To address climate change, scientists have long recommended reducing greenhouse gas emissions (mitigation), helping people adapt to a warming climate (adaptation), and removing the excess greenhouse gasses in the atmosphere (carbon dioxide removal). While the climate policy debate in the U.S. has focused primarily on reducing emissions, emerging carbon dioxide removal technologies are starting to receive more attention.

These technologies are critical as countries fall short of emission reductions necessary to achieve the goals of the 2015 Paris Agreement, which called for limiting global average temperatures to “well below 2°C above pre-industrial levels and pursuing efforts to limit the temperature increase to 1.5°C above pre-industrial levels.” Despite widespread climate action across numerous countries in landmark climate agreements, the world is still projected to fall short of this 1.5°C target. While global climate action has pushed incentives towards clean energy adoption, the transition will take time due to increasing global energy demand, technological lock-in, and entrenched economic and political interests. In this context, achieving global climate goals will require some form of carbon dioxide removal.

What is carbon dioxide removal?

Put simply, carbon dioxide removal means taking carbon dioxide (CO2) out of the atmosphere. The focus on CO2 is important because of the central role it plays in climate change. Due to its unique chemical properties, CO2 tends to linger in the atmosphere for a long time, trapping heat and exacerbating global warming. The scale of the problem is massive. Humans have released nearly two trillion tons of CO2 into the atmosphere since the industrial revolution, requiring solutions that go beyond emissions reduction. Carbon dioxide removal is one such solution.

There are many ways to mitigate atmospheric carbon dioxide, and experts use different terms to describe those pathways. Carbon dioxide removal (CDR), the most general term, refers to any human activity that intentionally removes CO2 from the atmosphere and durably stores it. In contrast, carbon capture extracts CO2 before it enters the atmosphere, usually from a point source, such as the smokestack of a power plant. While carbon capture prevents new carbon emissions, only CDR tackles the abundance of carbon in the atmosphere. Both approaches—removal and capture—have their benefits, and we’ll cover both in this article.

To support climate efforts, CO2 removal and capture initiatives must overcome three core technical challenges:

- The CO2 must be intentionally removed from the atmosphere or captured at the point of emission.

- The removed CO2 must be stored or sequestered1 so that it is unlikely to return to the atmosphere.

- The storage must last long enough to compensate for the energy required to remove and store it.

There are many ways to overcome these challenges, resulting in several distinct carbon dioxide removal and capture approaches, some of which we will cover below. However, as we will see, no approach is perfect, and experts increasingly discuss carbon dioxide removal efforts as a way of buying time for the technology to mature while reducing the overall harm of CO2 emissions.

How can we remove carbon dioxide from the atmosphere, and how much does it cost?

There are many ways to accomplish carbon dioxide removal and capture with more on the horizon. In this section, we explore a few of the prominent approaches, roughly in the order of ease of implementation given the state of current technology, which could change rapidly. These include removal through forests, carbon capture and storage (CCS) or utilization (CCU), marine carbon dioxide removal, and direct air capture (DAC).

Removal through forests: Afforestation/reforestation, improved forest management, agroforestry

Today, the vast majority of carbon removed from the atmosphere happens because of trees and plants. Trees and plants store carbon both above ground in the trunks, stalks, branches, and leaves, as well as in the roots below ground, through photosynthesis. By increasing the number of trees and plants absorbing CO2, humans can reduce the amount in the atmosphere. There are a few ways to do so. Afforestation refers to creating new forests on land that historically has not contained forests. Reforestation refers to converting land to forest that previously contained forests before it was converted to another use. Improved forest management practices increase the size or density of forests, which increases their carbon stock. Lastly, agroforestry refers to integrating trees and shrubs into agricultural lands.

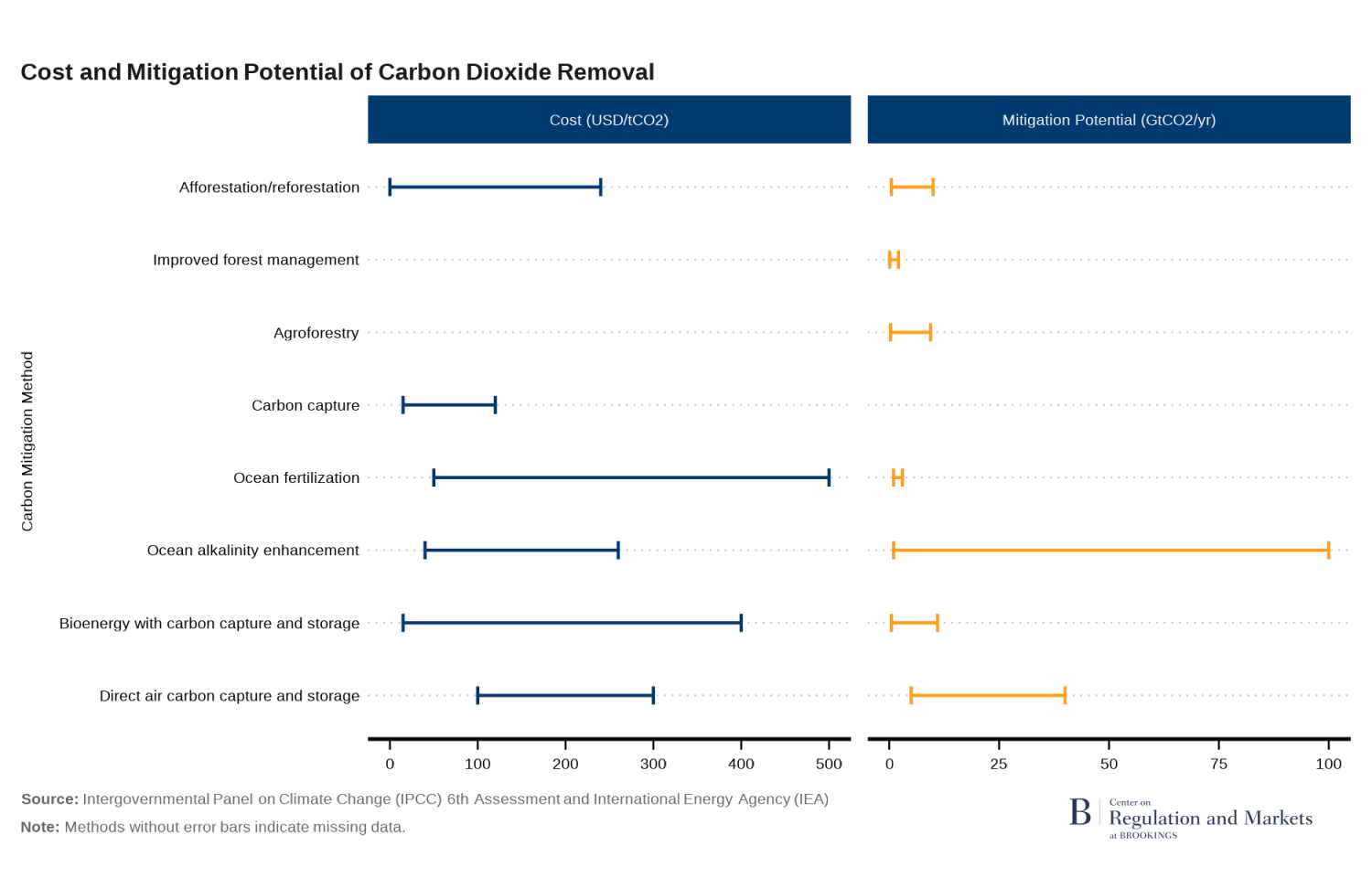

These methods—all of which are considered “conventional” CDR—have been rigorously examined for effectiveness and cost, but their estimated mitigation potential and cost vary substantially depending on assumptions about time horizons, permanence of storage, and accounting methodologies. The IPCC’s latest assessment estimates that afforestation/reforestation could remove, once fully deployed, between 0.5-10 Gt CO22 per year at a cost between $0to $240 per ton of CO2. Agroforestry has a similar mitigation potential of 0.3-9.4 Gt CO2 per year, though the IPCC states that there is not sufficient scientific data to estimate the cost of this strategy. However, a 2023 report sponsored by the German Federal Ministry of Education and Research estimated the cost of agroforestry at €125– €1,144 per ton of CO2 (approximately $132 – $1,210 based on recent exchange rates). Similarly, the IPCC states that there is not sufficient data to estimate the cost of improved forest management.

Carbon capture and storage (CCS) and carbon capture and utilization (CCU)

CCS and CCU have dominated political discussions of carbon removal and capture. CCS is the process of capturing CO2, usually from a point source, such as the smokestack of a power plant, then storing that carbon, often underground. The International Energy Agency (IEA) estimated in 2021 that cost of carbon capture depends on the source of CO2, and could range from $15-25/t CO2 for industrial processes producing highly concentrated CO2 streams, to $40-120/t CO2 for more dilute gas streams, once fully deployed. Unsurprisingly, carbon capture from more concentrated streams, such as ethanol production or natural gas processing, tends to be cheaper than more diluted streams such as cement production and power generation (note that this does not include the transport and storage costs). As of July 2024, five CCS facilities in operation in the U.S. store CO2 using deep saline formations, which are porous, underground rock structures ideal for storing carbon. Most of these facilities are in bioenergy or ethanol industries.

For CCU, the capture of the CO2 is the same as in CCS, but instead of sequestration, the captured CO2 is used for industrial purposes—for example, in concrete, chemicals, plastics, synthetic fuels, or oil field yield enhancements. When CO2 is utilized rather than stored, the climate benefit is likely reduced. However, this depends on the product lifetime, the product it displaces, and the CO2 source. Product lifetime affects how long the CO2 stays out of the atmosphere. For example, CO2 utilized for fuels or chemicals is likely to end up back in the atmosphere within one to ten years, minimizing the climate benefit. As of September 2023, there were 15 CCU/CCS projects operating in the U.S., capturing around 22 million metric tons of CO2 per year, which amounts to around 0.5% of the total U.S. annual emissions.

Captured CO2 can also be combined with green hydrogen3 to produce synthetic fuels. These synthetic fuels can serve as a cleaner alternative to fossil fuels and contribute to net-zero goals. In this case, it matters what fuel product the synthetic fuel displaces. If the synthetic fuel is used in hard-to-abate sectors like aviation, this could have considerable climate benefits. On the other hand, if synthetic fuel prevents usage of cleaner energy sources, this will negate the climate benefit.

Captured CO2 is also used for enhanced oil recovery—a process by which the CO2 is pumped underground into partially depleted oil wells to more easily extract the remaining oil. It is debatable whether or not CCU for enhanced oil recovery could be carbon neutral or negative. This practice also promotes the use of additional fossil fuels, negating some of the climate benefit. While CCU is more economically attractive than carbon capture and storage, permanently storing or sequestering carbon maximizes the long-term benefits for the climate. As of July 2024, 13 CCU facilities in operation in the U.S.4 provided the captured CO2 to oil companies for enhanced oil recovery, with CO2 captured from a range of industries, including the production of natural gas and liquefied natural gas, hydrogen, ammonia and fertilizer, and bioenergy and ethanol.

Marine carbon dioxide removal (mCDR)

Marine carbon dioxide removal (mCDR) involves the removal of carbon dioxide from the atmosphere through a suite of ocean processes. A 2021 National Academies of Sciences, Engineering, and Medicine report analyzed the promise of mCDR. In terms of cost, scalability, and efficacy, ocean fertilization—the process of stimulating phytoplankton growth to increase the ocean’s capacity to absorb CO2—is among the most promising mCDR approaches. They estimate that this method, once fully developed, could remove about 0.1-1.0 Gt CO2 per year at a cost of less than $50 per ton of CO2. Based on their review of the scientific literature, the IPCC 6th assessment estimates that ocean fertilization could remove 1-3 Gt CO2 per year with cost estimates between $50 – $500 at full development. However, both sources caution ocean fertilization could result in unintended ecological consequences, and the durability of that removal is measured in decades or centuries instead of millennia. Proponents have put forward the concept of a “centennial tonne”5 to measure expected durability. However, other forms of mCDR like ocean alkalinity enhancement would provide more durable storage, and could have positive environmental spillovers, such as alleviating ocean acidification, another ecological problem caused by greenhouse gas emissions. It is still early days for most mCDR approaches, although there are some small-scale field trials by companies, such as Planetary’s ocean alkalinity enhancement methods and Project Vesta’s use of volcanic mineral on beaches to increase alkalinity of seawater.

Bioenergy carbon capture and storage (BECCS)

BECCS involves growing plants (which removes CO2 from the atmosphere), burning the plants for energy (which releases the carbon again), then capturing the gas and sequestering it. Thus, it very strongly resembles conventional CCS, but is counted as CDR since the plants being burned were planted intentionally to capture carbon. In theory, BECCS represents negative-emissions energy. BECCS plays a prominent role in the IPCC’s Integrated Assessment Models (IAM), meaning that modelers assume BECCS will play a prominent role in reducing greenhouse gas emissions. Investments in BECCS have increased recently, although few commercial BECCS facilities exist. For example, British power company Drax plans to invest $12.5 billion in U.S. BECCS power generation plants. The IPCC’s 6th assessment estimates that BECCS could remove 0.5 to 11 Gt CO2 per year at a cost of $15 to $400 per ton of CO2 at full deployment. While BECCS could play an important role, like most CDR strategies, it requires targeted subsidies or other financial incentives. BECCS stands out among removal strategies because it simultaneously produces energy and removes existing CO2 from the atmosphere.

Direct air capture (DAC)

DAC involves capture of CO2 directly from the atmosphere, rather than at a point source. When paired with carbon storage strategies, this approach is called direct air capture and carbon sequestration (DACCS). The IPCC’s 6th assessment estimates that DAC could remove 5-40 Gt—at the upper end of this range, equivalent to more than the world’s total annual CO2 emissions of 37.6 Gt in 2024—of CO2 per year at a cost of between $100-$300 per ton of CO2, at full development, generally more expensive than other methods. Compared to CCS, DAC is more resource-intensive and difficult because CO2 is much less concentrated in the atmosphere when compared to point sources like the smokestack of a thermal power plant. Frequently, DAC methods require lots of power, which could offset the climate benefit if not generated from clean sources. Notwithstanding these challenges, the total mitigation potential of DAC is among the largest, as there are few physical or natural limitations to the amount of CO2 that could be pulled from the atmosphere. DAC facilities can also be located anywhere, instead of co-located at a point source. This could save transmission costs for the CO2 because they could be located over optimal reservoirs for storage. However, DAC faces economic constraints, which means that DAC could be an attractive option if technological advancements significantly reduce its cost. In 2023, Heirloom Carbon Technologies launched the first commercial plant in the U.S. to use DAC, with Microsoft being the main customer paying for this carbon removal.6 The company sequesters this carbon underground, which would make this an example of DACCS.

What policies help remove CO2 from the atmosphere? What is the US doing about CDR?

Removing enough CO2 from the atmosphere in a cost-efficient manner will require strong government intervention and private sector innovation. Both public and private resources will play a role in researching and developing these technologies and bringing them to commercial scale. In general, direct government financing plays a more important role earlier in the innovation cycle for basic scientific research, R&D and demonstration projects. However, as the technologies mature, private sector innovations and competition can more effectively bring down costs and drive efficiencies. In any case, the government can provide sufficient incentives for private firms to drive these efficiencies and innovations. Specifically, the government can pay private firms directly to remove CO2 through subsidies, put a price on carbon and allow carbon credits to count towards compliance markets (for example, through a carbon tax or a cap-and-trade program that accepts carbon credits), or facilitate voluntary carbon markets. To ensure trust in carbon markets and public policies, the government can also facilitate the monitoring, reporting, and verification of CO2 removal. Additionally, governments can help tackle ancillary challenges to scaling up CO2 removal, namely, removing permitting hurdles while protecting local communities from externalities. Thus, the principal policy challenges for CDR include:

- Funding research, development and demonstrations

- Carbon pricing

- Incentivizing deployment

- Permitting for CDR facilities and infrastructure and securing local buy-in

- Measuring, reporting, and verifying removed CO2

Funding research, development, and demonstrations

The federal government funded CDR research through various initiatives. For example, the Carbon Negative Shot project administered by the DOE funded research into a diverse array of CDR approaches with the goal of capturing gigatons of CO2 for a cost of under $100/metric ton of CO2. The project aimed to achieve this goal by catalyzing both incremental and disruptive CDR technological improvements. Government funding can play a key role in CDR research, as the profit motives of private sector firms can lead to underfunding of early-stage research, relative to the benefits of research for society. This leads to a collective action problem where no individual firm wants to bear the cost of research despite potentially large societal benefits.

The 2021 Infrastructure Investment and Jobs Act (IIJA) goes beyond funding for basic research, as it invests $3.5 billion in Regional Direct Air Capture Hubs to support large-scale DAC and sequestration projects. These regional hubs were designed to allow firms to benefit from shared infrastructure, information spillovers, and technical expertise, thereby reducing costs and accelerating learning-by-doing in an emerging industry. Demonstration projects of this kind are particularly useful for early-stage technologies as they help establish technical feasibility at commercial scales that private investors are unlikely to finance given high technological uncertainty and policy-dependent revenue streams.

However, under the second Trump administration beginning in 2025, federal support for CDR and clean energy innovation was substantially reduced. The administration cancelled or terminated significant portions of previously authorized funding for Regional DAC Hubs, including multiple demonstration projects that had been selected under the IIJA framework. These cuts were part of a broader rollback of federal research and development funding, affecting not only DAC but also a wider set of climate and energy innovation programs.

While government-funded demonstration projects can help prove technical viability, they are unlikely on their own to bring CDR technologies to commercial scale. Long-term deployment will require stable and credible policy incentives that attract sustained private capital. When funding research or demonstration projects, policymakers should consider focusing on technologies in early stages of development. Depending on the maturity of the technology, these policies can include research grants, technology prizes, and demonstration project grants. While applicants should be evaluated on the merit, these policies should not be overly prescriptive in favoring certain technologies over others, as it is difficult to predict innovations before they occur.

Carbon pricing

Compliance markets and carbon pricing for CDR credits are considered an effective policy tool for incentivizing CDR. Compliance markets typically involve a broader economy-wide carbon price either by setting a cap on the total allowable emissions in the economy (or portions of the economy) allowing firms to trade emission allowances (cap-and-trade), or by taxing CO2 emissions (carbon tax). In the context of a cap-and-trade program, verified captured carbon would receive a tradable credit that could be bought and sold in the same way as emission allowances. Firms could use these CDR credits to cover their own emissions or sell them to other firms. In the context of a carbon price, verified captured carbon could receive a tradable credit that allows firms to offset their emissions and lower their carbon tax liability. An advantage of the compliance-market approach is that it combines emission reductions and CDR incentives into one coherent policy framework. It ensures economy-wide net-emission reductions while allowing individual firms to choose how to reduce their net emissions and by how much. The market results in the “lowest-hanging-fruit” emission reductions to come first and the costliest reductions to come last, minimizing overall costs and maximizing efficiency. Another advantage is that it is technology-neutral, which means it allows for broad experimentation and unbiased innovation. Lastly, unlike the direct subsidy approach, compliance markets force polluters to pay for the cost of their pollution, promoting fairness.

It is generally the most efficient approach to apply the same carbon price to both emissions capture and removal, so firms only pay to remove a ton of CO2 once it becomes cheaper than cutting an equivalent ton of their own emissions. Putting this into practice is harder for removals than emissions capture, though—as one review notes—because regulators need to confirm that removed carbon actually stays out of the atmosphere for decades or centuries, and to guard against firms that sell removal credits today but fail to deliver later.

Unfortunately, carbon pricing and compliance markets have struggled to gain federal political support in the U.S. In the European Union, a global leader in carbon pricing, domestic CDR offset credits are now set to be included in their emission trading regime under the revised European Climate Law. Deliberations on the specifics of implementation remain ongoing.

Incentivizing deployment

Once research, development, and demonstrations have established the viability of a carbon removal or capture technology, the private sector requires incentives to scale up and deploy the technology. Policymakers can achieve this by directly subsidizing CO2 capture or removal, setting up compliance markets, or facilitating voluntary markets. While the U.S. has focused more on direct subsidies and voluntary markets, ultimately, compliance markets are likely necessary to adequately incentivize CO2 removal.

The IRA and IIJA bolstered direct subsidies for CCS and CDR. Notably, the IRA greatly expanded the 45Q tax credit which primarily incentivizes CCS, DAC, and BECCS technology. The One Big Beautiful Bill Act (OBBBA) expanded these credits further for projects that convert carbon into fuels, chemicals, or other products and projects that securely store CO2 in oil and gas fields. Companies deploying these technologies can claim a tax credit per metric ton of CO2, with the amount varying based on whether the CO2 is sequestered or utilized and whether certain labor requirements were met. Under the expanded credit, DAC investments can receive as much as $180 per ton of CO2 sequestered. The USDA also provides subsidies for afforestation, reforestation, and forest carbon management. While the incentives provided by these subsidies encourage adoption of these technologies, when it comes to CDR, they are not the most economical or efficient incentives. This is because, ultimately, taxpayers pay for these subsidies while polluting firms pay nothing for the costs of their pollution.

Voluntary carbon markets (VCMs) have gained some momentum in incentivizing development of CDR. These markets arise out of voluntary climate commitments made by companies, often stemming from investor and consumer preferences for firms with lower net-emissions. In VCMs, developers undertake projects to avoid emissions or remove CO2 from the atmosphere. Independent third parties verify the projects’ emissions benefits and certify a tradable credit for the entity undertaking the project. Companies looking to lower their net emissions can purchase these credits to offset their own emissions. Presently, credits generated from CDR projects represent a small but growing share of the market. The total value of VCMs in 2024 was around $535 million, down from its peak of $2.1 billion in 2021, reflecting, in part, concerns over fraudulent carbon projects. To function properly, like other markets, VCMs require government regulation to promote transparency and protect buyers and investors.

For a detailed analysis of the landscape and key policy challenges in voluntary carbon markets, see Broekhoff, Conley et al. (2026), Broekhoff, Patnaik et al. (2026), Shortell et al. (2026), and Delacote et al. (2026).

Monitoring, reporting, and verifying captured CO2

Monitoring, reporting, and verifying (MRV) that CO2 has been removed from the atmosphere is an integral component of any CDR policy framework or market for carbon credits. Credible MRV ensures trust and transparency in both compliance markets and voluntary carbon markets, vital to drive continued growth and innovation in CDR. MRV includes the processes of measuring and quantifying CO2 removal, reporting on those removals, and verifying via a third party the accuracy of the reported removals. This requires comprehensive written protocols and procedures. Typically, a firm taking on a CDR project registers their project with a standard-setting institution (e.g., ACR), submits a monitoring plan in accordance with guidelines set out by the institution, follows the institution’s quantification methodologies, reports the quantified removal, obtains verification of this reported removal quantity from an accredited third party verifier, and finally, receives carbon credits certified by the standard-setting institution.

The 2026 Carbon Dioxide Removal Report describes the progress and challenges in MRV including both methodological and governance issues. First, the tools, instruments, and protocols of MRV vary significantly across CDR methods with some further along than others. For example, MRV is most developed for forest projects, followed by BECCS. DAC MRV has shown recent progress, while marine-based carbon removal methods lag with minimal MRV development due to difficult methodological challenges. For MRV across carbon removal and capture methods, open questions remain regarding how to account for the durability of the storage method, uncertainty when quantifying removal amounts, and additionality issues.

While various entities are making progress on standardizing MRV, there is more work to be done. The IPCC’s 7th Assessment, set to release in 2027, will include guidance on MRV best practices. At COP29, countries agreed to MRV rules for the Paris Agreement’s carbon trading system, and at COP30 Brazil proposed a voluntary coalition of countries for integrating carbon market initiatives. The Integrity Council for the Voluntary Carbon Market and the Voluntary Carbon Markets Integrity Initiative are both making progress on MRV for voluntary carbon markets. Notably, the EU plans to integrate CDR credits into its emissions trading scheme and is thus making progress on a framework that will cover MRV issues. In the U.S., the Department of Energy funded research into CDR which includes MRV-related problems, including for mCDR.

Gaining local acceptance and permitting for CDR facilities and infrastructure

To be successful, carbon removal and capture initiatives must overcome longstanding local acceptance and permitting challenges that hinder new infrastructure projects. These challenges are particularly pertinent to the construction of CO2 pipelines and CO2 storage sites. Pipelines almost inevitably pass through land owned by interests and communities unfamiliar with and potentially hostile to such projects, often requiring local jurisdictions to grant permits for these projects. Beyond the local level, federal and state permitting also inhibits construction of new infrastructure and warrants reform. In short, permitting for CO2 pipelines varies by state, but is generally quite difficult. Without reform, CO2 pipeline permitting will continue to pose a bottleneck for CDR. When it comes to sequestering carbon, the EPA has primary authority to permit drilling and wells, though the EPA often cedes this authority to states. The EPA often takes longer to permit drilling compared to some states, which poses another potential bottleneck. Policymakers at the state and federal level will need to grapple with these permitting issues to achieve the full potential of carbon removal and capture.

Conclusion

Carbon dioxide removal and capture would be an essential part of addressing climate change if the costs could be lowered to the $50-100 range. This will likely require substantial added R&D, which could be incentivized through a significant carbon price or R&D subsidies to encourage deployment, so that learning curve benefits and economies of scale can be fully realized. Policymakers have taken concrete steps to make CDR a more prominent part of the U.S. climate response, and investments and research are starting to follow. However, CDR takes many forms, and it is unclear which approaches can scale up and at what cost. Despite uncertainties about the underlying technologies and economics of carbon removal, leaders continue to craft policies that will stimulate further investments and inquiry. In other words, carbon removal is a dynamic issue where science, policy, and economics intertwine to address one of the world’s most challenging problems. The scale of the challenge is such that this interdisciplinary tangle is likely to remain a feature of this space for quite some time.

Related Content

Authors

-

Appendix: List of acronyms and abbreviations

BECCS

Bioenergy carbon capture and storage

CCS

Carbon capture and storage

CCU

Carbon capture and utilization

CDR

Carbon dioxide removal

CFTC

Commodity Futures Trading Commission

CO2

Carbon dioxide

DAC

Direct air capture

DACCS

Direct air capture and carbon sequestration

DCM

Designated contract market

IEA

International Energy Agency

IIJA

Infrastructure Investment and Jobs Act

IPCC

Intergovernmental Panel on Climate Change

IRA

Inflation Reduction Act

mCDR

Marine carbon dioxide removal

MRV

Monitoring, reporting, and verifying

VCM

Voluntary carbon market

-

Footnotes

- “Carbon capture and sequestration” is often used interchangeably with “carbon capture and storage”

- For reference, U.S. CO2 emissions totaled approximately 4.5 Gt in 2024.

- “Green hydrogen” refers to hydrogen produced via electrolysis of water using electricity generated from zero-carbon energy sources, such as renewables. Because it produces no direct carbon emissions, it can serve as a clean fuel. It is different from “blue hydrogen,” which is produced from natural gas with carbon capture and storage.

- One out of these 13 facilities is a Direct Air Capture (DAC) facility, which we define in a later section.

- “A centennial tonne is defined as 1000 kg of carbon isolated from atmospheric ventilation for at least 100 years.”

- In April 2026, Microsoft reportedly halted all purchases on new carbon removal credit purchases. However, in May 2026, Microsoft announced that they will purchase 650,000 metric tons of removals over seven years from Denmark-based biogas producer BioCirc, signaling that its carbon removal program had not ended, though the scale and pace of future purchasing remains uncertain.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

What is carbon dioxide removal and capture in the context of climate change?

July 14, 2026