This article was updated on May 22, 2023 to clarify that the Republic of Congo, not DRC, uses the CFA franc.

DRC has better growth and fiscal prospects than regional peers…

Following a slowdown in real GDP growth induced by the COVID-19 pandemic, the Democratic Republic of Congo (DRC) posted a robust rebound (6.2 percent) in 2021. According to recent IMF forecasts, economic growth remained above 6 percent in 2022, with GDP growth projected to reach 6.3 percent in 2023. DRC’s growth will thus remain above the average for sub-Saharan Africa (SSA), driven by the extractives sector and improved utilization of other natural resources. The country’s overall public and publicly-guaranteed debt is also relatively low—at 24 percent of debt-to-GDP as at the end of 2022, it is less than half of the SSA average with only moderate risk of debt distress. High political and security risks, however, continue to dampen economic prospects and underscore the importance of governance reforms.

… But like most African sovereigns, DRC is caught in a low ratings trap

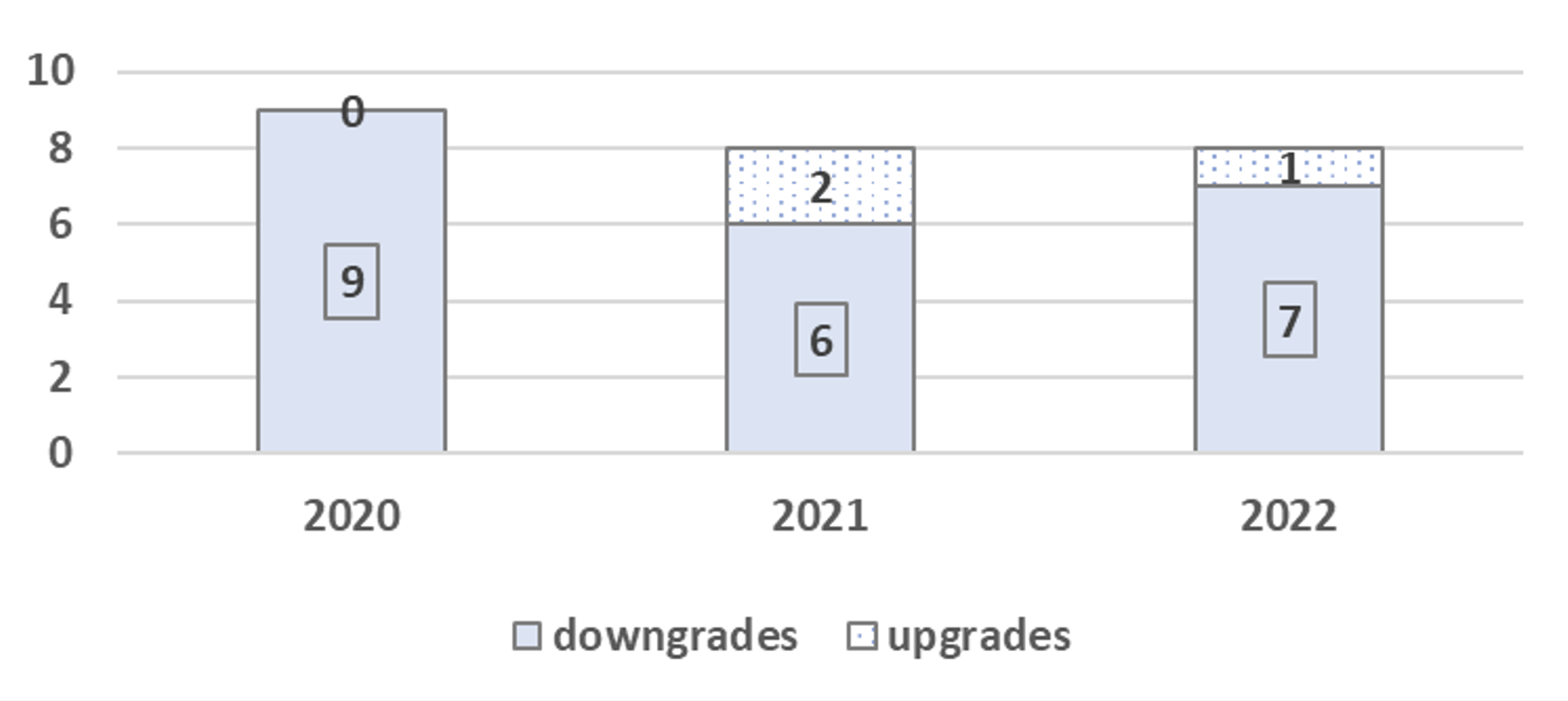

In November 2022, Moody’s Investors Service (Moody’s) upgraded DRC’s long-term local and foreign currency sovereign ratings to B3 (a high credit risk) from Caa1 (a very high credit risk). While the move is positive for the DRC, it was the only upgrade to sovereign ratings (versus seven downgrades) that the rating agency granted in Africa during 2022, and one of only three upgrades during the last three years (Figure 1).

Furthermore, in January 2023, Moody’s downgraded Nigeria to Caa1 from B3, compounding the negative trend in the region’s credit risk assessments. As such, the general outlook for SSA’s sovereign ratings in 2023 remains precarious, reflecting rising fiscal, liquidity, and social risks amplified by the adverse effects of the Russia-Ukraine war and the tightening of global financial markets.

Figure 1. Moody’s changes in rating levels in Africa, 2020 – 2022

Source: Authors’ calculations based on the Moody’s Investors Service data.

Note: Excludes North African countries (Egypt, Morocco, Tunisia).

Since credit ratings are path-dependent, abrupt downgrades in Africa’s ratings can have long-term implications regarding limits to rating improvements. Over the past decade, the speed of rating adjustments in Africa (and frontier markets in general) has been asymmetric—with unexpected, procyclical, and multiple downgrades but slow and gradual upward climbs.

More specifically, while upgrades occur only after the sovereign has been on a positive outlook for some time, downgrades do not necessarily follow negative outlooks. For example, it took Senegal six years to be upgraded one notch, from B1 to Ba3. In contrast, the Republic of Congo’s (Congo Brazzaville) three-notch downgrade in 2015/2016 occurred within less than one year: from Ba3 with stable outlook in October 2015, to B3 by August 2016 with further review for downgrade, putting into question the country’s ratings stability and long-term horizon. Zambia’s downgrades in April 2016 and May 2019 occurred without signaling, from stable outlooks.

Overinflated risk ratings reflect credit rating agencies’ limited recognition of Africa’s unique idiosyncrasies, such as: its green mineral endowments, the lack of relevant data (e.g., on contingent liabilities or public sector debt), and heightened risk perceptions reinforced by negative narratives of mainstream media. These factors, which play a disproportionate role in unsolicited ratings, can put African governments into the “low ratings, high borrowing cost” trap described by Hippolyte Fofack.

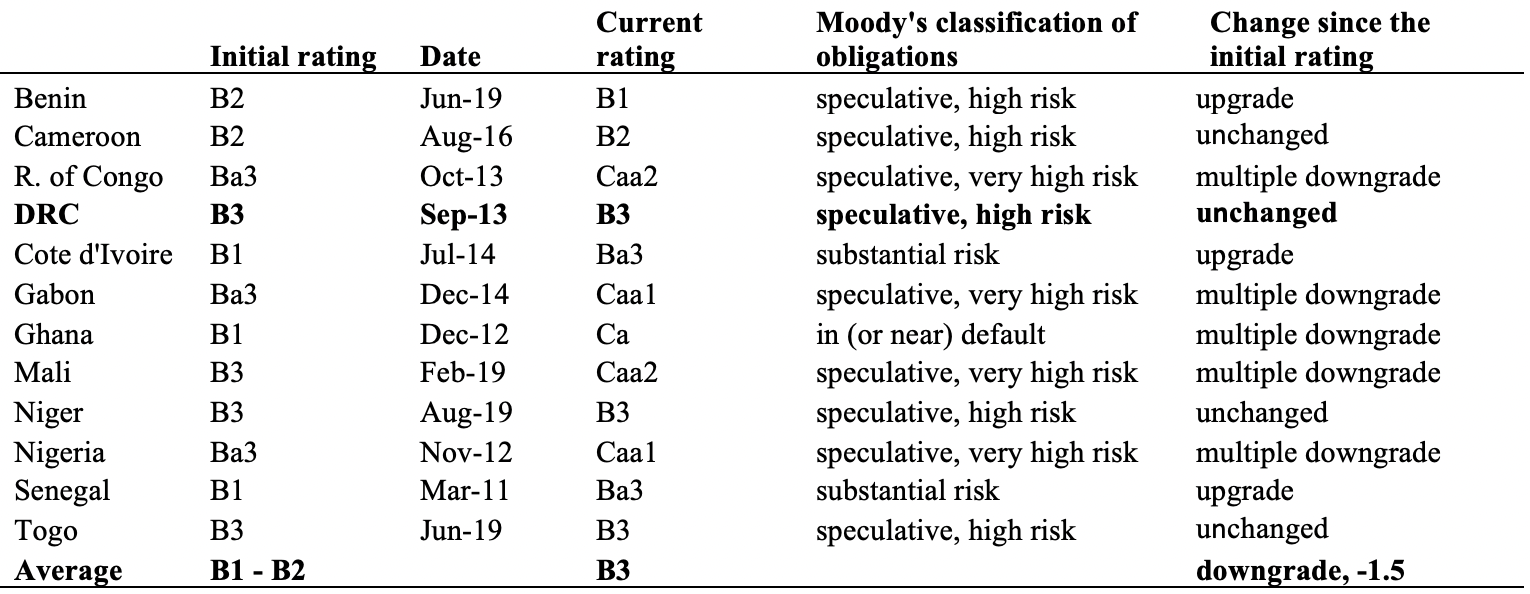

In similar fashion to DRC, views on credit risks associated with long-term, fixed-income obligations of other sovereigns in Central and West Africa are also bleak. They are on average rated between B2 and B3 (i.e., speculative and high credit risk). Barring recent upgrades for Benin, Cote d’Ivoire, and Senegal, the average sovereign rating for Central and West Africa fell during the post-COVID period by more than one notch in most countries. Moreover, in the majority of the cases, the change entailed multiple downgrades—to very high/nearing default credit risk (Table 1).

Table 1. Rating levels and changes for sovereigns in Central and West Africa

Source: Authors, based on the Moody’s Investors Service data.

Sovereign ratings constrain ratings of other entities

Sovereign ratings have a systemic effect on countries’ domestic capital markets because these ratings typically serve as a ceiling for credit ratings of most other rated entities such as municipalities, banks, or corporations. Indeed, sovereign rating downgrades have significant adverse effects on ratings of private companies and financial market institutions, even if there is no fundamental change in the creditworthiness of these entities. The fall in bond prices and downgrade of nine banks in Nigeria, following the sovereign’s downgrade, illustrate this point.

Given DRC’s relatively low and volatile domestic savings rates, access to foreign financing at a reasonable cost is critical for the country’s social and economic development.

DRC still faces a steep path to investment grade

As a result of the latest rating assessments by Moody’s (and the S&P which in January 2022 upgraded DRC’s credit rating from CCC+ to B-, an identical rating to Moody’s B3), the country is bound to benefit from strengthened economic and fiscal prospects, as well as an improved external position, i.e., increased foreign exchange reserves and stabilized exchange rate.

While these factors could change suddenly should another major global or regional shock arrive, the drivers constraining upward movement of DRC’s ratings, are structural in nature and hence more long-term. For example, they include very low GDP per capita; weak (albeit improving) institutions; large infrastructure gaps; risk of social unrest and political instability; as well as continued conflict in eastern DRC. Against these hurdles, it appears that the DRC faces a steep and long climb to an investment grade rating or even a better non-investment grade rating; that is, at least a Ba rating as has been the case for Senegal and Cote d’Ivoire.

However, the broader and more pertinent question (which pertains to other SSA sovereigns), remains: To what extent has the DRC been set back by the negative initial assessments? The question is especially relevant since some of the country’s main strengths are not directly included in the rating methodologies, for example, its sizeable demographic dividend arising from its large, youthful, and rapidly growing population; a peaceful democratic transition (the first ever in the country’s history); increased competitiveness, as well as expectations of more diversified trade and economic growth following its admission as a member of the East African Community.

… but Eurobond issuance backed by natural resources and regional MDBs could ease the way

What can therefore be done to improve Africa’s, and in this case DRC’s, credit ratings? Especially over the short-term as many of the frequent recommendations (adjusting methodologies, regulating credit rating agencies, establishing independent data collection agency) would take time.

To reset the perception of DRC’s low creditworthiness in the near future, there is a strong case for the government to issue a pilot sovereign bond on international markets that would receive a good rating and establish a new benchmark. The enhanced rating could be achieved via securitization of the DRC’s existing or future assets (minerals, hydropower potential, arable land, and the second-largest rainforest in the world). However, the process would need to be transparent and linked to growth-enhancing projects to avoid pitfalls associated with resource-backed loans. In the past, these loans often went to countries with weak governance, suffered from the lack of competitive markets, and contributed to capital outflows.

DRC could also strive to have its Eurobond issuance backed by guarantee from a multilateral development bank (MDB). In this case, support from borrower-led MDBs is more likely because on the continent, these MDBs are governed by African countries with similar goals and views on their role in development. Conversely, lower credit ratings of such entities would limit the upgrades of any Eurobonds they may guarantee, and thus reduce effectiveness.

In the longer term, countries such as the Republic of Congo that share common currency (CFA franc) with the Central African Economic and Monetary Union (CEMAC) or West African Economic and Monetary Union (WAEMU) members, may wish to consider issuing joint regional Eurobonds. The EU has already embarked on such issuance, and African countries may start exploring this option and monitoring EU experiences with this endeavor. To succeed, such a move would require significant political will, including a regional debt management strategy, enhanced communication, agreements on future debt issuance and the use of the proceeds, as well as backing by joint guarantees. This option would also support regional integration of financial markets and hence implementation of the African Continental Free Trade Area (AfCFTA).

Related Content

2023

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Upgrade of DRC’s sovereign credit rating—One step forward, after one step back

May 11, 2023