On January 27, the Brookings Africa Growth Initiative (AGI) launched its Foresight Africa 2021 report with an interesting panel discussion. One of the speakers, Vera Songwe of the U.N.’s Economic Commission for Africa and AGI, emphasized the good news. Africa had surprised everybody with its resilience during the coronavirus crisis. African economies had shown the world that they were no longer helpless in the face of big shocks: They could collectively raise nearly $50 billion in resources to combat the crisis and freely tap private credit markets instead of relying on foreign governments and development agencies. This could not have happened without structural progress.

The second feature that defines the new Africa is divergence: Half the countries on the continent were middle-income economies, not a collection of low-income least developed economies. Heterogeneity has always characterized Africa; it now defines the region’s economy.

The third encouraging development was integration. This year, hopes are even higher because of the African Continental Free Trade Area (AfCFTA) that came into effect on January 1. The expectation is that the continent’s economies will be remade:

“AfCFTA will cover a market of more than 1.2 billion people and up to $3 trillion in combined GDP, with the potential of increasing intra-African trade by over 50 percent, according to the United Nations Economic Commission for Africa. According to the World Bank, meanwhile, the agreement could add $76 billion in income to the rest of the world. On its completion, the AfCFTA will become the largest free trade area in the world since the establishment of the World Trade Organization.”

The other panelists seemed to agree. In 2020, Africa had shown the world it could handle its problems on its own; in 2021, if its policymakers started creating jobs, Africans could again wow the world with a quick recovery and structural renewal.

While much is being made of the permanent or structural consequences of the pandemic such as quickened digitalization of economic activities, most developing countries have yet to deal with large structural backlogs of the analog kind.

Coincidently last week, along with Giovanni Zanalda at the Duke University Center for International and Global Studies, we were working to update Africa’s sovereign debt scenarios. Foresight Africa and the panel discussion raised several questions. Has the debt relief championed by David Malpass of the World Bank and Kristina Georgieva of the International Monetary Fund for low-income economies materially improved their growth trajectories? Meanwhile, how are Africa’s middle-income economies faring? Should debt relief be extended to middle-income economies as was argued here last year when the virus first hit, or is this no longer necessary now that Africa has done so much better than expected? Is there a “debt-development doom loop” in sub-Saharan Africa that will once again derail progress?

We figured it might be useful to share our main findings right away. Readers should note that our paper and this blog are about sub-Saharan Africa (SSA). Foresight Africa and the panelists discussed developments in North Africa—mainly Algeria, Egypt, Libya, Morocco, and Tunisia—as well. But it doesn’t change our conclusions very much.

Divergent development

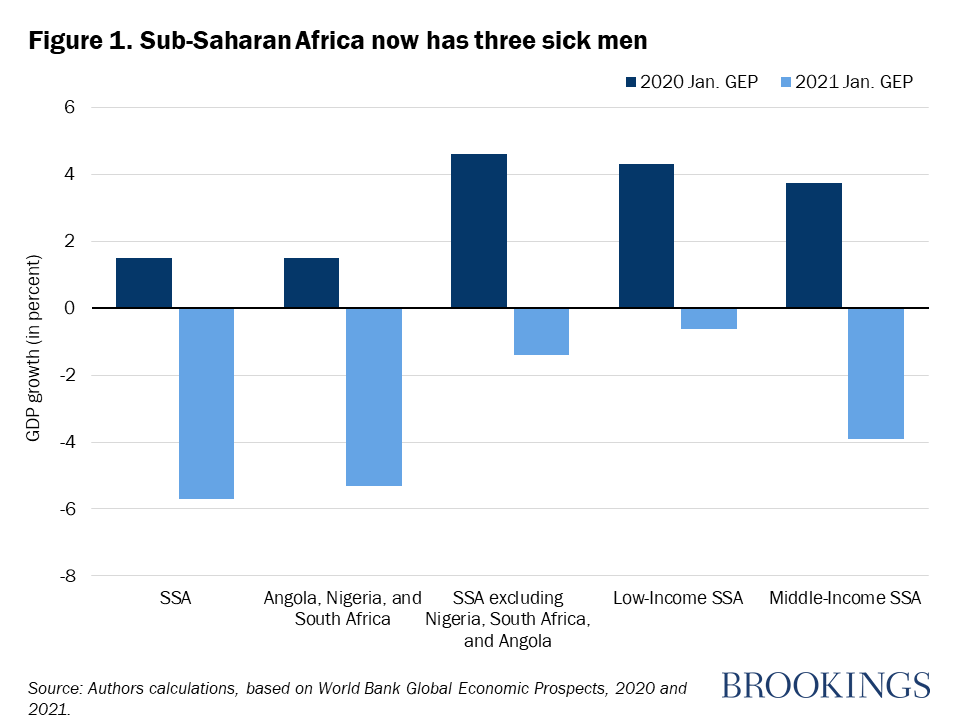

There is indeed a divergence among SSA’s economies, but the fault line is not between least developed and middle-income. The drift is between the sick and the healthy. We contrasted growth expectations for 2020 when the year began with what actually happened, using the World Bank’s last two January Global Economic Prospects reports. Figure 1 summarizes the forecasts. Collectively, low-income economies in the region staved off a big contraction and middle-income economies contracted by 4 percent instead of growing by nearly as much. But what really matters for the region’s economy is how Nigeria, South Africa, and Angola have been faring. They add up to about two-thirds of SSA’s GDP, and nothing—neither a debt moratorium nor a continental trade accord—will mean much unless they start doing a lot better. Last year, they were not expected to do well. They ended up doing horribly.

The heterogeneity that now matters most is within middle-income Africa: between the three biggest economies and the rest. Developments in Botswana, Lesotho, and Seychelles—even in Côte d’Ivoire, Ghana, and Senegal—are worth cheering, but they cannot offset the depressing drag in Angola, Nigeria, and South Africa. Europe seems to have one sick man at a time; for the past few years, Africa has had three.

Divergent debt

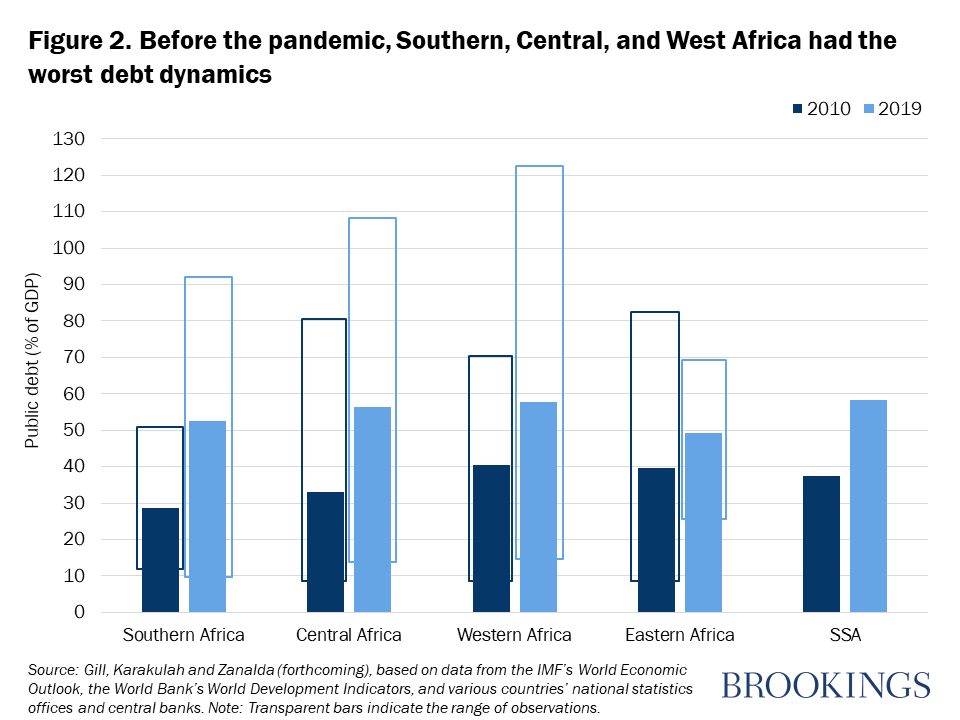

In the decade before the COVID-19 pandemic, debt-to-GDP ratios rose across the region. Figure 2 presents a synopsis of sovereign debt patterns in the region. Between 2010 and 2019, debt-to-GDP ratios nearly doubled in Southern and Central Africa. In West Africa, the rise was less steep, but some countries in the subregion appear to have been in trouble before the crisis.

It may not be a coincidence that these three subregions each have one of the big three economies. The increase in public-debt-to-GDP ratio during 2010-2019 was 30 percentage points among oil exporters, twice as high as for other countries. It is not a coincidence that 9 out of 11 countries in East Africa are not resource-based. Notably, during this period of decent growth, only eight countries were able to reduce public debt ratios: Botswana, Zimbabwe, Comoros, Seychelles, Sao Tome and Principe, the Democratic Republic of Congo, Guinea, and Côte d’Ivoire.

An African ‘debt-development doom loop’?

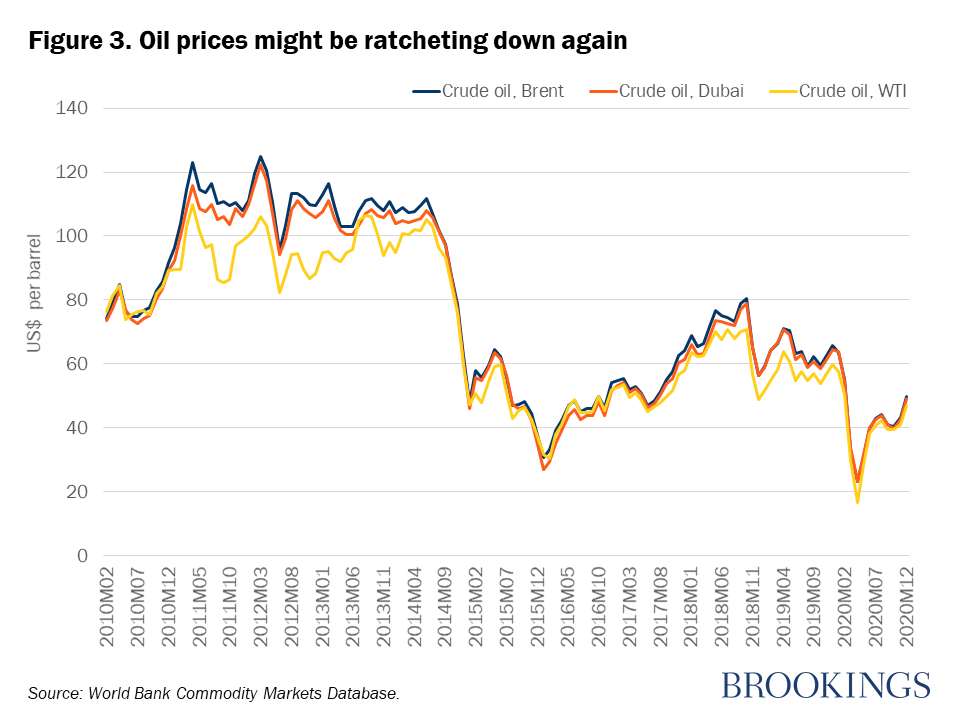

We know that weaknesses in commodities markets translate quickly into economic setbacks for Africa. This is especially the case for oil and gas, though it might also be the case for minerals and metals. In the five years before the coronavirus contraction, oil prices had fallen from about $100 a barrel to around $50; in 2020 they averaged about half of that. The prospects for a quick recovery are remote.

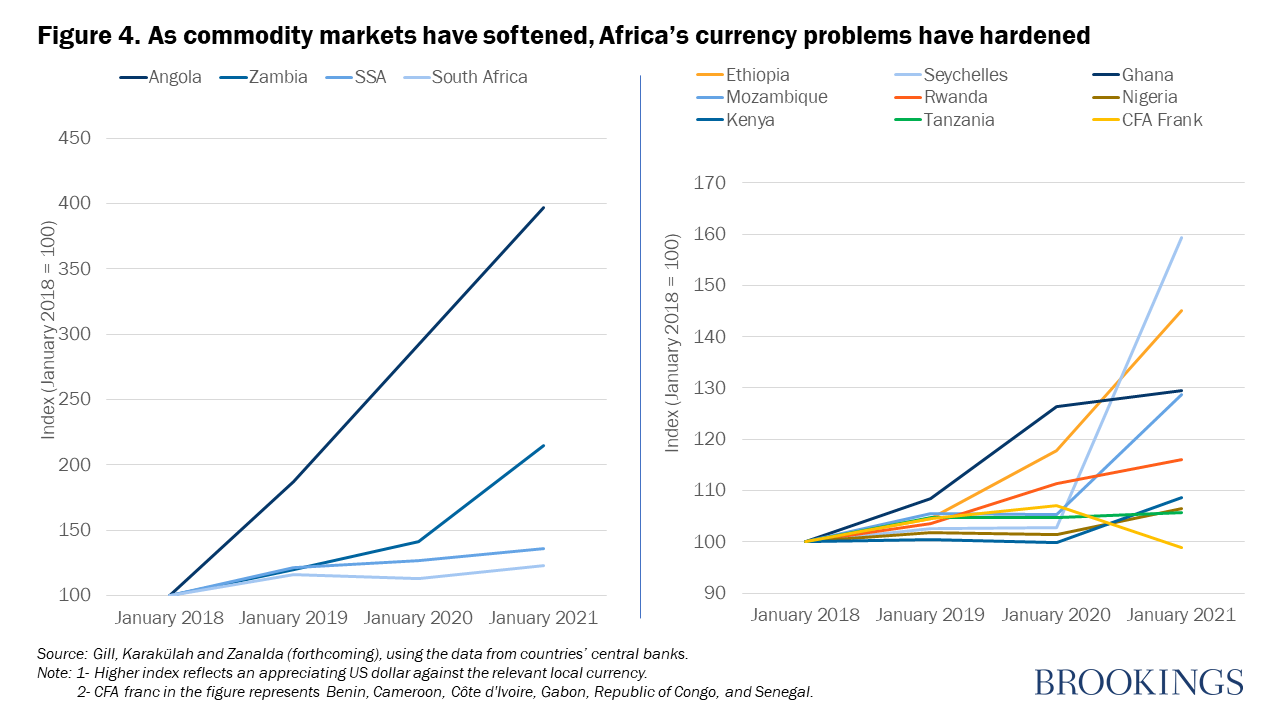

Other commodity prices were also declining and, in the first half of 2020, got pushed down by the pandemic. On average the price drop was about 10-20 percent in core commodities, such as aluminum, copper, and platinum. This doesn’t seem like a lot, but it was enough to create sizable fiscal problems for resource-rich countries. And, in most emerging economies, currency crises tend to follow close behind such pressures on public finance. As if on cue, currency problems have started plaguing the weakest economies in Africa.

During the last few years, the U.S. dollar has remained roughly stable against the currencies of major U.S. trade partners and against most emerging market currencies. But African currencies did not follow a similar trajectory. Currencies of all 45 countries in the subcontinent depreciated against the U.S. dollar in 2018, and in 2019 fewer than a dozen countries saw their currencies appreciate a bit in 2019 (ranging from 0.1 percent to 5.3 percent). Since January 2018, the cumulative depreciation in the subcontinent has been about 36 percent, with the currencies of Angola, Zambia, Seychelles, Ethiopia, and South Africa falling the most. This has spelled serious trouble for some of them. External public debt constitutes 67 percent of Angola’s GDP, and the Angolan kwanza has lost about 75 percent of its value against the U.S. dollar since January 2018. The value of the Zambian kwacha against the U.S. dollar has more than halved since January 2018, and the country’s external public debt is about 68 percent of GDP. These are warning signs for the entire subcontinent.

Commodities play an important role in most developing countries. In SSA, because of China, their role is both big and somewhat unique. In 2016, more than a third of the total loan finance by China to Africa was secured by commodity exports. In countries like Angola, this ratio is much higher. Coulibaly, Gandhi, and Senbet (2019) point out that as countries in SSA accessed financing through commodity-backed loans, creditors such as China enjoyed reduced lending risks. Now, as a result of the collapse in oil prices, Angola and others are liable to send higher commodity volumes to China to meet repayment terms. In other words, commodity exporters in SSA face a double whammy due to the drop in commodity prices: Falling prices reduce government revenues, and commodity-backed loans reduce supplies available for new sales. For countries with close economic relations with China, the spiral could quickly become vicious.

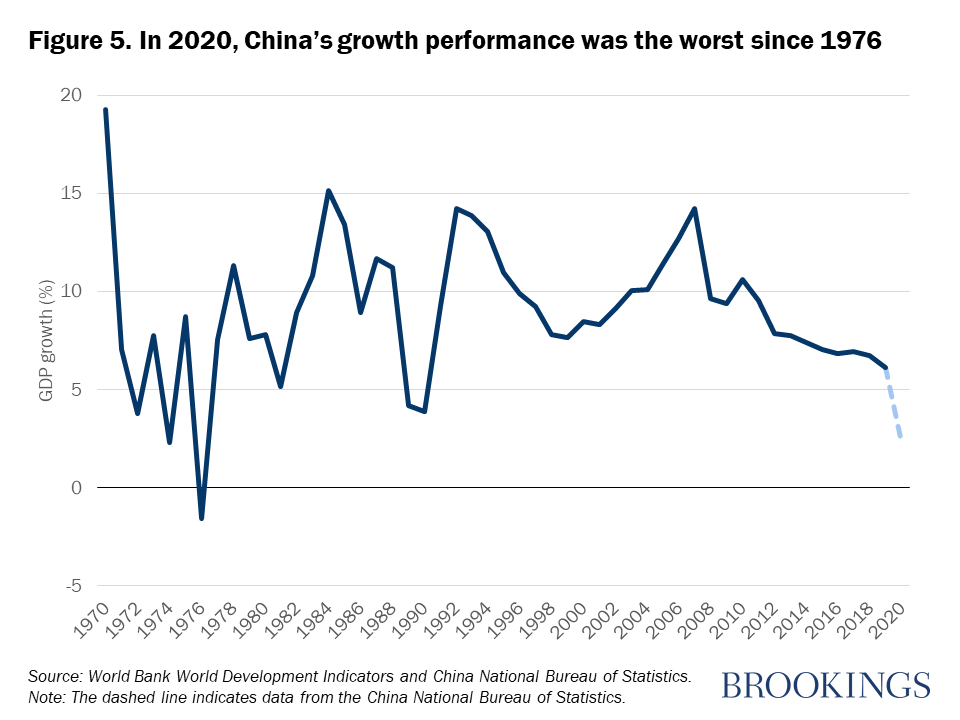

If this were not bad enough, SSA also faces the prospect of lower terms of trade due to China’s declining growth. In 2020, China’s economy was expected to avoid a contraction, but not by a lot (Figure 5).

China is now the largest trading partner for Africa, but also it is the largest financier of the construction of infrastructure including railways, roads, power plants, and ports. Since the 2000s, China’s activities in SSA have aided economic growth in both Africa and China. Sub-Saharan Africa needed long-term finance and China became a steady source of trade credits, direct investments, and official aid. In the 2010s, China financed Africa’s infrastructure more than did multilateral development banks. In addition, China became a reliable source of countercyclical finance for most countries in the subcontinent. A slowdown in China’s growth will turn into less financing for infrastructure in Africa at a time when it needs it most.

Macro-agenda 2021: Commodities, currencies, and China

While much is being made of the permanent or structural consequences of the pandemic such as quickened digitalization of economic activities, most developing countries have yet to deal with large structural backlogs of the analog kind. Especially serious structural shortcomings in Africa make the linkages between economic development and sovereign debt its Achilles heel. In 2021 as in 2019, the most important items on Africa’s macroeconomic agenda will soon be commodities, currencies, and China—not the economic exigencies associated with COVID-19. Its policymakers should start paying more attention to them.

Related Content

2021

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Did Africa turn a corner in 2020 or did it just dodge a bullet?

February 5, 2021