The paper summarized here is part of the Fall 2023 edition of the Brookings Papers on Economic Activity (BPEA), the leading conference series and journal in economics for timely, cutting-edge research about real-world policy issues. The conference draft of this paper was presented at the Fall 2023 BPEA Conference (recordings and slides are available via the link). The final version was published in the Fall 2023 issue by Johns Hopkins University Press. Submit a proposal to present at a future BPEA conference here.

Download final paper with online appendix, discussion comments, and general discussion summary

Supply constraints as the economy exited the COVID-19 pandemic caused price inflation to surge while wages picked up only gradually. But now that inflation has started to fall, wages can increase faster than inflation, for a time, without producing a wage-price spiral that overheats the economy, suggests a paper discussed at the Brookings Papers on Economic Activity (BPEA) conference on September 29.

In the paper, “Wage-Price Spirals,” the authors—Guido Lorenzoni of the University of Chicago and Iván Werning of the Massachusetts Institute of Technology—modeled the effects of different demand and supply shocks on wages and prices. Their results explain why constraints in the supply of non-labor market inputs, as the economy exited the pandemic, caused inflation to surge and real (inflation-adjusted) wages to decline, leaving room for real wages to bounce back later.

They used a variation of the standard New Keynesian model, which accounts for stickiness (slowness to adjust) in both wages and prices. But, in contrast with the simplest textbook models, their model accounts for the effect of non-labor inputs into prices, such as increased demand for home goods and construction materials and decreased supplies of microchips and lumber during the pandemic.

During episodes of excess demand, the prices of scarce non-labor inputs initially spike, fueling an increase in price inflation. Price inflation eventually subsides, allowing an increase in real wages. In effect, wages fall behind inflation initially and then catch up.

The implication of the paper is that the wage gains that followed the surge in prices during the pandemic need not inevitably lead to wages and prices spiraling out of control. That, in turn, suggests that, rather than engineer a recession in response to an inflation surge in similar circumstances, central banks can aim for a so-called soft landing (slower but continued growth) to bring inflation down.

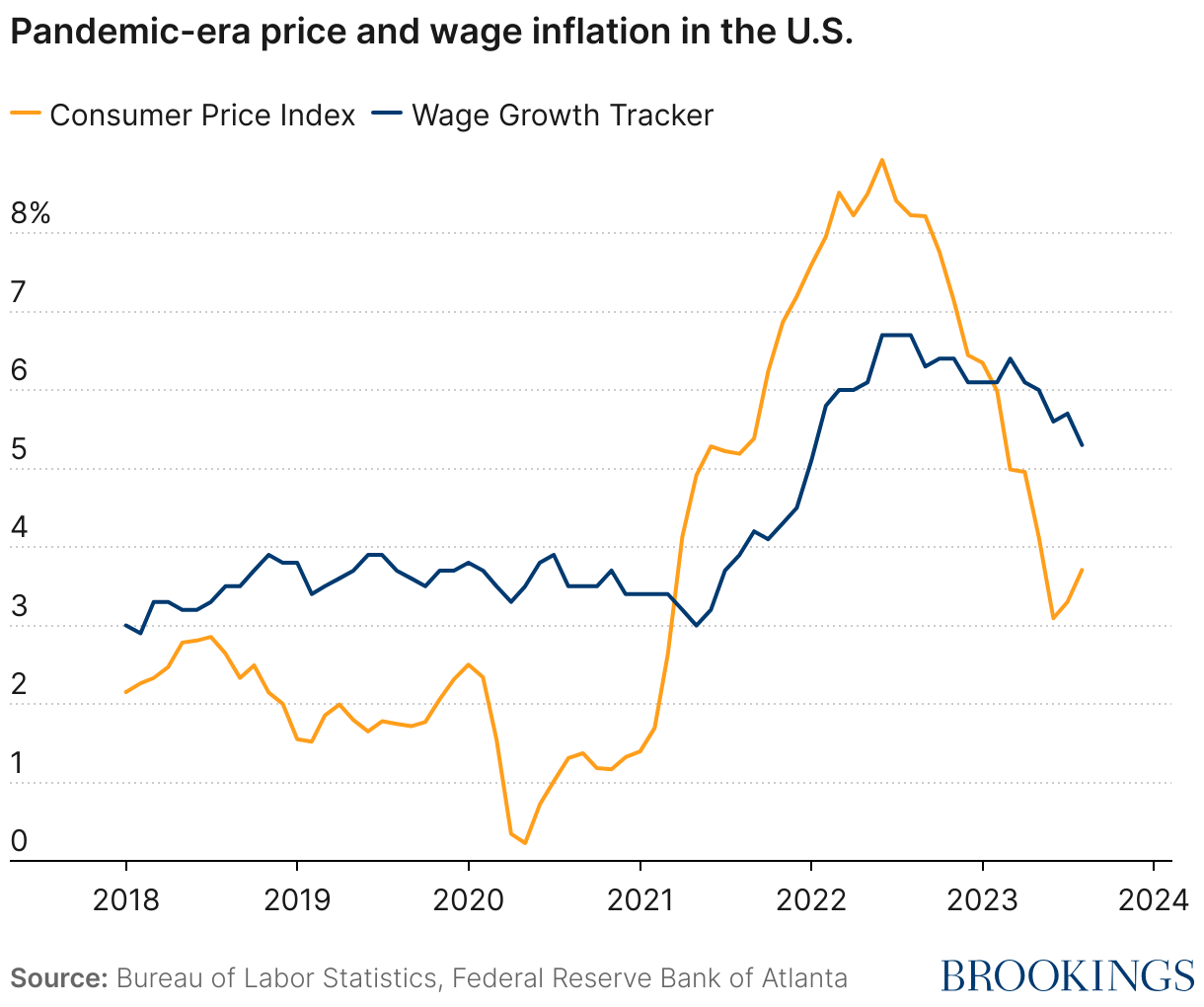

The modeling results mirror the U.S. experience of the past two years. Annual inflation, as measured by the Labor Department’s consumer price index, peaked at a 40-year high of 9.1% last summer but retreated to 3.7% by this August. Meanwhile, average hourly wages in August were up 4.3% from a year earlier—a gain in inflation-adjusted terms.

As price inflation accelerated last year, the Federal Reserve began attacking it by rapidly raising short-term interest rates from near zero to reduce demand. As inflation receded this year, it slowed the pace of rate increases and will consider later this year whether to further increase its short-term rate target from a 22-year high and how long to keep rates high.

“People were worrying that we were going back to the 1970s. But this paper gives you pause about overreacting,” Werning said in an interview with The Brookings Institution. “Recently, as price inflation came down, wage inflation started to be the bad news. But it doesn’t have to be bad news. There is a feedback effect but that doesn’t imply things get out of control.”

CITATION

Lorenzoni, Guido and Iván Werning. 2023. “Wage-Price Spirals.” Brookings Papers on Economic Activity, Fall. 317-367.

Galí, Jordi. 2023. “Comment on ‘Wage-Price Spirals’.” Brookings Papers on Economic Activity, Fall. 368-381.

Şahin, Ayşegül . 2023. “Comment on ‘Wage-Price Spirals’.” Brookings Papers on Economic Activity, Fall. 392-389.

Authors

Authors

Discussants

-

Acknowledgements and disclosures

Guido Lorenzoni is a consultant for the Federal Reserve Bank of Chicago. The authors did not receive financial support from any firm or person for this article or, other than the aforementioned, from any firm or person with a financial or political interest in this article. The authors are not currently an officer, director, or board member of any organization with a financial or political interest in this article.

David Skidmore authored the summary language for this paper. Chris Miller assisted with data visualization.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).