Millions of households are saving for retirement through index funds. Yet, two investors holding identical portfolios can accumulate different after-tax wealth depending only on whether they invest through a mutual fund or an exchange-traded fund (ETF).

This difference does not reflect risk, return, or investment skill. It reflects how and when the tax code requires gains to be recognized.

As we describe in new work, ETF investors typically only owe taxes when they choose to sell their shares. Mutual fund investors, by contrast, can also owe taxes even if they do not sell—for example, when other investors’ redemptions lead the fund to realize and distribute capital gains. As a result, mutual fund investors may be taxed before they realize gains themselves.

Earlier taxation reduces the capital that remains invested and able to compound, while deferring realization allows returns to accrue on a larger base for longer. These differences reflect a structural disparity in the tax code: Economically similar investments generate different after-tax returns solely because of their legal form. This raises a central policy question: Should capital gains taxation be tied to transactions within a fund, or instead to investors’ own decisions to sell?

A tax externality changes how mutual fund investors realize capital gains

In mutual funds, one investor’s redemption can trigger taxes for others. Investors transact directly with the fund, and the fund typically satisfies redemptions by selling assets to generate cash. If those assets have appreciated, the sale realizes capital gains that must be distributed to remaining shareholders. As a result, investors can incur tax liabilities based on other investors’ decisions rather than their own.

ETFs largely avoid this dynamic. Most ETF shares trade on an exchange between investors, so the fund does not need to sell assets when ownership changes. Moreover, when large redemptions occur, they are typically handled through in-kind transactions in which the fund transfers securities rather than selling them. Because these transactions do not trigger capital gains under section 852(b)(6) of the Internal Revenue Code, one investor’s exit does not generally impose tax liabilities on others.

As a result, mutual fund investors may owe taxes without selling their shares, while ETF investors generally control when gains are realized. This difference in control over timing is the source of the externality.

Ownership patterns shape who benefits from deferral

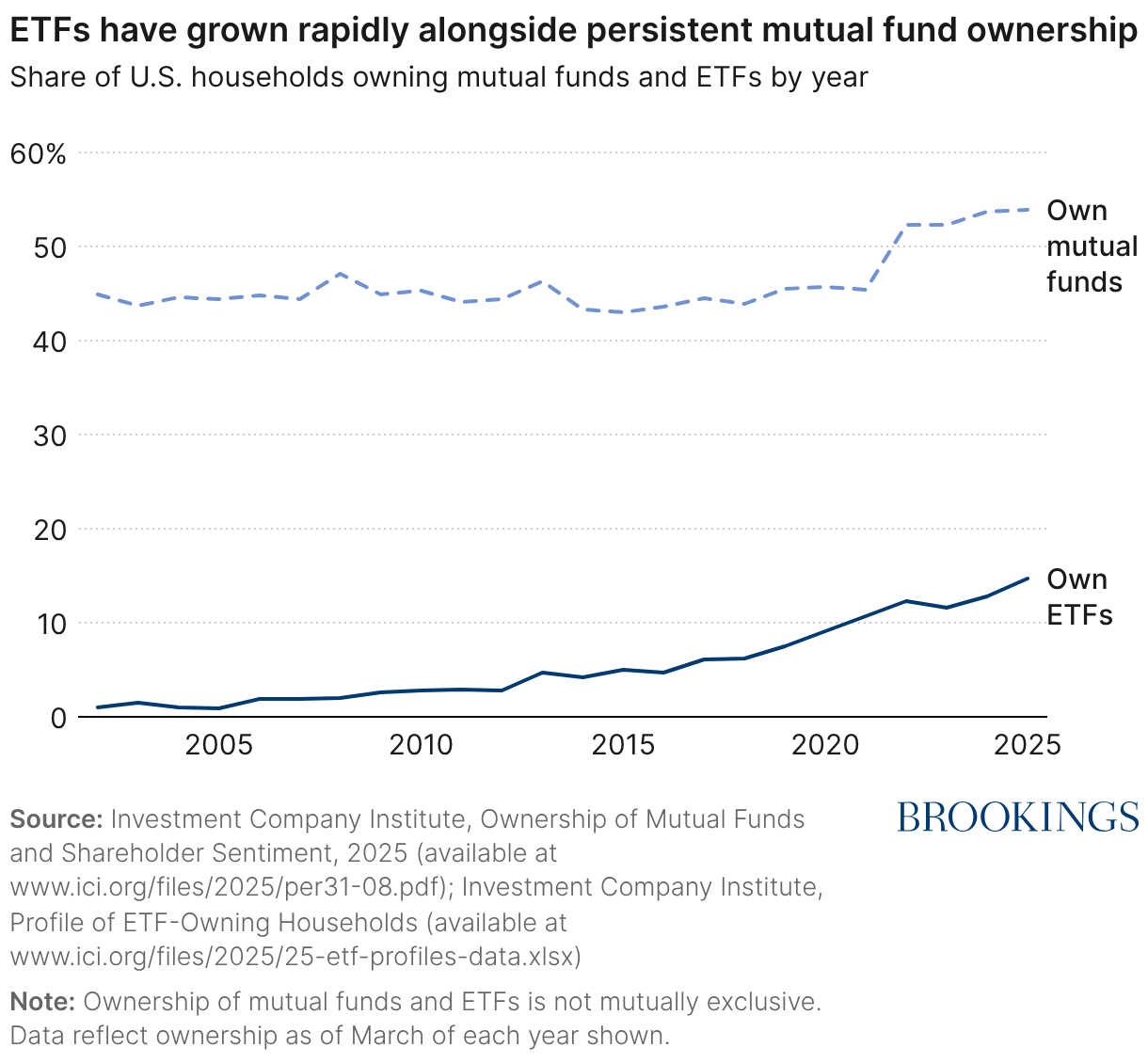

ETF ownership has increased from near zero to roughly 15% of households over the past two decades, while mutual fund ownership has remained broadly stable (Figure 1). This growth means that the tax advantages associated with ETFs apply to a steadily expanding share of household financial wealth.

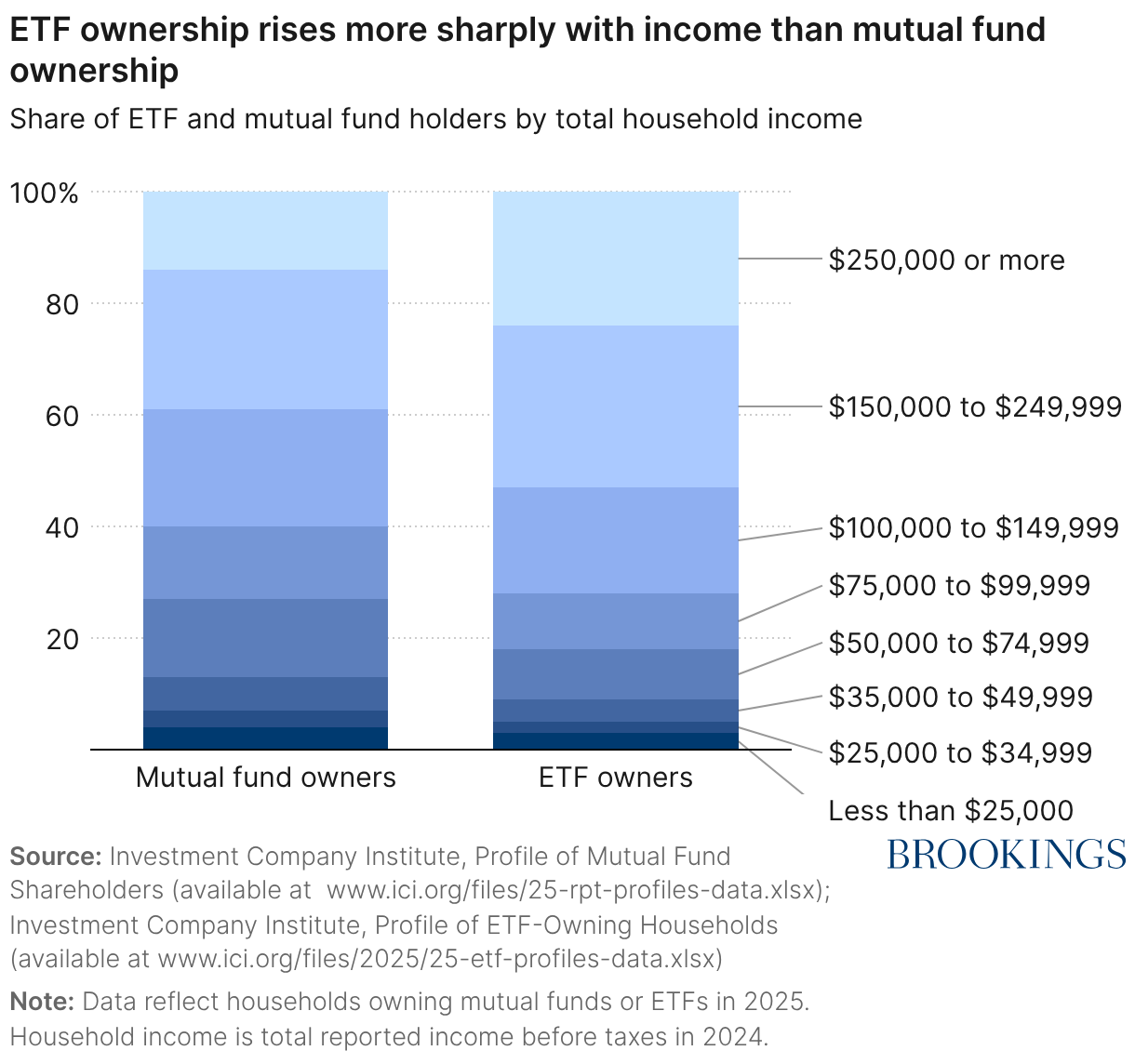

As shown in Figure 2, ETF ownership rises more sharply with income than mutual fund ownership. Because the value of capital gains deferral rises with portfolio size and investment horizon, this pattern implies that the tax advantages associated with ETFs accrue disproportionately to higher-income households. These structural timing differences affect a widening share of household financial wealth.

Reform options point in different directions

Policymakers can eliminate differences in tax timing across fund structures, but doing so requires choosing how capital gains should be recognized—either at the fund level or when investors choose to sell.

One approach would extend forced realization to ETFs, in effect ensuring they are taxed like mutual funds. Repealing the rule that allows in-kind redemptions under Internal Revenue Code section 852(b)(6) would require ETFs to recognize gains whenever appreciated assets leave the portfolio. Capital gains recognition would then be tied more closely to portfolio-level transactions, and revenue would generally be collected earlier. However, treating these transactions as taxable events could alter how ETFs function in practice because in-kind redemptions play a central role in ETF liquidity and price alignment.

An alternative approach would remove forced realization from mutual funds so they are taxed more like ETFs. Deferring capital gains taxation until investors sell their shares would allow realized gains to accrue without annual distribution. Instead, investors would be taxed when they exit the fund. Capital gains recognition would then align more closely with investor-level realization decisions, though revenue would be collected later.

The taxation of index funds reflects a structural design choice

The taxation of index funds turns on a fundamental policy choice: Should capital gains be recognized based on transactions within a fund or on investors’ own decisions to sell? Under current law, otherwise identical portfolios can generate different after-tax outcomes depending on how gains are realized and distributed.

As index investing continues to expand, these rules apply to a growing share of household wealth and increasingly shape how returns compound. Because ETF ownership is more concentrated among higher-income households, these differences also have distributional consequences that extend beyond individual investment choices.

The choice is not simply whether to equalize tax treatment, but what should trigger taxation in the first place. Tying taxation to fund-level transactions reduces investors’ control over when gains are realized and leads to earlier revenue collection, while deferring taxation until sale places that decision directly in the hands of investors. With the continued growth of index investing, that design choice will increasingly shape how households accumulate wealth and when the government collects revenue.

Authors

Related Content

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Taxing index funds: Tax timing, investor control, and household wealth

Structural differences in the taxation of ETFs and mutual funds affect investor control, compounding, and after-tax wealth

May 21, 2026