Property insurance is a critical foundation of U.S. real estate markets. It protects property owners and lenders from catastrophic losses, supports mortgage lending, and helps stabilize communities after natural disasters. But in recent years, the cost of commercial property insurance has risen sharply. Minjoo Kim, Prateek Mahajan, and Zirui Wang of the University of Texas at Austin examine who ultimately bears these rising costs and how insurance markets are reshaping commercial real estate.

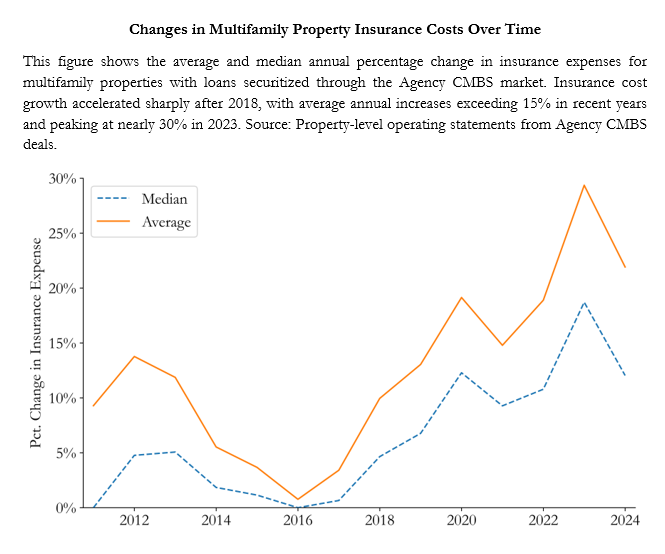

Using property-level data from Agency Commercial Mortgage-Backed Securities deals covering more than 100,000 multifamily properties across the U.S, the authors find that between 2019 and 2024, average commercial property insurance premiums have grown more than 15% a year—and by nearly 30% in 2023. Insurance costs have roughly doubled as a share of rental income and operating expenses over the past five years, transforming what was once a modest operating expense into a significant financial burden.

The study finds that rising insurance costs are not confined to a handful of hurricane-prone coastal markets. While states such as Florida, Texas, Louisiana, and California have experienced some of the largest increases, substantial cost growth has also occurred across much of the country. The increase appears across multiple commercial real estate sectors, suggesting a broad repricing of climate and catastrophe risk rather than a localized phenomenon. The paper focuses mainly on multi-family housing.

The research identifies three major forces driving this repricing.

First, insurers have become much more sensitive to local disaster risk. Prior to 2018, commercial insurance costs were only weakly related to measures of climate and catastrophe exposure. Since then, insurers have increasingly incorporated both expected and realized disaster losses into pricing decisions. Properties located in areas with greater flood, wildfire, hurricane, or other disaster risks now face substantially larger insurance increases.

Second, rising reinsurance costs have amplified the increase. Reinsurance—the insurance that insurers purchase to protect themselves against large losses—has become significantly more expensive. States whose insurers rely heavily on reinsurance markets have experienced especially large increases in commercial property insurance costs. This means that a national increase in catastrophe risk pricing does not affect all locations equally; it disproportionately impacts properties in riskier regions and states with greater dependence on reinsurance markets.

Third, the study finds evidence that regulatory constraints in homeowners insurance markets may be spilling over into commercial insurance. In states where homeowners insurance premiums face greater regulatory limits, insurers may have less flexibility to fully price risk in residential policies. The authors find evidence consistent with some of those costs being shifted into commercial insurance lines, creating an indirect channel through which renters and commercial property owners may help absorb costs that homeowners do not fully bear.

The authors then turn to the question of who bears the rising costs—landlords or tenants. The answer has changed over time. Earlier in the study period, property owners were often able to offset much of an insurance increase through higher rents. On average, roughly half of insurance-cost increases were reflected in rents. Rent pass-through was strongest in markets where housing supply was constrained, places where owners have greater market power, and tenants have fewer alternatives.

However, the ability to pass costs through to renters has weakened substantially. By 2024, the relationship between insurance-cost increases and rent increases had nearly disappeared. As insurance shocks have become larger, property owners appeared increasingly unable to recover those costs through higher rents. Instead, the burden showed up in lower net operating income, reduced profitability, and weaker property valuations. The study estimates that in the areas experiencing the largest insurance increases, net operating income may have fallen by more than 25% over the past decade.

The effects extend beyond cash flow. Properties in higher-risk locations are increasingly selling at lower prices and higher capitalization rates than before 2018, suggesting that investors are pricing climate-related insurance costs as a persistent drag on future returns. In other words, rising insurance costs are becoming capitalized into commercial real estate values.

The study also finds that insurance costs are not distributed evenly across property owners. Larger owners consistently secure lower insurance costs than smaller owners, particularly in high-risk areas. Owners with more diversified and lower-risk portfolios also obtain more favorable pricing, even when insuring otherwise similar properties. These advantages appear to reflect economies of scale, bargaining power, insurer relationships, and portfolio diversification.

As climate-risk repricing has intensified, these owner-level advantages have become more important. High-risk properties owned by smaller investors are increasingly likely to be sold, and when they are sold, they are more likely to be acquired by larger owners. The result is a gradual reallocation of climate-exposed assets toward larger firms that appear better positioned to manage rising insurance expenses.

Authors

Related Content

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Who bears rising commercial property insurance costs?

July 7, 2026