COVID-19 is a unique, severe. and unprecedented health and economic crisis that is changing our lives. Three things make it unique. First, it is a rolling combination of a health pandemic and an economic crisis. Second, the crisis has turned global in record time. Third, it is both a demand and supply side shock to all the major economies. The damage caused by the virus and the policy responses it requires are deep and multifaceted. Its effects can be grouped into three categories.

- Human suffering. The rapid loss of life and deterioration of health outcomes, but increasingly also economic suffering through loss of jobs and other incomes. In a little over three months, more than 150,000 people have died and more than 2.1 million have been infected. As small and medium enterprises are hammered by the lockdowns, many workers have lost their jobs or are working on reduced work schedules. If the economic suffering is prolonged and as deep as expected, this will hurt people—especially the poor—in other ways as well, such as education, indebtedness, and nutrition.

- A severe global economic recession. It is now a foregone conclusion that the global economy will slip into a recession in 2020. What we don’t know is how deep, long, and widespread the contraction in economic activity is going to be. As a result of the unprecedented sudden stop in global economic activity, 2020 is on track to witness the deepest global recession on a scale not seen since World War II. At the World Bank, we are projecting GDP to contract in all developing regions (ECA, LAC, MENA and Africa) except Asia. Even in Asia, the sudden slowdown will feel like a recession.

- Deep financial and corporate sector distress. The financial and corporate sectors are likely to suffer large scale deterioration. Markets have taken a big hit, financial systems are under stress, and banks are likely to see huge pressures on their balance sheets. Private firms are being hurt by the collapse in demand. The likelihood of large-scale bankruptcies is rising. Rapidly increased risk aversion among investors has led to a sudden stop in capital flows to emerging markets.

By itself, each of these three adverse outcomes is devastating. But because these outcomes are mutually reinforcing, their combined threat is even more ominous. The world will have to bear the consequences of the coronavirus for years if the policy response is late, weak, or uncoordinated.

The solution: Simultaneously flatten the pandemic, recession, and financial distress curves

Pandemics, economic downturns, and financial crises are mutually dependent. And the deeper and longer these crises are, the more pernicious their combined impact. This means that they need to be mitigated at the same time:

- Flattening the pandemic curve is important because it saves lives by avoiding bottlenecks in the health system when larger numbers of sick exceed the health system’s capacity.

- To the greatest extent feasible—which will be different across economies—deep and prolonged recessions must be avoided, for these can cause lasting damage. Long periods of weak supply and demand can lead to elevated structural unemployment, permanently lower capital stock, and contained “animal spirits.” Flattening the recession curve is therefore important.

- Finally, during episodes of deep financial and corporate distress, even productive banks and firms can experience widespread failures. The fiscal cost of bailing out banks and firms can become prohibitive, forcing governments to then cut back on other productive spending. This argues for the need to flatten the financial distress curve at the same time.

Simultaneous action on all these fronts requires greater resources—medical, fiscal, financial, and monetary. It also puts a premium on efficiency. In other words, developing countries need a strategy to leverage both public and private resources in a hurry. At the World Bank, we have been working on a framework that their governments could use to devise strategies tailored to their circumstances—health-sector capacity, fiscal space, financial sector development, and monetary headroom.

A framework for flattening the curves

Policymakers should be guided by three general principles:

- Do not be bound by convention. The immediate policy response to the current situation has to match its nature and focus on limiting the virus outbreak and managing the crisis. Governments across the world have to do what it takes, fast, and in a coordinated way. It is important for the policies to be multidimensional, bold, and unbound by convention.

- Pay special attention to sequencing. The immediate focus has to be on measures to contain the spread of the pandemic and to treat the infected. The policy focus is then quickly shifting to providing help to cash-strapped individuals and firms to just keep them afloat until the pandemic begins to ebb. Governments need to move swiftly in this regard, but should also remain cognizant of the fiscal and economic realities, leaving as much fiscal space as possible for the next phase. A fiscal stimulus in the current circumstances of suppressed demand may have little impact on economic activity but it will make a big difference once people start returning to work.

- Distinguish between the terms of the trade-offs. In the short term, the health toll will cause a deep economic contraction. But over the medium to long term, there is no trade-off between the aggressiveness of health interventions and economic activity. Research on the 1918 pandemic suggests that while pandemics have large short-term costs, “non-pharmaceutical interventions can lead to both better economic outcomes and lower mortality rates.”

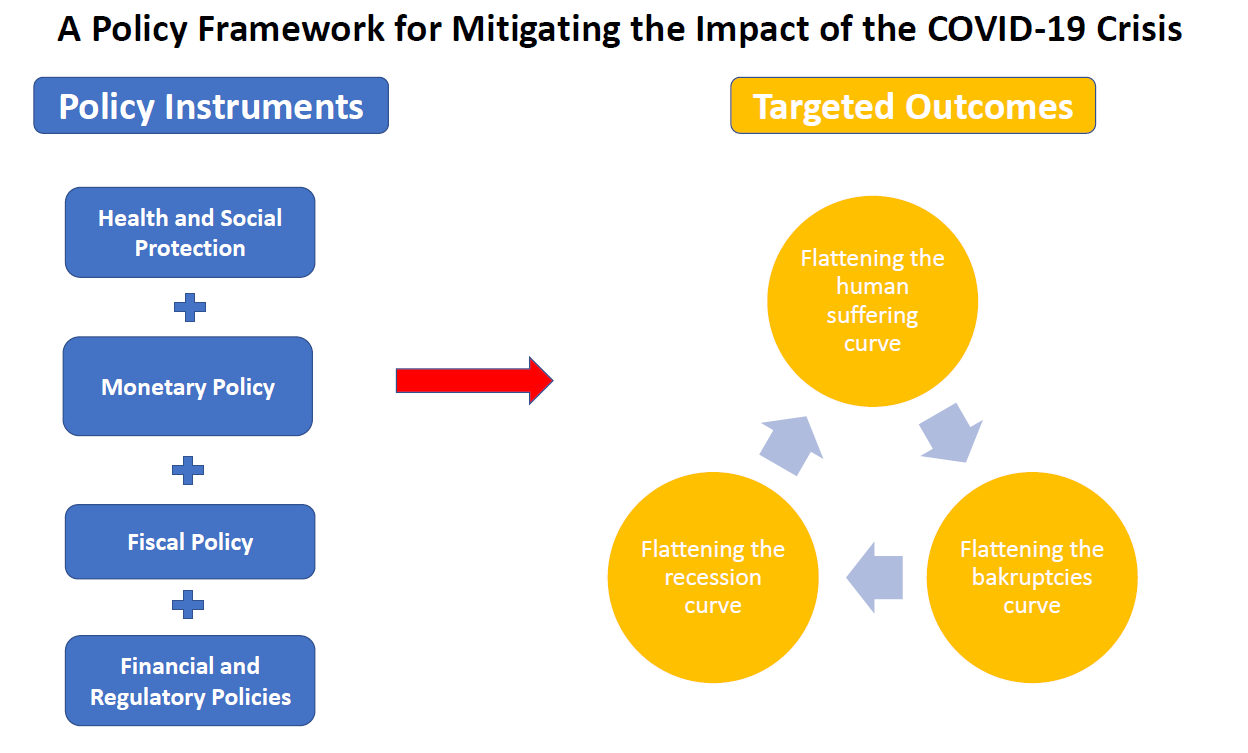

A swift, simultaneous, and sequenced implementation of four sets of policy instruments is needed to flatten the three curves discussed above:

- Health and social protection. These are the priority government policies, ranging from testing and treatment, to hiring new medical staff, to expanding social assistance and implementing cash transfers to households.

- Fiscal policy. Measures include efforts on the revenue side (deferring filing and payment, reducing social contributions), spending (low-interest loans to firms, reprioritizing spending), and financing of the larger fiscal deficit.

- Monetary policy. Many countries may have room to cut policy rates. Providing liquidity to solvent banks is also important.

- Financial, industrial, and trade policies. Interventions include bank forbearance on domestic private loans with certain strict preconditions so as not to create financial instability down the road, reductions in collateral requirements, canceling all but the most necessary procedures for firm registration, and reducing import restrictions and tariffs.

Figure 1 illustrates the main elements of the framework.

It is important that these measures are timely, time-bound, targeted, and transparent. At some point—sooner rather than later for most countries—governments will need to readjust these mitigation efforts and the strict measures will have to be eased. Right now, governments have to do all they can to limit the health, economic, financial, and corporate distress. But soon they will have to begin to think about the shift to the next phase of economic policies. The biggest part of an effective response is a quick escalation of social, fiscal, and financial policy measures, but steering the economy back to normal is also a critical component of crisis management.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

A policy framework for mitigating the economic impact of COVID-19

April 20, 2020