those low- and middle-income countries than in the U.S. or U.K. Thus, high levels of business uncertainty are likely to distort investment and hiring patterns in lower-income countries. This finding brings researchers one step closer to showing that, indeed, some countries might fail to develop and grow because their unpredictable business environment encourages firms to wait and see too much, rather than invest and improve their productivity.

Third, the negative relationship between uncertainty and GDP per capita is not easily explained away. It does not seem to come from differences in the composition of the business sector across countries. It is also not systematically related to the volatility of exchange rates or business cycles, which are often higher in the developing and emerging world. Instead, there appears to be a robust relationship between economic development and the amount of risk and unpredictability (i.e., uncertainty) that businesses perceive in their economic environment.

Figure 3. Employment-weighted business uncertainty declines with GDP per capita.

Notes: This figure plots employment-weighted subjective uncertainty in each country averaging across waves of the World Bank Business Pulse and Enterprise Surveys against the country’s 2019 GDP per capita on the horizontal axis. We weigh firms by employment within each country. U.K. and U.S. values taken as the averages for Apr 2020 – Dec 2021 and Apr 2020 – Mar 2022 respectively.

Notes: This figure plots employment-weighted subjective uncertainty in each country averaging across waves of the World Bank Business Pulse and Enterprise Surveys against the country’s 2019 GDP per capita on the horizontal axis. We weigh firms by employment within each country. U.K. and U.S. values taken as the averages for Apr 2020 – Dec 2021 and Apr 2020 – Mar 2022 respectively.

Policy implications

The evidence from these World Bank surveys has at least two policy implications. First, Central banks and governments in low- and middle-income countries can feasibly collect forecasting and uncertainty data as part of their routine business surveys, and thus obtain timely information about the business outlook. Such data could be a boon to policymakers and researchers interested in macroeconomic fluctuations and firm dynamics in these countries. Moreover, country-specific surveys could also collect forecasts and uncertainty data about prices, employment, or investment which could be useful for the conduct of monetary, fiscal, and business development policy.

Second, addressing and lowering the amount of uncertainty that businesses perceive through specific policy interventions could play an important role in supporting firm investment and growth in developing countries, generating positive effects for the macroeconomy. And the economic gains from making business uncertainty a higher policy priority could also bring greater stability to the political and social spheres, which in turn matter for the business environment.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Measuring business uncertainty in developing and emerging economies

July 29, 2022