This Policy Brief is based on an article entitled “Efficient and Equitable Income Taxation of the Affluent,” published in Tax Notes, November 18, 2024.

Tax policy discussions regarding the wealthy typically focus on how much affluent households should pay relative to other households. For example, President Biden stated, “Let’s make corporations and wealthy Americans start paying their fair share” in his 2022 State of the Union address. Similarly, criticism of the Tax Cuts and Jobs Act of 2017 (TCJA) often centers on how it disproportionately reduced taxes for high-income households.

These arguments agree that the wealthy should pay more in taxes, but the current debate has focused less on how to structure the taxation of high-income households. The structure of taxes is important because while typical American households primarily earn income in the form of wages and salaries, affluent households typically receive a much greater share of their income in the form of returns to capital. As a result, the taxation of these households can have a meaningful impact on neutrality and efficiency of the overall tax code.

The taxation of the wealthy can create distortions which can influence numerous taxpayer choices and thus affect economic efficiency and horizontal equity. Although changes to the tax system over the past several decades have greatly reduced these economic distortions, there is still room for improvement. Fundamental tax reform could further reduce or eliminate these distortions.

How the affluent earn their income

In general, households can earn both labor and capital income. Labor income includes wages, salaries, and fringe benefits. Fringe benefits are payments to, or on behalf of, workers in lieu of cash and can include health insurance, transportation, entertainment, and club memberships. Further, employers make several payments on behalf of workers, such as contributions to government social programs like Social Security, Medicare, and unemployment insurance. Capital income is the return a household receives from assets, and it can come in several forms. Households may earn interest income, rents, royalties, corporate dividends, capital gains, pass-through business profits, and returns to pensions.

In the aggregate, most income earned by households in the United States is labor compensation. In 2023, about 69% of net factor income was labor compensation (either wages, salaries, or fringe benefits).1 Various forms of capital income constitute the remaining 31%. The largest components of capital income are corporate profits (13.4% of national income) and proprietor’s income (9% of national income). The remaining capital income comes from net interest and imputed rental income from homeowner-occupied housing (8% of national income).

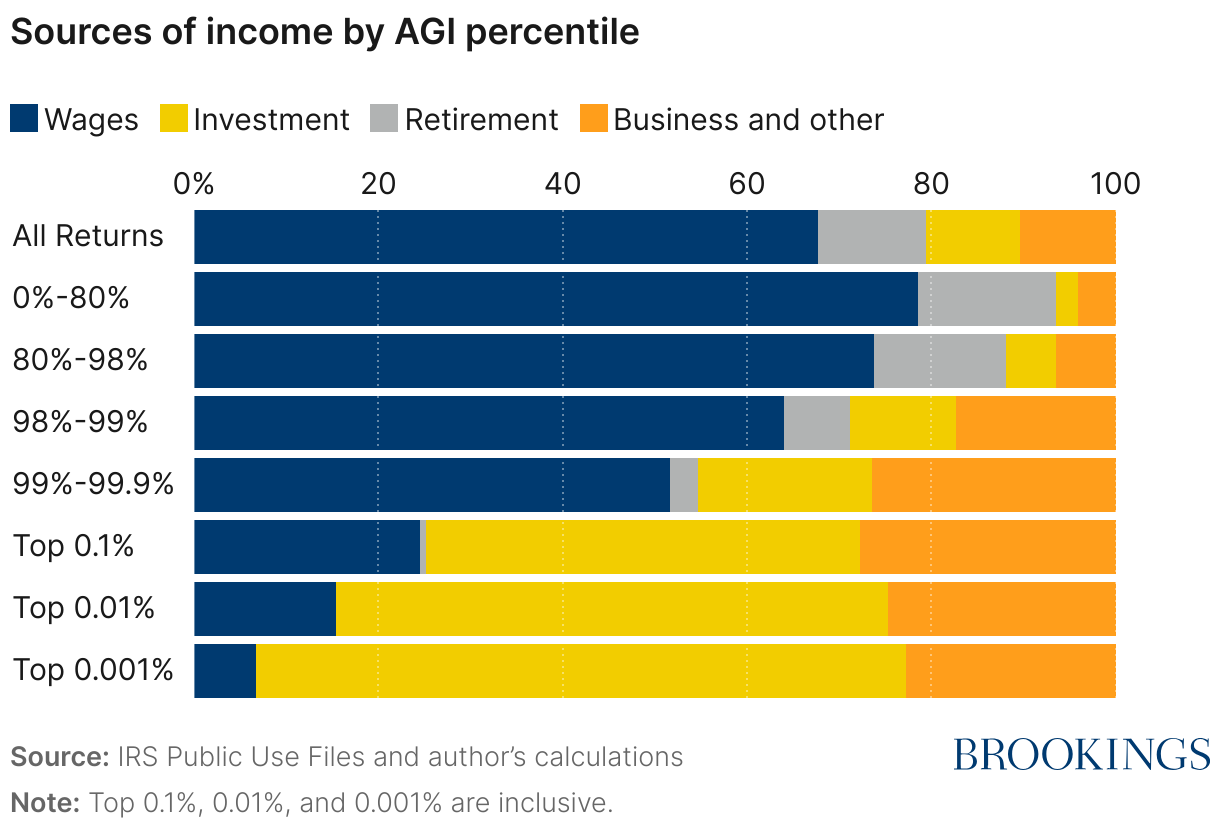

Most Americans receive almost all their income through wages and retirement income (pensions, section 401(k) plans, Social Security, and IRAs) (Figure 1). The most recent available IRS data (2014) show that wages and retirement income made up 93% of adjusted gross income (AGI) for households in the bottom 80% of the income distribution. Even for households in the 98th to 99th income percentile, wages and retirement income accounted for 71% of AGI.

At the very top of the income distribution, wages and retirement income are less important, accounting for just 15% of the income of the top 0.01% of households and 7% of the income of the top 0.001%. These households receive most of their income from assets and passthrough businesses. These items constitute 85% of income for the top 0.01% and 93% of income for the top 0.001%.

Related Content

How income is taxed under current law

Labor income

Under current law, labor income is taxed through the individual income tax and two federal payroll taxes. The individual income tax features a graduated rate structure that, after allowing for the standard or itemized deductions, features tax brackets ranging from 10% to 37%. The Old-Age, Survivors, and Disability Insurance tax collects 12.4% of wages up to $168,600 (a cap that is adjusted annually for changes in average wages). The Medicare hospital insurance tax collects 2.9% of wages and salaries, without limit. Each tax is split equally between employer and employee.

Filers with modified AGI above $200,000 ($250,000 for married couples filing jointly) also face an “additional Medicare tax” of 0.9% of wages, salaries, and self-employment income. Some fringe benefits (for example, health insurance) are exempt from taxation or face deferred taxation (for example, contributions to section 401(k) plans). Other fringe benefits are taxed as ordinary income (for example, gym memberships, bonuses, and employer-provided vehicles).

Capital income

Tax rules for capital income are more complex than those for labor income. As with labor income, some forms of capital income face multiple taxes, some are taxed at ordinary rates, and some are partially or wholly exempt.

Corporate profits face the corporate income tax, a flat 21% entity-level tax. After-tax corporate profits that are distributed to shareholders as dividends are either taxed as qualified income at a rate up to 20% or as ordinary income at a rate up to 37%. Retained earnings that result in appreciated corporate stock held for less than a year (short-term gains) are taxed as ordinary income (like wages and salaries) at a statutory rate of up to 37% or, if held for more than a year are treated as qualified income and taxed at a rate of 20%.

Individual also earn passthrough business income—profits reported on individual tax returns from sole proprietorships, S corporations, partnerships, and limited liability companies—which is taxed as ordinary income and faces statutory tax rates of up to 37%. Some passthrough business profits can qualify for section 199A, the 20% deduction for qualified business income. The top marginal tax rate for income qualifying for the section 199A deduction is 29.6% (80% of the 37% top statutory rate).

Net business income of sole proprietors also faces tax under the Self-Employment Contributions Act (SECA), which mirrors the payroll taxes on wages and salaries. The SECA tax is 15.3% of certain business income on the first $168,000 of net income and 2.9% on income over that threshold. The 0.9% additional Medicare tax also applies to this income.

Dividends and realized capital gains, as well as certain pass-through business income earned by high-income individuals, also face the net investment income tax, a 3.8% tax that applies to taxpayers with modified AGI above $200,000 for single filers and $250,000 for married couples filing jointly.

Other capital income including net interest received, rents, and royalties is generally taxed as ordinary income, although in some cases rents and royalties can qualify for section 199A. All three forms of income are subject to net investment income (NII) tax.

How the tax code distorts decision making

Given the various types of income earned by high-income households, the differences in how this income is taxed has implications for both the neutrality and efficiency of the tax code. For example, taxing capital income at higher rates would increase the progressivity of the tax system by raising the tax burden on high-income households. However, this could also change the relative tax treatment of capital and labor income or other types of capital income in ways that encourage tax avoidance behavior and could distort real economic decision making.

There are numerous ways the current tax code influences taxpayer behavior, but over the past decade, lawmakers, policy analysts, and academics have focused on a handful of important margins: Whether to take income in taxable form, how to classify taxable income, which organizational form to adopt, which asset to invest in, how to finance investment, and when to realize gains. Although each of these decisions has distinct impacts on an individual’s tax liability, the magnitude of each of these distortions varies under current law.

Whether to take income in taxable form

When tax rates change, taxpayers adjust their behavior, often with the goal of minimizing or reducing their tax burden by either reducing taxable forms of income such as wages and capital income or increasing deductions. For affluent households, the top marginal rate on taxable income influences the decision to report an additional dollar of taxable income by affecting the net-of-tax return on an additional dollar of income. For example, under current law the top statutory tax rate is 37%, meaning that the net-of-tax rate is 0.63. Restoring the top tax rate to 39.6% would reduce the net-of-tax rate by 3.65% to 0.604. At a -0.25 elasticity, this would imply that taxable income would fall by nearly 1% for taxpayers subject to the top tax rate.

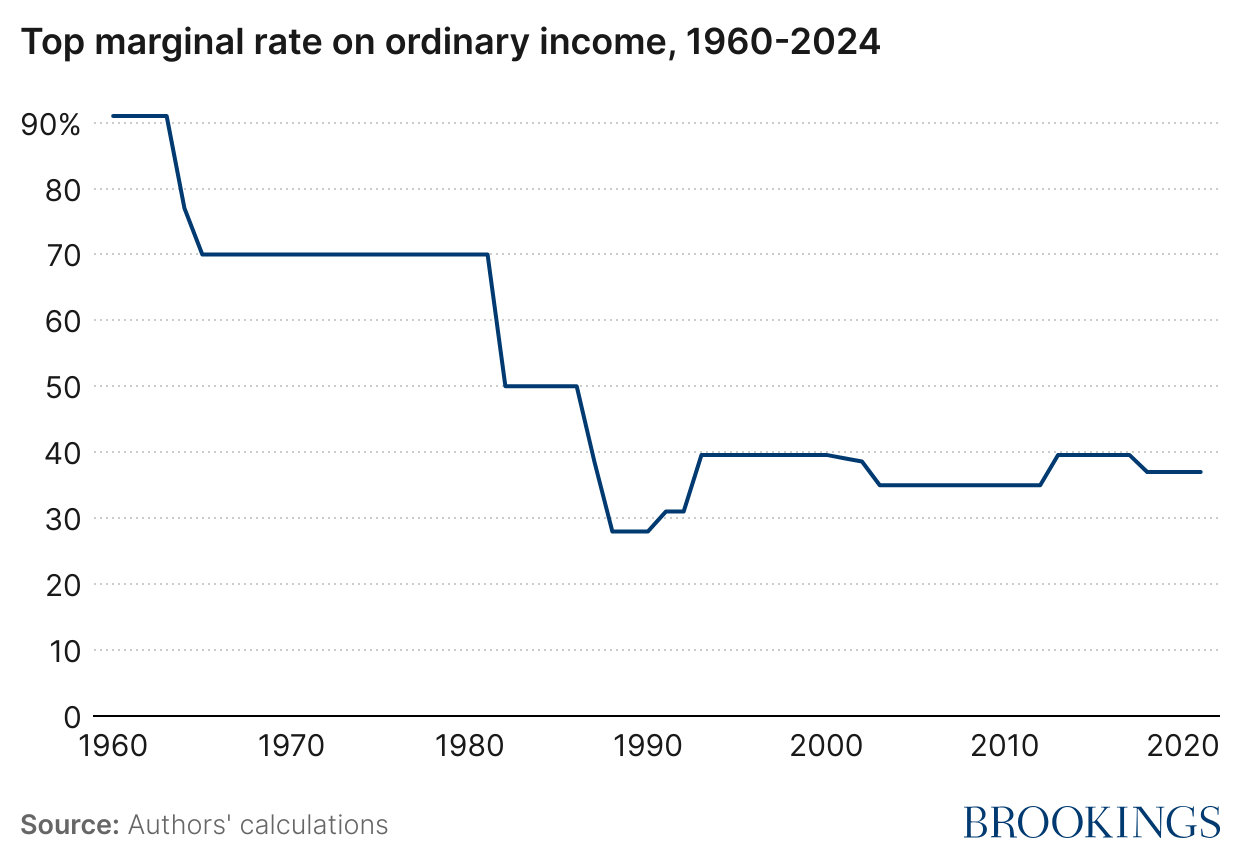

In general, the top statutory tax rate on ordinary income has declined over time, reducing the incentive to shield taxable income from taxation (Figure 2). In 1960, the top statutory tax rate on ordinary income was 91%. This declined to 70% after the 1964 tax cuts and to 50% after the 1981 tax cuts. The last significant reduction in the top statutory tax rate was included in the Tax Reform Act of 1986, which reduced the top statutory tax rate to 28%. The top rate was then increased multiple times in the 1990s, first to 31% in 1991 and then to 39.6% in 1993. Since then, the top rate has varied only slightly. It was temporarily cut from 39.6% to, eventually, 35% as part of the Economic Growth and Tax Relief Reconciliation Act of 2001 before reverting to 39.6% in 2013. Most recently, the top rate was cut to 37%, but it is scheduled to again revert to 39.6% in 2026.

How to classify taxable income

Most affluent Americans are owners of, or significant investors in, closely held businesses. Using administrative tax data from 2014, Matthew Smith et al. show that more than 69% of the top 1% of earners (and more than 84% of the top 0.1%) have at least some income from passthrough businesses. Owners of closely held businesses have substantial latitude to classify their compensation as either wage or capital income for tax purposes. Meanwhile, investors are often able to select a role as active or passive investors, while corporations can decide to remit profits to owners through either dividends or share repurchases. As a result, differences in how these varying forms of income are taxed have important implications for how the wealthy report their business income.

The incentive to report income as one form or another is driven by differences in the top statutory tax rate on reported income.

In the case of certain pass-through businesses, this distortion is significant: Wages face a tax rate 10.6 percentage points higher than business profits (Table 1). The large gap is the result of two existing policies: section 199A, which reduces the top statutory income tax rate on these profits from 37% to 29.6%, and gaps in SECA and the NII tax, which do not apply to these profits. Other passthrough businesses do not face this sort of incentive. Owners of general partnerships and sole proprietorships generally do not split their compensation between labor and capital returns. All income is taxed as self-employment income, which is treated roughly the same as labor compensation.

|

Organizational Form |

Profits |

Labor Compensation |

Difference |

|---|---|---|---|

|

Sole Proprietorship/General Partner |

32.6 |

32.6 |

0 |

|

Active S Corporation/Partnership |

29.6 |

40.2 |

-10.6 |

|

Closely-hed C Corporation |

39.8 |

40.2 |

-0.4 |

Source: Authors’ Calculations

The incentive to report income as profits rather than wages is much smaller for owners of closely held C corporations. Corporate profits face a similar top marginal tax rate as labor compensation. All in, C corporation profits are taxed at 39.8%, which is the combined burden of the corporate income tax and the individual income tax on dividends (including the 3.8% NII tax). This is only 0.4 percentage points lower than the top marginal tax rate on labor compensation.

For C corporations, there has been a long-standing tax advantage to returning profits to their shareholders in the form of stock buybacks rather than dividends. Although dividends and stock buybacks face the same top statutory tax rate of 23.8%, an advantage exists for buybacks because a portion of the return is not immediately taxed as it is in the case of a dividend.

Which organization form to adopt

Under current law, there are two major legal forms of businesses: C corporations and passthrough businesses—the latter including sole proprietorships, partnerships, and S corporations. Passthrough businesses account for the vast majority of businesses and a majority of total business profits. Passthrough entities do not pay tax at the entity level. Rather, their owners or partners report their shares of profits on their individual income tax returns. Taxpayers choose the legal form of their business based on the relative costs and benefits of each legal form (for example, in terms of the legal liability an entity protects against, the ability to borrow funds, and tax liability).

Under current law, the tax code places a lighter tax burden on passthrough businesses than on C corporations. Table 2 compares the average effective tax rate (ETR) by major legal form of organization. The average ETR is a forward-looking ETR that measures the share of pretax profits subject to tax. This measure includes the effect of statutory tax rates on returns net of any deductions or credits a business expects to receive. Under current law, C corporations, on average, face a 6.6 percentage point higher average ETR than passthrough businesses (36.1% versus 29.5%), when individual-level taxes on corporate payouts are included in the effective corporate rate.

|

Organizational Form |

Average Effective Tax Rate |

|---|---|

|

C corporation |

36.1 |

|

Pass-through Business |

29.5 |

|

Difference |

6.6 |

Source: Authors’ Calculations

Which assets to invest in

The taxation of companies also influences their investment decisions. Businesses use a mix of tangible and intangible assets in their production processes, and, under current law, these assets often face markedly different tax burdens because of differences in depreciation schedules and tax credits for certain types of investments. Assets with more favorable treatment have higher after-tax returns, which can result in an inefficient allocation of assets throughout the economy.

|

Asset Type |

Tax Wedge |

|---|---|

|

Intellectual Property |

-0.1 |

|

Equipment and Software |

0.5 |

|

Residential Structures (Not Owner Occupied) |

0.9 |

|

Non-Residential Structures |

1.1 |

|

Inventories |

1.4 |

|

Land |

1.4 |

|

Standard Deviation |

0.5 |

Source: Authors’ Calculations

Table 3 compares the tax wedge on six major types of assets. The tax wedge measures the difference between the pretax return and the after-tax return on new investment. Under current law, intellectual property faces the lowest tax burden (a tax wedge of -0.1 percentage points). This is because a major component of IP products—research and development—is eligible for the research and experimentation (R&E) tax credit. Equipment and software face a tax wedge of 0.5 percentage points. Equipment and software’s tax wedge is lower than that of other assets because they often qualify for bonus depreciation, which reduces the effective tax burden on these assets relative to other depreciation regimes. In contrast, nonresidential and tenant-occupied residential structures, which do not generally benefit from accelerated depreciation, face tax wedges of 0.9 and 1.1 percentage points, respectively. Finally, inventories and land face the highest tax burdens (tax wedge of 1.4 percentage points each) because the cost of these assets cannot be deducted until they are sold.

Overall, the standard deviation of the tax wedge across all capital assets is 0.5 percentage points—a deviation equal to 50% of the weighted average tax wedge across all assets of 1 percentage point.

How to finance investment

Businesses finance new investment by issuing new equity shares to investors, using retained earnings, or borrowing funds. Without tax considerations, businesses would balance debt and equity financing, equalizing the marginal cost of each source. Under current law, there is a clear tax benefit to using debt financing over equity financing to fund business activities. This encourages companies to use more debt than they would in the absence of taxation. Businesses must balance this benefit with the nontax costs of debt, such as financial distress costs, debt overhang, and personal income tax rates for investors holding debt.

|

Financing Form |

Tax Wedge |

|---|---|

|

Debt |

0.6 |

|

Equity |

0.8 |

|

Difference |

0.2 |

Source: Authors’ Calculations

Under current law, the tax wedge on debt-financed investment is 0.6 percentage points, which is 0.2 percentage points lower than the tax wedge of 0.8 percentage points on equity-financed investment (Table 4). The bias in favor of debt-financed investment is primarily the result of taxing debt financing once, while taxing equity investment twice. The bias is partially offset by limitations on net interest expense that were enacted as part of the TCJA and the lower tax rates on dividends and capital gains.

When to realize gains

The current tax system relies in part on a realization principle. For administrative convenience (and perhaps liquidity reasons), taxpayers are often taxed only when they realize income. For example, capital gains and losses are counted only when a taxpayer disposes of an asset. As a result, taxpayers have an incentive to delay selling an appreciated asset and to accelerate the sale of a depreciated asset to realize a loss.

For example, consider an asset valued at $100 today. At a real rate of return of 5% and 2% inflation, this asset would appreciate to $107.25 if held for one year and continuously compounded. If the asset is sold at that point, the tax would be $1.73 (rounded up), assuming the taxpayer faced the top statutory tax rate of 23.8%. The after-tax value would be $105.53 (rounded up), and the real average annual after-tax rate of return would be 3.4%. But if the same taxpayer held the asset for 10 years, the asset would grow to $201.38. When sold, it would face a tax of $24.13 for a total after-tax value of $177.25. This return would yield an average 3.7% after-tax return—an average return of 0.3 percentage points higher than if the asset were sold after one year, even though the market rate of return, rate of inflation, and tax rate did not change over the period.

How tax reform can enhance neutrality and efficiency

Ideally, tax reform would limit or eliminate these and other distortions. Fundamental reforms can differ significantly in both their base (for example income or consumption) and their structure (flat rate or progressive rate). Some of these choices impact how and the extent to which a reform addresses these distortions. To demonstrate, we examine three canonical reforms—Treasury’s broad-based comprehensive income tax (CIT), the Hall-Rabushka flat tax, and Edward D. Kleinbard’s business enterprise income tax (BEIT).

The CIT would apply to all sources of income and tax that income at progressive rates. Labor income from wages, salaries, fringe benefits, and retirement income would be taxed. For capital income, the tax base would include all business income, interest, dividends, rents, accrued (as opposed to just realized) capital gains, and the imputed rent from owner-occupied housing. Deductions would be allowed only to ensure income is taxed in the hands of those who ultimately consume it. Passthrough businesses would maintain flow-through treatment. C corporations would continue to face a separate entity-level tax, which would be integrated with the individual income tax. Businesses would depreciate fixed assets in line with economic depreciation, and interest expenses would be fully deductible.

Hall and Rabushka propose a so-called flat tax, which is a two-part value-added tax (VAT). Wages and pension income would be taxed at the individual level, above an exemption amount. Besides the family exemption, there would be no deductions or credits for households. The nonwage portion of value-added—cash flow—would be taxed at the entity level. Both taxes would have the same statutory tax rate.

Kleinbard’s BEIT would replace the current tax system with a split rate tax system. All businesses would face a flat entity-level tax. Taxable business income would be calculated roughly the same way as under current law with two exceptions. First, interest expenses would no longer be deductible. Second, businesses would receive what is called a cost of capital allowance (COCA). This allowance would be equal to a set percentage of the adjusted basis of assets each year. The provisions would effectively exempt a deemed normal return to assets from the entity-level tax. At the individual level, labor compensation would face a progressive tax, while capital income would face a flat tax at the same statutory tax rate as the business tax. The capital income tax would not be based on capital income received. Rather, individuals would face tax on a deemed normal return to their assets which would match the COCA provided to business entities. Unlike current law, there would be no tax on capital gains when realized. For purposes of our analysis, we assume no individual deductions or credits.

Table 5 compares how these reforms would impact the six distortions noted above.

|

Margin |

Current Law |

CIT |

Flat Tax |

BEIT |

|---|---|---|---|---|

|

Whether to take income in taxable or non-taxable forms |

Incentive to shield | Smallest reduction in incentive to shield; eliminates ability to shift income between wages and profits and increase itemize deductions | Larger reduction in incentive to shield; eliminates ability to increase itemized deductions but could create new avoidance opportunities | Larger reduction in incentive to shield; eliminates ability to shift income between wages and profits and increase itemize deductions |

| How to classify taxable income | Notable incentive for pass-through businesses to report income as profits instead of wages; small incentive to report income as profits for C corporation owners | Eliminates income reporting distortions; eliminates tax differential between dividends and stock buybacks | Eliminates income reporting distortions; eliminates tax differential between dividends and stock buybacks | Expands incentive to report labor income as capital income; eliminates tax differential between dividends and stock buybacks |

| What organizational form to adopt | Tax advantage for pass-through businesses | Mostly eliminates distortions across legal form; potential tax benefit for corporations relative to pass-through businesses depending on tax status of owner | Eliminates distortions across legal form | Mostly eliminates distortions across legal form; potential tax benefit for corporations relative to pass-through businesses depending on tax status of owner |

| Which assets to invest in | Clear tax incentive to invest in short-lived assets over longer-lived assets, inventories, and land | Mostly eliminates tax distortions across types of assets; potential distortion of the ownership of capital assets | Eliminates tax distortions across types of assets; incentivizes business investment | Eliminates tax distortions across types of assets; creates a positive and uniform burden on new business investment at the individual level |

| How to finance investment | Clear tax incentive to using debt financing over equity | Mostly eliminates distortions across forms of financing—may create a debt subsidy or penalty | Eliminates distortions across forms of financing; does not distort the cost of investment financed by retained earnings | Eliminates distortions across forms of financing; some distortion caused by taxing capital gains at a flat rate |

| When to realize capital gains | Creates lock-in effect for appreciating assets and incentive to accelerate the selling of declining assets | Reduces lock-in effect on appreciating assets; eliminates under certain policies | Eliminates lock-in effect | Reduces but does not eliminate lock-in effect |

Despite underlying differences in the structure of these reforms, all three of these reforms would generally address three of the six distortions: which organizational form to adopt, which asset to invest in, and how to finance a new investment. Although they differ in the extent to which they tax the returns to capital, they do so uniformly, regardless of the characteristics of the underlying investment. The CIT would tax all returns to investment uniformly at the statutory tax rate.2 The BEIT would tax the returns to capital in the hands of savers at the statutory tax rate but exempt them in the hands of business entities. The flat tax would exempt all capital from taxation. As a result, all investments under each reform would face the same tax burden.

All three reforms have the potential to limit the incentive to reduce taxable income, but the CIT would have the smallest impact. Of the three reforms, the flat tax would reduce incentives for avoidance the most by lowering the top statutory tax rate, thereby greatly limiting the tax benefit of shielding taxable income. At the flat tax’s originally proposed statutory tax rate of 19%, for example, the net-of-tax rate would rise from 0.63 to 0.81 or by 28.6%. Further, the flat tax would have no personal deductions, eliminating the ability to use them to reduce taxable income. Although the BEIT maintains a progressive individual income tax rate structure, it would still reduce the incentive to decrease taxable income because, as discussed above, we assume it would eliminate all personal deductions. The CIT would maintain more opportunities for taxpayers to reduce taxable income by maintaining a progressive rate structure as well as a handful of deductions.

While the flat tax and the CIT would tax all forms of reported income at the same statutory tax rate, the BEIT would maintain meaningful differences between the top marginal tax rates on capital and labor income. All capital income would face a flat tax rate while labor income would be taxed at progressive rates, some of which exceed the capital income tax rate. As a result, this proposal would expand the incentive that exists under current law to report labor income as capital income. For example, a taxpayer who faces a top tax rate of 40% on wages and a capital tax rate of 25% could save 15 cents per dollar of earnings reported as capital income instead of as wages. The BEIT, like current law, deals with this issue with a somewhat arbitrary rule that requires capital returns far exceeding a deemed normal return to be reported as labor income.

All three reforms would also reduce the tax differential between dividends and stock buybacks. Under the CIT, all capital income faces the same statutory tax rate, including dividends and capital gains. Further, capital gains are taxed as they accrue, eliminating the deferral benefit for shareholders of companies that buy back their shares. The flat tax would eliminate this tax differential in the opposite way: Capital income would no longer face any individual income tax. As a result, the tax consequences of returning profits in the form of dividends or buybacks are the same: no tax. The BEIT would similarly eliminate the tax differential between dividends and stock buybacks by eliminating taxes on these transactions. As described above, individual capital income is not taxed. Rather, individuals are taxed on an imputed return on their assets each year. Thus, the tax burden on corporate equity is fixed, regardless of how cash is returned to shareholders.

BEIT would also reduce the benefits of deferral slightly less than the CIT and flat tax. Under the CIT, capital assets would be taxed as they appreciate. Thus, the ETR on capital assets would be equal to the taxpayer’s statutory tax rate, regardless of the holding period. Elimination of the lock-in effect under the CIT requires taxing assets mark-to-market or using a similar structure. Under the flat tax, the ETR would be zero at the margin and invariant regarding the holding period. The BEIT would also reduce the lock-in effect. As described above, the BEIT would not tax capital gains when realized. Instead, it would impute the normal return on business assets to taxpayers each year and tax those assets at a flat tax statutory tax rate. Thus, taxes would not depend on realizing a gain. Further, any unrealized appreciation at death is taxed. Kleinbard notes that although realized gains do not face immediate tax, the proceeds do face tax if reinvested and increase a taxpayer’s basis in capital assets, and that could discourage sale. The BEIT (and potentially the CIT) would also require special rules for gains attributed to the returns to entrepreneurship. Those rules could discourage firms from going public.

Conclusion

Tax policies affecting the affluent have important consequences for the equity and efficiency of the tax system. We have focused on six tax-related decisions that affluent households often face: whether to take income in taxable or nontaxable forms, how to classify taxable income, which organizational form to adopt, which assets to purchase, how to finance investment, and when to realize capital gains.

All six of the issues we have identified can be addressed to a large extent with either income or consumption tax reforms. However, progressive individual income tax rate structures can cause some problems by creating labor/capital arbitrage opportunities for closely held businesses, ownership distortions for businesses, and distortions in debt financing if owners and lenders have different tax rates. Thus, while the tax system has come a long way, removing or reducing the six distortions we have identified will require further reform.

Authors

-

Acknowledgements and disclosures

The authors thank Alex Brill for helpful comments; Swati Joshi, Samuel Thorpe, Aatman Vakil, and Semra Vignaux for outstanding research assistance; and Arnold Ventures and California Community Foundation for financial support.

The Brookings Institution is financed through the support of a diverse array of foundations, corporations, governments, individuals, as well as an endowment. A list of donors can be found in our annual reports published online here. The findings, interpretations, and conclusions in this report are solely those of its author(s) and are not influenced by any donation.

-

Footnotes

- Net factor income is equal to gross domestic income minus the consumption of fixed capital, taxes, and subsidies.

- The CIT’s progressive tax schedule could distort the ownership of capital assets. Business owners who face lower marginal tax rates benefit from a lower ETR on their assets than those held by business owners who face higher marginal tax rates.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).