Introduction

There is a long-standing concern that some large, profitable companies pay little to no federal taxes. According to a 2021 report by the Institute on the Taxation and Economic Policy, 55 of the largest corporations in the U.S. paid no federal income tax in 2020 despite reporting substantial pre-tax profit. In response, in 2022 Congress created a corporate alternative minimum tax (CAMT) to address these disparities.

These concerns, however, are not new. For example, in its 1985 report, “Corporate Taxpayers & Corporate Tax Freeloaders,” Citizens for Tax Justice found that 50 of 275 “highly profitable” companies paid no federal income tax between 1981 and 1984, including Boeing Co., which the report noted earned more than $2 billion in profits over this time period but generated tax refunds totaling $285 million. Results like these led to the expansion of an earlier corporate AMT in the Tax Reform Act of 1986, which lasted until it was repealed in the Tax Cut and Jobs Act of 2017 (TCJA).

The fact that profitable companies sometimes pay no taxes raises fundamental questions about the fairness of the corporate tax system and may raise concerns about potential misconduct. The truth, however, is quite different. Instead, this issue arises from key differences between a corporation’s taxable income, which determines its current tax bill, and its “book” income, which reflects on-going profitability for investors, creditors, and other stakeholders. As discussed below, these measures capture different concepts, and differences are shaped by congressional choices to reduce taxable income to encourage certain business activities. As a result, profitable corporations—those with high book income—often legitimately have low or no taxable income.

As I show in this brief, CAMTs can be designed to ensure that all corporations pay at least a baseline level tax, regardless of any deductions, credits, and deferrals that might otherwise reduce taxes to zero or even below. At the same time, it is important to take a step back and recognize why corporations, whether from time to time or on a persistent basis, can end up in a position where they do not owe federal taxes even if they are completely playing by the rules.1 Low corporate tax liability is a policy choice of the U.S. corporate tax code—a consequence of corporate tax deductions and credits that are designed, for example, to incentivize investment or increase employment. This brief examines the intended role of the AMT in corporate tax policy and its effectiveness in ensuring tax fairness, while also identifying its limitations and potential areas for reform.

The purpose and history of the corporate AMT

While a minimum tax on business income was first introduced in 1969, the modern corporate AMT was provisioned by the Tax Reform Act of 1986. The express purpose was “to ensure that no taxpayer with substantial economic income can avoid significant tax liability by using exclusions, deductions, and credits,” (Joint Committee on Taxation 1987). In other words, the corporate AMT was intended to prevent companies from using so many deductions, credits, and deferrals, which are sometimes collectively referred to as tax loopholes or tax breaks, to reduce their taxes to zero or even create negative tax liability while otherwise generating income. The corporate AMT endured for the next thirty years until it was largely repealed2 as part of the TCJA. The corporate AMT was reinstated in 2022 under the Inflation Reduction Act (IRA) as a major source of revenue to offset the cost of the green energy provisions. As will be explained shortly, the design of the IRA’s CAMT marked a departure from previous versions by targeting certain large corporations based on financial statement profit as opposed to measures of taxable income.

Related Content

Measuring corporate earnings: Taxable income vs. book income

Measuring taxable income

Taxable income, defined by the Internal Revenue Code (IRC) and regulated by the Internal Revenue Service (IRS), is generally determined by gross income less all allowable deductions. Corporations earn gross income from a variety of sources including the sale of goods and services, rents, royalties, most interest income, gains generated by the sale of assets, and foreign operations. Expenses can be deducted from gross income in one of two ways. Certain expenses are deducted in the same year that they occur—for example, wages and salaries, material costs, or interests paid. Other expenses are deducted over several years, following the relevant depreciation or amortization schedule. These expenses are often associated with the purchase or development of assets that will produce income over several years—for example, the purchase of durable inputs or research and development expenses.

A corporation’s tax liability is determined by the corporate tax rate, its taxable income, and any tax credits a firm may have earned:

Tax Liability = Corporate Tax Rate × (Gross Income – Deductions) – Tax Credits

The TCJA introduced a 21% corporate tax rate, reduced from a top marginal rate of 35% that had been in place for decades. A firm’s Effective Tax Rate (ETR) is measured as the ratio of tax liability to a pre-tax measure of profit.3 ETRs that fall below 21% have raised questions about whether a firm is paying their “fair share.”

Firms can have low ETRs for several reasons. First, businesses naturally fluctuate between positive and negative profit throughout the business cycle. In loss years, no tax is owed. Instead, and as will be described later, the tax system permits businesses to carry these losses forward to reduce positive taxable income in the future; this deduction is called the net operating loss deduction (NOLD). The NOLD is an important design element of the corporate tax because it helps firms avoid big tax swings from year to year; instead, they are taxed based their average profitability over time. Second, certain business activity can generate large deductions or credits, such as a large capital expenditure or a substantial investment in research and development activities.

When certain tax rules affect how taxable income is calculated, the benefits are referred to as tax expenditures. More formally, tax expenditures measure the value of the tax deduction, tax credit, or other benefit by the foregone tax revenue that would have otherwise been collected. The Office of Tax Analysis and the Joint Committee on Taxation regularly updates the estimated value of most tax expenditures.

During the past few decades, the largest tax expenditures for corporations have included a credit for foreign income taxes paid; an accelerated deduction for the cost of acquiring equipment and machinery; a credit for increasing research activities; and a credit for the development of low-income housing. In the wake of the 2022 Inflation Reduction Act, large tax expenditures now also exist to support the production of clean energy. Each of these tax expenditures serves an important policy objective:

- Credit for foreign income taxes paid: The Foreign Tax Credit (FTC) prevents the double-taxation of multinational corporations for income that is earned abroad. This policy is a cornerstone of optimal multinational tax treatment.

- Accelerated depreciation for equipment and machinery: This deduction, sometimes referred to as bonus depreciation, incentivizes investment by allowing businesses to deduct the capital expense more quickly.

- Credit for research and development (R&D): This credit encourages innovation by providing a tax subsidy to offset the cost of developing new products or technologies.

- Credit for low-income housing development: This credit promotes the construction and rehabilitation of affordable housing to address long-running housing shortages for lower-income communities.

- Clean energy tax credits: These credits encourage investment in renewable energy sources.

Reports suggest that these tax expenditures help explain low tax liabilities over the last several decades. For example, between 2006 and 2018, more than two-thirds of corporations had no tax liability, although larger, profitable firms were more likely to owe taxes (Government Accountability Office 2016; 2022). These reports highlight several notable and large tax expenditures as related to low tax liabilities including NOLDs, accelerated depreciation, foreign tax credits, and large general business credits like the R&D credit. Notably absent from these reasons: tax evasion.

Measuring book income

While taxable income serves as the foundation for determining corporate tax liability, this is just one measure of earnings. A different measure, often referred to as book income, is designed to provide an accurate representation of a firm’s financial health to inform investors, creditors, and other stakeholders. Book income, which is reported on financial statements, is determined following a set of rules governed by Generally Accepted Accounting Principles (GAAP) and overseen by the Financial Accounting Standards Board (FASB). Generally, book income includes revenues when they are earned and records expenses when they occur, regardless of when cash is received as payment or paid as an expense. This accrual-based measure reflects a company’s operational performance over time.

Many reports that identify profitable corporations with low tax bills are based on an analysis that compares earnings and the tax expense using book income measures that are reported on financial statements. Research shows, however, that financial statement tax disclosures do not accurately reflect a firm’s tax liability or effective tax rate due to differences in the way that income is measured within complex multinational structures across GAAP and IRC rules and regulations (Hanlon 2003; Bokulic, Henry, and Plesko 2012). For this reason, it’s important to exercise caution when drawing conclusions based solely on financial statement income.

Differences between taxable income and book income can reconcile the disconnect that sometimes occurs between the profits companies report to shareholders and the taxes they pay. These book-tax differences can be temporary or permanent. Temporary differences arise when expenses are recognized in different periods across book and taxable income. Importantly, temporary differences will eventually reverse over time. On the other hand, permanent differences occur when certain income or deductions affect financial income but are never included in taxable income or vice versa. Permanent differences lead to lasting disparities between book and tax income.

The treatment of expenses incurred to purchase equipment is one prominent example of book-tax differences. Suppose a company purchased a piece of machinery with a useful life of 10 years for $1 million. Under book income (and following GAAP rules), the company would typically depreciate the cost of this equipment over its useful life, reporting a $100,000 expense in each year over the next ten years on its financial statements. Under the IRC, the company may be permitted to report more of this expense sooner during the life of the asset. For example, under a tax policy of 100% bonus depreciation, the company would be permitted to deduct the entire cost of the purchase in the year it was made. This means that the company would have a taxable income in the year of the purchase that was substantially smaller than book income. By allowing businesses to recover their investment costs more quickly, policies like bonus depreciation aim to make purchasing new assets more attractive, effectively reducing the “user cost of capital”—or, in simpler terms, making it cheaper and easier for companies to invest in growth.

The treatment of negative profit is another area where book-tax differences can diverge significantly. Suppose a company experiences a large economic loss in one year, causing earnings to be negative. Following book accounting rules, the company would report negative earnings in the year that they occurred. However, following the IRC, the company would report zero taxable income this year and would be permitted to report the negative earnings as an NOLD, reducing future positive earnings.4 Consider a company that had a $500,000 loss in 2023 and earned $2 million in 2024. In 2024, this company would be permitted to reduce its taxable income by $500,000. This differs from book income, where losses and profits are reported in the years they occur, without the ability to shift income across periods.

Another example of a book-tax difference is the way certain tax-exempt investments are treated. For example, corporations that invest in municipal bonds do not pay tax on the interest income that they receive from this investment. The tax exemption on municipal debt encourages investment in public infrastructure and community development projects, supporting essential services like schools, hospitals, and roads. However, for financial reporting purposes, this interest is recorded as income when measuring book income. This creates a permanent book-tax difference, as the income from municipal bonds will never be subject to corporate taxes. Unlike temporary differences, which eventually reverse themselves (as with accelerated depreciation or NOLDs), permanent differences like those that arise from investments in tax-exempt municipal bonds lead to a lasting gap between book and tax income.

Both temporary and permanent book-tax differences can create situations where seemingly profitable companies based on an examination of financial statement income can owe little to no tax, underscoring the rationale for policies like a corporate AMT.

How the AMT works: Mechanism and design

Core AMT mechanism

The AMT requires taxpayers to calculate their tax liability multiple times. First, corporations calculate their tax liability under the normal rules and regulations governed by the IRC, as previously described. Then, corporations must calculate their tax liability using a different tax rate and a different set of rules that adjust what is included as income, which deductions are allowable, and which tax credits are allowable. This alternative calculation yields their tentative alternative minimum tax liability. Corporations pay whichever of these liabilities is larger.

Pre-TCJA CAMT

Prior to its 2018 repeal under the 2017 TCJA, corporations were required to calculate their tentative alternative minimum tax liability based on their Alternative Minimum Taxable Income (AMTI) and a tax rate of 20%. AMTI adjusted taxable income by adding back certain tax preferences like accelerated depreciation, limiting the use of NOLDs, and limiting the use of certain tax credits like the Research and Development Tax Credit and the Foreign Tax Credit. Excess AMT paid could be carried forward as a credit to offset future regular tax liabilities but not below the minimum tax threshold.

For example, suppose a company had a regular tax liability of $500,000 but an AMT liability of $700,000 this year, as described in Table 1 (below). In this case, the company would be required to pay an additional tax of $200,000 under the AMT. However, this $200,000 is recorded as an AMT credit that is carried forward to the next year. In the next year, when the company’s regular tax liability is $800,000 and its AMT tax liability is $500,000, the company would pay the regular tax and could apply the $200,000 AMT credit from the prior year. This would reduce the company’s tax liability to $600,000.

|

Year 1 |

Year 2 |

|

|---|---|---|

|

Regular Tax Liabilty |

$500,000 |

$800,000 |

|

AMT Liability |

$700,000 |

$500,000 |

|

AMT Credit Applied |

$0 |

$200,000 |

|

Total Taxes Paid |

$700,000 |

$600,000 |

|

AMT Credit Generated |

$200,000 |

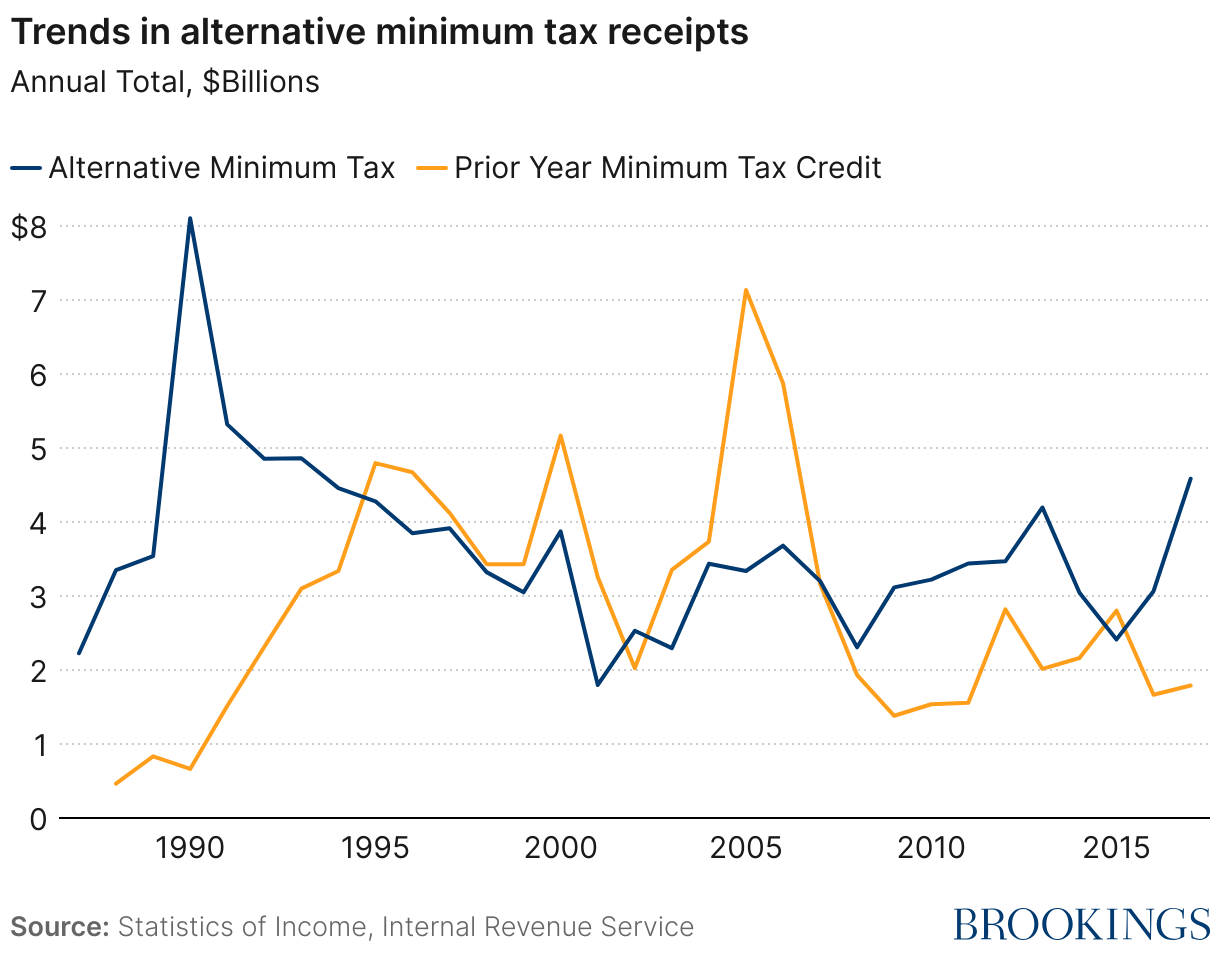

Figure 1, below, shows the annual alternative minimum tax liabilities (blue) and prior year AMT credits (orange) during the life of the pre-TCJA corporate AMT (1987–2017). This graph highlights the ebb and flow of AMT liabilities and credits over this period, where a steady stream of AMT liability is also paired with a steady stream of AMT credit. Note that the scale of the AMT in any given year is small within the context of corporate tax receipts: During decade prior to repeal, annual AMT liabilities were, on average, just 1.3% of total corporate tax receipts.

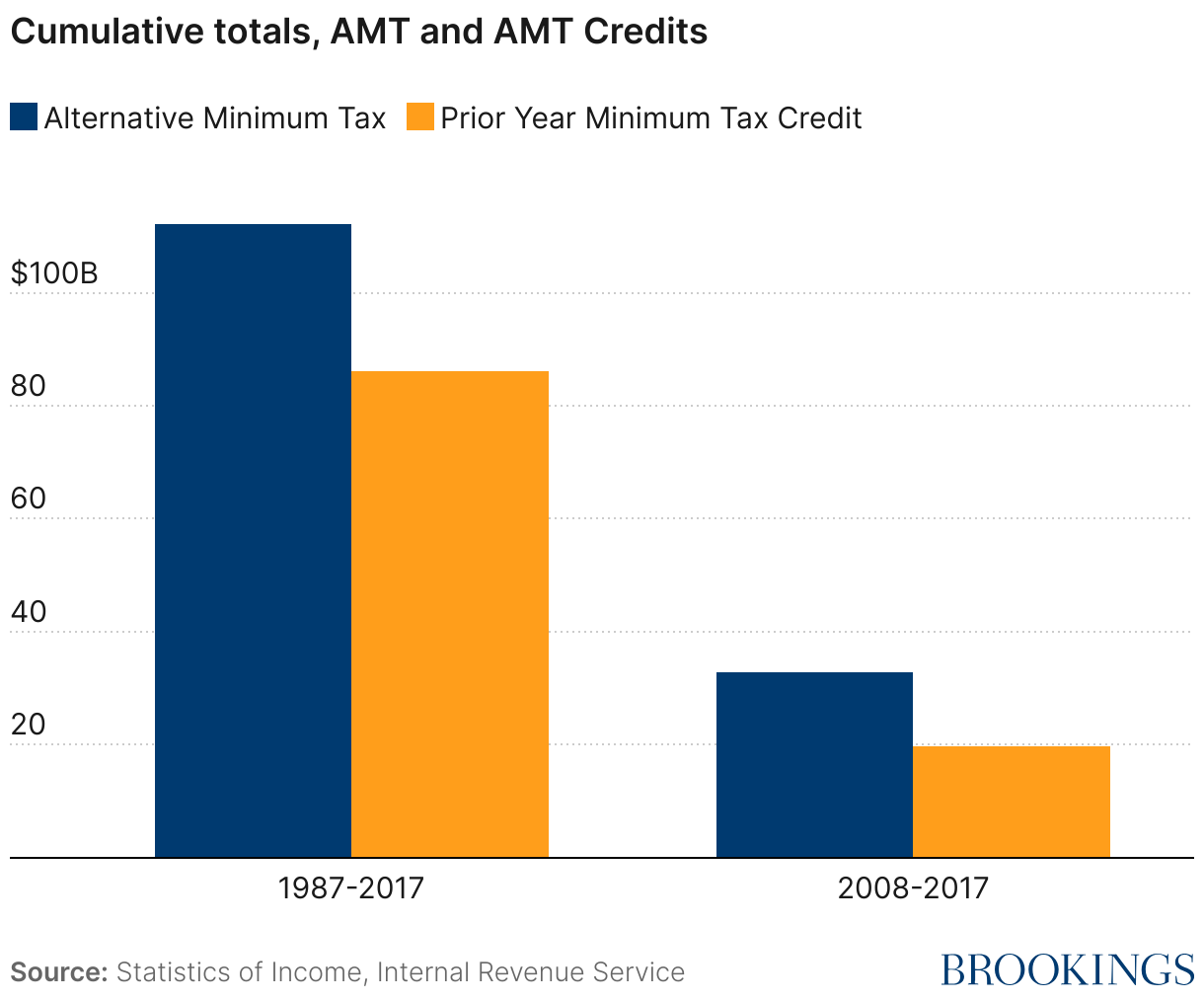

Figure 2 cumulates these totals during the full history of the AMT and separately during the decade prior to repeal. In both cases, most of the revenue earned by the AMT is eventually refunded in the form of a prior year tax credit. From 1987-2017, just $26.08 billion in net total revenue was raised by the AMT, $13.19 billion of which was earned during the decade prior to the repeal of the AMT.

CAMT and the 2022 Inflation Reduction Act

The IRA re-introduced the corporate AMT with several key changes from its previous version. First, the IRA imposes a 15% minimum tax, a reduction from the prior 20%. Second, the IRA introduced a new income measure, referred to as Adjusted Financial Statement Income (AFSI). AFSI is based on book income, but it adjusts book income to continue to allow certain deductions, credits, and other exclusions that are allowed for tax purposes but do not appear in financial statements. Third, the new corporate AMT has a more limited scope, applying only to large corporations based on their AFSI, whereas the old corporate AMT had no such restriction.

The new corporate AMT requires businesses to calculate their income three times: once under traditional taxable income, once to determine if they are in scope (over $1 billion in AFSI over the prior three tax years), and a final AFSI calculation that allows, for example, foreign tax credits, accelerated depreciation, certain general business credits, and net operating losses. As before, excess AMT paid could be carried forward as a credit to offset future regular tax liabilities but not below the minimum tax threshold. The new AMT became effective for tax years starting after December 31, 2022.

By tying the AMT tax liability to financial statement income, the new corporate AMT revives old questions about the costs and benefits of book-tax conformity. Central to these discussions is a reminder of the purpose of each measure of income. Taxable income is designed to inform the tax authorities about the tax liability of the taxpayer, whereas financial statement income is designed to inform creditors, investors, and the public about the financial health of the firm. Research shows that attempts to harmonize these measures reduce the quality of reported earnings by causing firms to bias their reported earnings to reduce their tax liability (Boynton, Dobbins, and Plesko 1992; Guenther, Maydew, and Nutter 1997; Maydew 1997; Desai 2003; 2005; Hanlon, Maydew, and Shevlin 2008). This suggests that the new corporate AMT could lead to a degradation of the quality of financial reporting without otherwise increasing tax revenue (Hanlon 2021).

Moreover, allowing many of the same deductions and credits against AFSI that tend to lead to low tax liability will likely limit the effectiveness of the new corporate AMT as a tool to ensure that firms that earn profit also pay a baseline amount of tax. To assess this question, preliminary research studies the effectiveness of the IRA corporate AMT design by using historical data and assuming that the new policy had been in place (Green et al. 2024; Blouin and Born 2024). These studies suggest that many of the issues with the pre-TCJA AMT are likely to persist. For example, these papers show that accelerated depreciation, NOLDs, and foreign tax credits still allow corporations to significantly reduce their effective tax rates under the new system. The papers also highlight that the revenue generated by the new corporate AMT is likely to be smaller than initial projections from the Joint Committee on Taxation, particularly after accounting for the AMT carryforward and for corporations adjusting their accounting practices to optimize around the new rules.

International considerations: Global tax competition

Tax policies that implement a minimum tax on business income tie into broader international tax debates, particularly with respect to international tax competition and the OECD-lead Global Tax Deal. Currently, each country determines its own tax treatment of multinational corporate income by balancing domestic revenue needs with competitive pressures to locate operations in low-tax jurisdictions. Tax competition happens when countries lower their corporate tax rates or offer special deductions or credits to multinational corporations that relocate some or all of their operations. These tax benefits reduce the effective tax rate of corporations operating within their borders, reducing total taxes paid across the multinational organization. While these tax benefits may increase domestic investment, this behavior also classically creates a “race to the bottom” that tends to depress effective tax rates across the globe, reducing corporate tax revenue and, therefore, government spending on public services.

To combat this, Pillar 2 of the Global Tax Deal, endorsed by more than 130 countries including the United States, seeks to establish a 15% global minimum tax to ensure that multinational firms pay a minimum level of tax, regardless of where they operate. This reduces the incentive for multinational corporations to shift operations or profit to low-tax jurisdictions like tax havens. A corporate AMT in the U.S. is essential to align with these goals.

However, key differences exist between the IRA’s corporate AMT and Pillar 2. Most notably, the IRA’s corporate AMT blends foreign and domestic income for the purposes of determining tax domestic liability, consistent with other U.S. international tax policies like Global Intangible Low-Taxed Income (GILTI). Pillar 2, on the other hand, requires that the global minimum tax be applied separately in each jurisdiction where a company operates. Under the approach of Pillar 2, a corporation could owe additional tax in a high jurisdiction if it underpays in a low-tax country relative to a 15% minimum tax rate. The IRA’s corporate AMT does not follow this approach. This and other differences in the treatment of certain deductions and credits under the IRA’s AMT pose challenges in aligning U.S. tax policy with the standards outlined by Pillar 2 (Blouin and Born 2024).

Benefits and challenges of the corporate AMT

A well-designed corporate AMT can enhance the fairness of the tax code by ensuring that corporations with significant economic profit cannot reduce their tax liability to zero through excessive use of tax expenditures. However, limiting the use of tax expenditures requires careful consideration of which tax expenditures tend to reduce effective tax rates and drive tax liabilities to zero, what constitutes excessive, and why those tax expenditures were introduced within the context of optimal tax policy.

So far, the legislature has shown little interest in addressing the challenges of designing a corporate AMT. Over the past four decades and across multiple iterations, alternative definitions of taxable income used for the AMT have largely preserved the major tax expenditures that are commonly associated with low or zero tax liability. The rationale for maintaining each of these tax provisions in isolation clear: Accelerated depreciation incentivizes capital investment by allowing businesses to recover the costs of their investments more quickly, which can stimulate growth and innovation. General business credits, including those for research, support activities that enhance productivity, innovation, and global competitiveness. NOLDs smooth income over time, reflecting the cyclical nature of profits, while FTCs prevent double taxation of foreign income, promoting international competitiveness. To the extent one or several of these expenditures excessively reduce taxable income such that a firm’s effective tax rate falls below the minimum tax rate (say, 15%), choices must be made about which of these expenditures should take precedent. Or, we must be comfortable with the fact that a blunt AMT, which simply limits taxable income without regard for specific tax expenditures, will dampen the intended effect of tax policies like accelerated depreciation by reducing the value of the expenditure.

In the meantime, the corporate AMT, especially as enacted by the IRA, introduces significant complexity for the taxpayer. The corporate AMT now requires that businesses maintain four different sets of books: one for financial accounting, one for the regular tax computation, one to determine whether they are in scope, and one to determine their AMT liability to the extent that they are in scope (Hanlon 2021). Further, the Office of Management and Budget estimates that the cost of complying with the corporate AMT will cost more than $100,000, a 50% increase over the baseline cost of complying with the regular corporate tax (roughly $200,000) (Blouin and Born 2024).

These compliance costs must, of course, be balanced against the revenue it is expected to collect. The Joint Committee on Taxation estimated that the IRA’s corporate AMT would raise $222 billion from FY2022–FY2031 (Joint Committee on Taxation 2022). However, these estimates may have been overly optimistic. For example, and as previously described, the old corporate AMT raised just $13 billion in net tax revenue during its last ten years. Many of the same tax expenditures that were allowed under the old corporate AMT are also allowed under the new corporate AMT, and companies can continue to use AMT payments to reduce their taxes in the future. Consistent with this, Blouin and Born (2024) show that if the new AMT had been in effect over the past decade, 40% of the revenue raised would have been used to lower future taxes. This makes it hard to see how the new AMT could generate almost 20 times more revenue over the next ten years than the old AMT did.

Conclusion

Specific policy choices embedded in the U.S. tax code create the opportunity for low-to-zero tax liability, even when a firm earns economic profit. Each of these choices can be justified under the principles of optimal tax design, such as accelerated deductions and credits to encourage capital and intangible investment, foreign tax credits that ensure that multinational corporate profits are only taxed once, or NOLDs that smooth income over time in light of the cyclical nature of profits. While the corporate AMT can serve as a corrective mechanism to ensure that every corporation pays some baseline level of tax, it is critical to acknowledge that this policy alone does not resolve the underlying structural decisions that lead to minimal tax liabilities in the first place.

Other considerations, such as international tax competition or the pursuit of fairness in the tax system, may justify a corporate AMT alongside other policies in an optimal corporate tax system. However, design and implementation remain significant challenges. With this in mind, a more careful and nuanced approach to how the corporate AMT is structured is warranted. Future reforms should seek to balance the desire for fairness and the need for revenue with the desire to influence corporate behavior through the tax code and maintain the global competitiveness of U.S. corporations.

-

References

Blouin, Jennifer, and Nathan Born. 2024. “The Corporate Alternative Minimum Tax: A Congressional Folly.” National Tax Journal 77 (2): 413–47. https://doi.org/10.1086/730211.

Bokulic, Caitlin, Erin Henry, and George A. Plesko. 2012. “Reconciling Global Financial Reporting with Domestic Taxation.” National Tax Journal 65 (4): 933–59. https://doi.org/10.17310/ntj.2012.4.11.

Boynton, Charles E., Paul S. Dobbins, and George A. Plesko. 1992. “Earnings Management and the Corporate Alternative Minimum Tax.” Journal of Accounting Research 30:131–53. https://doi.org/10.2307/2491198.

Desai, Mihir A. 2003. “The Divergence between Book Income and Tax Income.” Tax Policy and the Economy 17 (January):169–206. https://doi.org/10.1086/tpe.17.20140508.

———. 2005. “The Degradation of Reported Corporate Profits.” Journal of Economic Perspectives 19 (4): 171–92. https://doi.org/10.1257/089533005775196705.

Government Accountability Office. 2016. “Corporate Income Tax: Most Large Profitable U.S. Corporations Paid Tax but Effective Tax Rates Differed Significantly from the Statutory Rate | U.S. GAO.” https://www.gao.gov/products/gao-16-363.

———. 2022. “Corporate Income Tax: Effective Rates Before and After 2017 Law Change | U.S. GAO.” https://www.gao.gov/products/gao-23-105384.

Green, Danielle H., Erin Henry, Caitlin McGovern, and George A. Plesko. 2024. “The Demographics of the CAMT: Insights from Tax Return Data.” National Tax Journal 77 (2): 383–411. https://doi.org/10.1086/730168.

Guenther, David A., Edward L. Maydew, and Sarah E. Nutter. 1997. “Financial Reporting, Tax Costs, and Book-Tax Conformity.” Journal of Accounting and Economics 23 (3): 225–48. https://doi.org/10.1016/S0165-4101(97)00009-8.

Hanlon, Michelle. 2003. “What Can We Infer about a Firm’s Taxable Income from Its Financial Statements?” National Tax Journal 56 (4): 831–63. https://doi.org/10.17310/ntj.2003.4.07.

———. 2021. “The Possible Weakening of Financial Accounting from Tax Reforms.” The Accounting Review 96 (5): 389–401. https://doi.org/10.2308/TAR-2021-0198.

Hanlon, Michelle, Edward L. Maydew, and Terry Shevlin. 2008. “An Unintended Consequence of Book-Tax Conformity: A Loss of Earnings Informativeness.” Journal of Accounting and Economics 46 (2): 294–311. https://doi.org/10.1016/j.jacceco.2008.09.003.

Joint Committee on Taxation. 1987. “JCS-10-87.” https://www.jct.gov/publications/1987/jcs-10-87/.

———. 2022. “JCX-18-22.” https://www.jct.gov/publications/2022/jcx-18-22/.

Maydew, Edward L. 1997. “Tax-Induced Earnings Management by Firms with Net Operating Losses.” Journal of Accounting Research 35 (1): 83–96. https://doi.org/10.2307/2491468.

Author

-

Acknowledgements and disclosures

The Brookings Institution is financed through the support of a diverse array of foundations, corporations, governments, individuals, as well as an endowment. A list of donors can be found in our annual reports published online here. The findings, interpretations, and conclusions in this report are solely those of its author(s) and are not influenced by any donation.

-

Footnotes

- Corporations can reduce their tax liability legally (through tax avoidance) or illegally (through tax evasion). Evidence suggests that the zero or negative taxes owed by major corporations are primarily the product of avoidance behavior—that is, completely legal use of deductions and credits—rather than criminal activity (Government Accountability Office 2022).

- The TCJA provisioned new minimum taxes on certain foreign income through the Global Intangible Low Tax Income (GILTI) and the Base Erosion and Anti-Abuse Tax (BEAT).

- Income in this measure typically reflects book or financial statement income rather than taxable income.

- The 2017 TCJA limited the NOLD so that a company could reduce otherwise positive tax liability by, at most, 80%. In the case where this limits the NOLD, the remainder can be carried forward into future years.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).