This post discusses my monthly update of the Barnichon-Nekarda model. For an introduction to the basic concepts used in this post, read my introductory post (Full details are available here.)

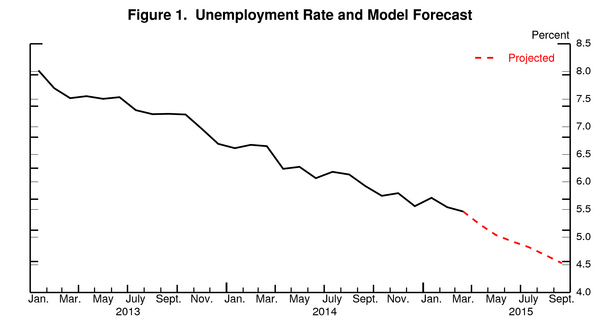

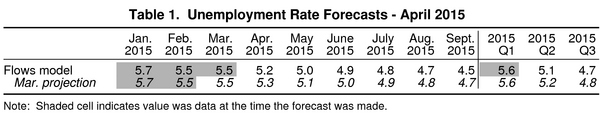

In March, the unemployment rate remained steady at 5.5%, as anticipated by the model. Going forward, the contour of the forecast is broadly unchanged with a fast decline in unemployment over the next 6 months. In fact, the model anticipates a large drop in unemployment in April, with a jobless rate at 5.2 percent (so a 0.3 percentage point drop), going down to reach 4.5% by September 2015.

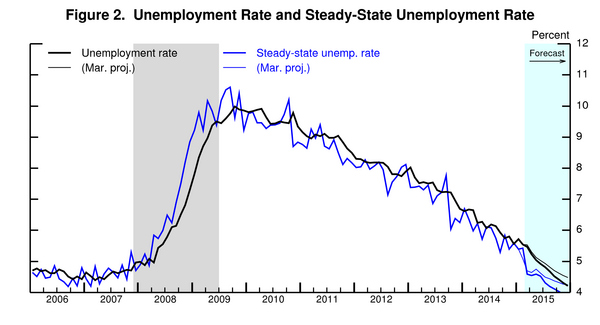

This upbeat model’s forecast can be easily understood by looking at the projected behavior of the “steady-state” unemployment rate. The steady-state unemployment rate, the rate of unemployment implied by the underlying labor force flows—the blue line in figure 2— stands currently at 4.6%, almost a full percentage point lower than the actual unemployment rate. Our research shows that the actual unemployment rate converges toward this steady state. With a steady-state unemployment rate so much lower than the actual rate (in fact steady-state unemployment has never been so far from the actual rate in the 3 years since the beginning of this blog[1]), this “steady-state convergence dynamic” will push the unemployment rate down very strongly, implying a fast decline in unemployment going forward.

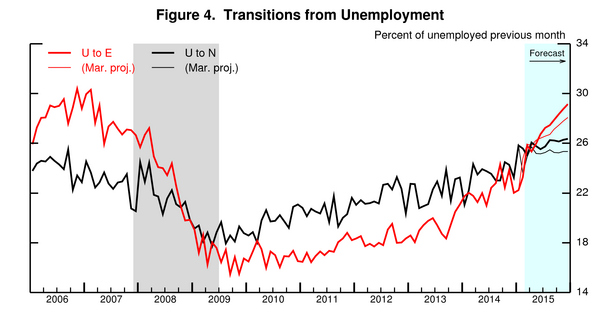

To forecast the behavior of steady-state unemployment, the model propagates forward its best estimate of how the flows in and out of unemployment will evolve over time. Following months of good news on the job openings front, the model anticipates strong growth in the job finding rate (U-E) over the next few months (figure 4), which will push down the steady-state unemployment rate, and will lead to a strong decline in the unemployment rate strongly over the next 6 months.

Interestingly, for the first time in the past 3 years, the model anticipates the job finding rate (U-E) to return to its pre-crisis level within the forecast horizon (figure 4), which would then mark the end of the decline in unemployment.

To read more about the underlying model and the evidence that it outperforms other unemployment rate forecasts, see Barnichon and Nekarda (2012).

[1] An exception is the government shutdown in the Fall of 2013, but there are many reasons to believe that the flow data were severely affected by the shutdown and thus did not accurately reflect the state of the labor market.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Unemployment to drop to 5.2% in April, to reach 4.5% by September

May 5, 2015