In 2022, Congress reintroduced a corporate alternative minimum tax (CAMT) as part of the Inflation Reduction Act. The intent was clear: address the long-standing concern that large, profitable corporations often pay little to no federal taxes.

In a new research brief, I describe why the new CAMT is unlikely to resolve this tension.

Understanding how profitable corporations end up owing no taxes is key. These companies are generally not breaking the law. Rather, they are using the tax policy incentives that Congress itself designed. The incentives might, for example, promote growth or efficiency. But in the process, they might also eliminate most or all taxable income even for highly profitable companies.

In principle, the CAMT can be designed to ensure that profitable corporations pay at least some tax, even if various deductions and credits would otherwise reduce their tax liability excessively. A CAMT requires companies to calculate their taxes using alternative measures of earnings. If the tax that they owe using this measure is higher than under the regular corporate tax rules, they pay the difference as an AMT.

In practice, the devil is in the details. Two features, in particular, reduce the revenue-raising potential of the CAMT (and were present in the old AMT that existed from 1986 to 2017 as well as in the current tax). First, several provisions that reduce tax liability for profitable companies in the regular corporate tax also reduce the tax base in the CAMT:

- Accelerated depreciation reduces the cost of investment by allowing businesses to deduct the cost of these investments more quickly.

- Credit for research and development encourages innovation by providing a tax subsidy to offset the cost of developing new products or technologies.

- Net operating loss deduction smooths temporary fluctuations in income by ensuring that businesses are taxed on their average profitability over time.

- Foreign tax credit prevents the double-taxation of multinational corporations for income that is earned abroad.

Second, companies that pay CAMT can use these payments as credits against future tax bills.

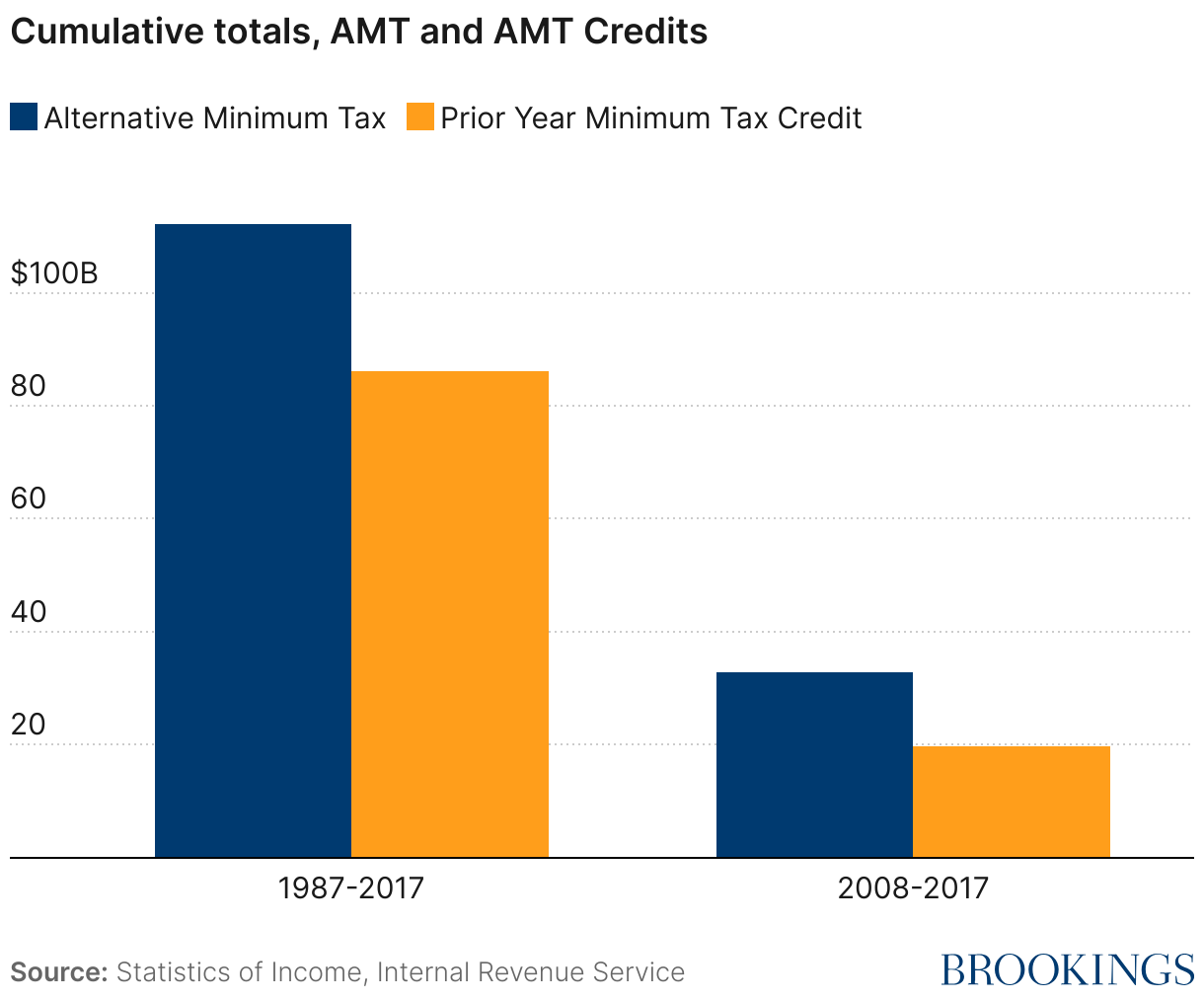

As shown in Figure 1, the old CAMT raised a net total of $26.08 billion in revenue from 1987 to 2017 after accounting for AMT credits, with $13.19 billion of that amount collected in the decade before the AMT was repealed. In fact, the credit reduced baseline AMT revenue by 40% during this final decade. New research suggests that a similar revenue loss could occur with the new CAMT. This raises questions about how much revenue the new CAMT will actually generate. While the Joint Committee on Taxation (JCT) estimated that the new CAMT would raise $222 billion in the first ten years, this projection is nearly 20 times higher than the net revenue raised by the old CAMT, and both policies share many of the same design features.

Finally, the new CAMT ties tax liability to a measure of earnings that is largely based on book income, introducing its own set of complexities. Book income follows accounting rules and provides an accurate representation of a firm’s financial health to shareholders, investors, and creditors, while tax income aims to inform the tax authorities about the tax liability of a company. Research shows that efforts to induce book-tax conformity, like the new CAMT, can lead to the degradation in the information quality of financial statement income with little effect on underlying taxes paid.

The new corporate AMT was introduced to address the public concern that large corporations sometimes pay no federal taxes, even when they report profit on financial statements. While CAMT policies aim to ensure that these corporations contribute something, they have not fixed the underlying reasons why companies pay so little in the first place. Until policymakers take a hard look at the tax code itself—particularly the deductions and credits that lower corporate tax liabilities—the problem is likely to persist. While the CAMT may raise some revenue, it’s far from a comprehensive solution to corporate tax avoidance.

Related Content

Author

-

Acknowledgements and disclosures

The Brookings Institution is financed through the support of a diverse array of foundations, corporations, governments, individuals, as well as an endowment. A list of donors can be found in our annual reports published online here. The findings, interpretations, and conclusions in this report are solely those of its author(s) and are not influenced by any donation.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

The limits of the new corporate AMT: Why little has changed

November 13, 2024