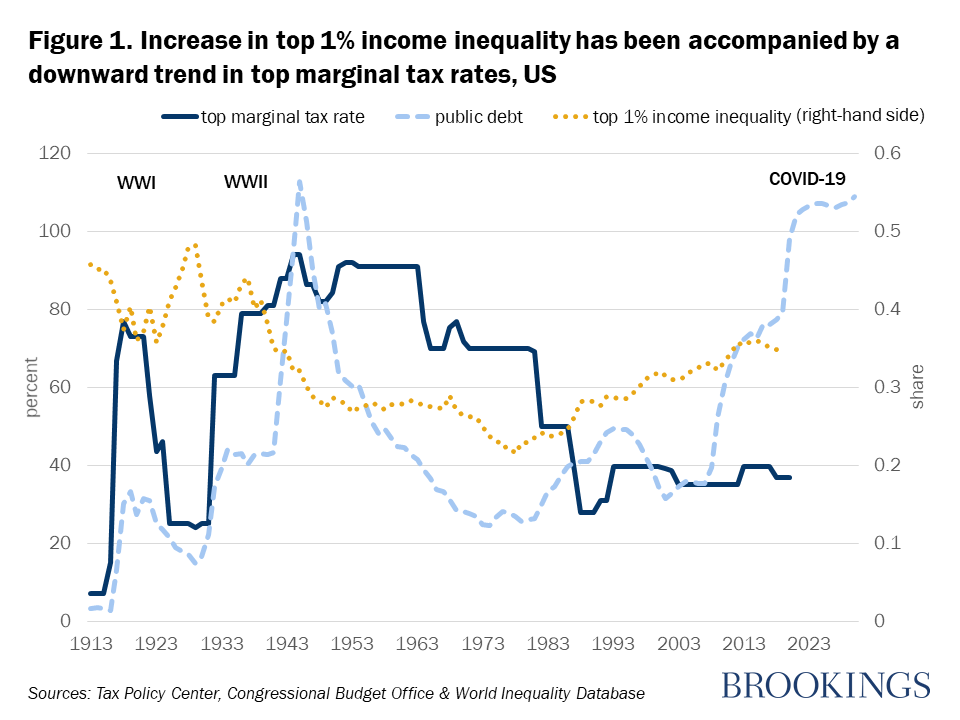

At the end of World War I, J. A. Schumpeter coined the term “thunder of history” to describe the historical roots of fiscal systems. Indeed, wars, revolutions, and disasters persistently shape domestic tax systems. For instance, the two world wars gave way to new taxes—notably the income tax—that are still in existence and reflect the thundering of history. In the United States, the world wars’ effects on top marginal tax rates contrast with the more recent period where the increase in top 1 percent income inequality has been accompanied by a downward trend in top marginal tax rates (see Figure 1). Fast forward to today, fighting COVID-19 is in many ways analogous to fighting a war. One might thus wonder what the legacy of COVID-19 will be for our tax systems 10 or 20 years from now.

The COVID-19 crisis is an opportunity to renew the “social contract.” The disease reinforces the role of the state in protecting against health risk and in its social transfer programs to shield the citizenry against the economic consequences of the health crisis. COVID-19 has thus reasserted the need for an effective state and may help improve the willingness of the citizenry to pay tax.

There is a strong rationale for the introduction of a wealth tax post-COVID-19, as there is after all calamities such as wars and other pandemics. What is more, the older generations who have been the most vulnerable to the disease are richer than the younger generations who have been most hit economically by the containment measures. That may further justify a wealth tax. Yet, the implementation and effectiveness of a wealth tax have been challenged in the United States where the debate has been raging. For developing countries facing much bigger challenges in tax administration and compliance, a more pragmatic approach would be the introduction of a real estate tax for property beyond a certain threshold in the richest neighborhoods of Africa’s large cities.

Beyond a potential property tax, COVID-19 offers an opportunity for developing countries to rethink their tax policy to contribute to the reconstruction effort and promote recovery. There are three levers to support this needed rethink.

1. Governments should both reinforce tax administration and promote tax simplicity

Too often, economists obsess over tax rates while overlooking issues related to implementation, including those related to tax administration and compliance. Weaknesses in the area of tax administration combined with complex tax codes can lead to important leakages, in turn making governments lose resources to finance much-needed economic development. Beyond domestic tax administration, customs remain important and are often the main tax collectors in developing countries. The cooperation between customs and tax authorities for countries without a tax revenue agency is therefore essential for effective enforcement of the tax laws. Often, developing countries suffer from the fragmentation of taxing power between ministries, which contributes to the complexity and the multiplicity of actual tax regimes. Designing taxes that are simple to administer is the way to go.

There is a risk that the post-COVID-19 era will lead to the proliferation of supplementary tax regimes in order to promote economic recovery. Such a proliferation may complexify actual tax regimes, thereby making the assessment and publication of tax expenditures a high priority to safeguard the tax system and improve fiscal transparency. In such a context, the tax exemption of foreign aid appears unwarranted.

Additionally, economies that depend on oil and other natural resources often have tax exemptions combined with royalty schemes to support investment in the sector. The peril with such exemptions is that they are often abused and could lead to a crowding out of tax revenues in other sectors. To address the challenge, it is important to “ring-fence” exemptions to ensure there are no loopholes, including a strict definition of subcontracting firms that are eligible for exemptions. While increasing taxes on moribund economies would not be advisable, in a forthcoming paper, we provide evidence that corporate income tax holidays are a giveaway. Tax credits should be systematically preferred to tax holidays.

2. Consider using taxation for industrial policy and encouraging formalization

For instance, the use of tax incentives has allowed China to direct raw-materials producing firms away from exporting the raw product and toward selling to manufacturing firms. Hence these tax incentives have increased the added value for the Chinese economy.

Specifically, offering tax credits on (capital) inputs to promote the transformation of raw products while taxing exports of the latter can be a powerful transformative tool for economic development.

Developing countries, including those in Africa, need to build new comparative advantages away from exporting raw products. To do so, the private sector needs to be incentivized to innovate and venture into higher technology sectors. Lobbies of importers can make it difficult and influence the design of policies including taxes and tariffs away from the promotion of domestic productive systems.

Taxation can play a role in encouraging and smoothing the formalization of the informal sector. The informal sector is a contestable sector in that it has low barriers to entry but it suffers from chronically low productivity and low profitability. The informal sector should not be punished for being informal but rather incentivized to move up the “sophistication” ladder. One avenue is through the design of a value-added tax (VAT) that can help encourage formalization. Indeed, adjusting the VAT threshold liability—the level at which a firm is subjected to VAT—can encourage small farmers to get a rebate on their investments and hence move up the value-add chain.

3. Look beyond taxation when approaching the issue of revenue mobilization

We need to make financial systems work for development. Too often, financial systems, namely banks, do not fulfill their basic functions—which include information production, price discovery, monitoring, and payment systems, as well as resource mobilization. When financial systems function properly, savings both domestic and foreign are allocated toward productive investments through the core banking functions. Optimal allocation occurs through a combination of better macro policies and more competition in the financial system—which includes fintech operators, who are making headway on payment systems including in many developing countries.

In sum, the key to a successful recovery from COVID-19 lies in governments eliminating all forms of leakages in public resources both on the spending and revenue sides. To do so they should reaffirm the social contract and enhance tax administration and transparency—including in the natural resource sector. Governments also need to look beyond taxation to mobilize savings into much-needed investment for developing countries.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

COVID-19’s ‘thundering’ effect on taxes

February 18, 2021