What are the current challenges and trends in the U.S. defense industrial base? What policy options and actions should be considered to strengthen it? These questions have become acute in recent years and should be major defense priorities for the next president.

The United States has, in broad brush, never had a clear strategy for maintaining a strong defense industrial base. In World War I, it entered the conflict late and mobilized quickly but had to fight largely with European-manufactured equipment. By World War II, it had become the world’s preeminent technological and industrial power and also had the “head start” of providing weapons to Britain and the Soviet Union through the Lend-Lease program before entering the war itself. Its manufacturers ultimately dominated the world’s production of weaponry and had much to do with the Allies’ ultimate success. But this was a unique moment of American manufacturing dominance. Throughout the Cold War, the United States consistently spent enough money on its military (usually 5% to 10% percent of GDP) that a strong defense industrial base could be sustained even without any particular government strategy for how to ensure it. The private sector was largely expected to take care of itself, without Uncle Sam picking favorites or winners (though, in practice, the military’s favored areas of technology enjoyed the natural benefit of federal largesse).

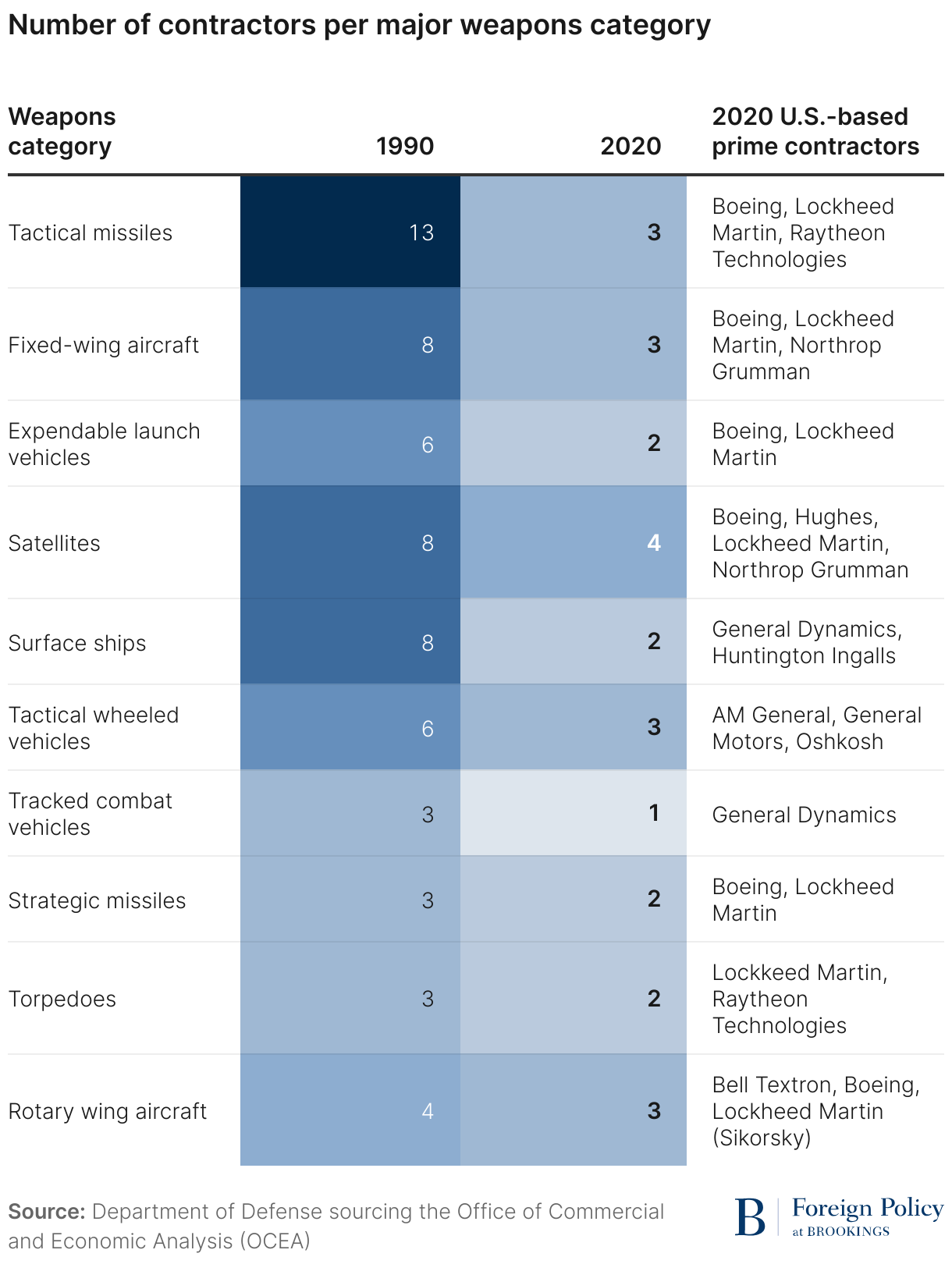

Then, the Cold War ended, and U.S. defense spending headed downward toward roughly 3% percent of GDP. But the government still maintained a largely hands-off and minimalist approach to defense industrial policy. In a famous meeting dubbed “the last supper” by observers at the time, in 1993, then-Deputy Secretary of Defense William Perry asked the defense industry to consolidate and streamline itself, since there would no longer be enough dollars to sustain many key existing companies. Yet the government would not offer advice on how industry should do so, or even try to direct the process to ensure that critical shortages, gaps, or bottlenecks did not develop. As a result of these trends, the nation soon confronted a situation in which it became possible that there might be only one major producer (and developer) of key areas of defense technology. The subcontractor ecosystem became fragile, with the Department of Defense (DOD) often unaware of the most critical points of vulnerability. This fragility threatened the supply of key inputs for major weapons systems. Meanwhile, the complexity of working with the government—paperwork, regulations, and disagreements over ownership of intellectual property—often discouraged new entrants into the defense acquisition ecosystem (including very innovative companies in the digital domains), a problem that has been only partially mitigated in more recent times. The below table indicates the decline in the number of suppliers for major weapon categories over the past 20 years.

In a report published in 2022, the Department of Defense argued, “Since the 1990s, the defense sector has consolidated substantially, transitioning from 51 to 5 aerospace and defense prime contractors.” It is not clear that defense budget cuts caused any such problem. Even in lean times, post-1990 defense budgets remained typically three-quarters of the Cold War average. Indeed, today, U.S. national defense spending exceeds that of any year during the Cold War even after adjusting for inflation.

Still, there are worrisome trends. In recent years, with concerns about China’s domination of key technology sectors, the supply-chain disruptions witnessed during the heart of the COVID-19 crisis, and the difficulty of ramping up production of key weapons as seen in the war in Ukraine, the U.S. strategic community has begun to settle on a new consensus. That is, having the world’s best weapons is not an American birthright, but a crucial end-state that needs to be earned and protected rather than assumed. Relatedly, the government may need to take explicit actions previously considered unacceptable by free-market purists to achieve that crucial outcome. Before raising questions and options for a future president, Congress, and DOD to consider, this policy backgrounder first provides some information on how the Pentagon buys weaponry today.

The ABCs of Department of Defense acquisition

As Mackenzie Eaglen of the American Enterprise Institute has said, America has two sacred vows with the men and women of its armed forces: that it will always take care of them and their families, and that it will always send them into battle with the best equipment in the world. The second vow is no less important than the first. How does the Pentagon pursue that goal?

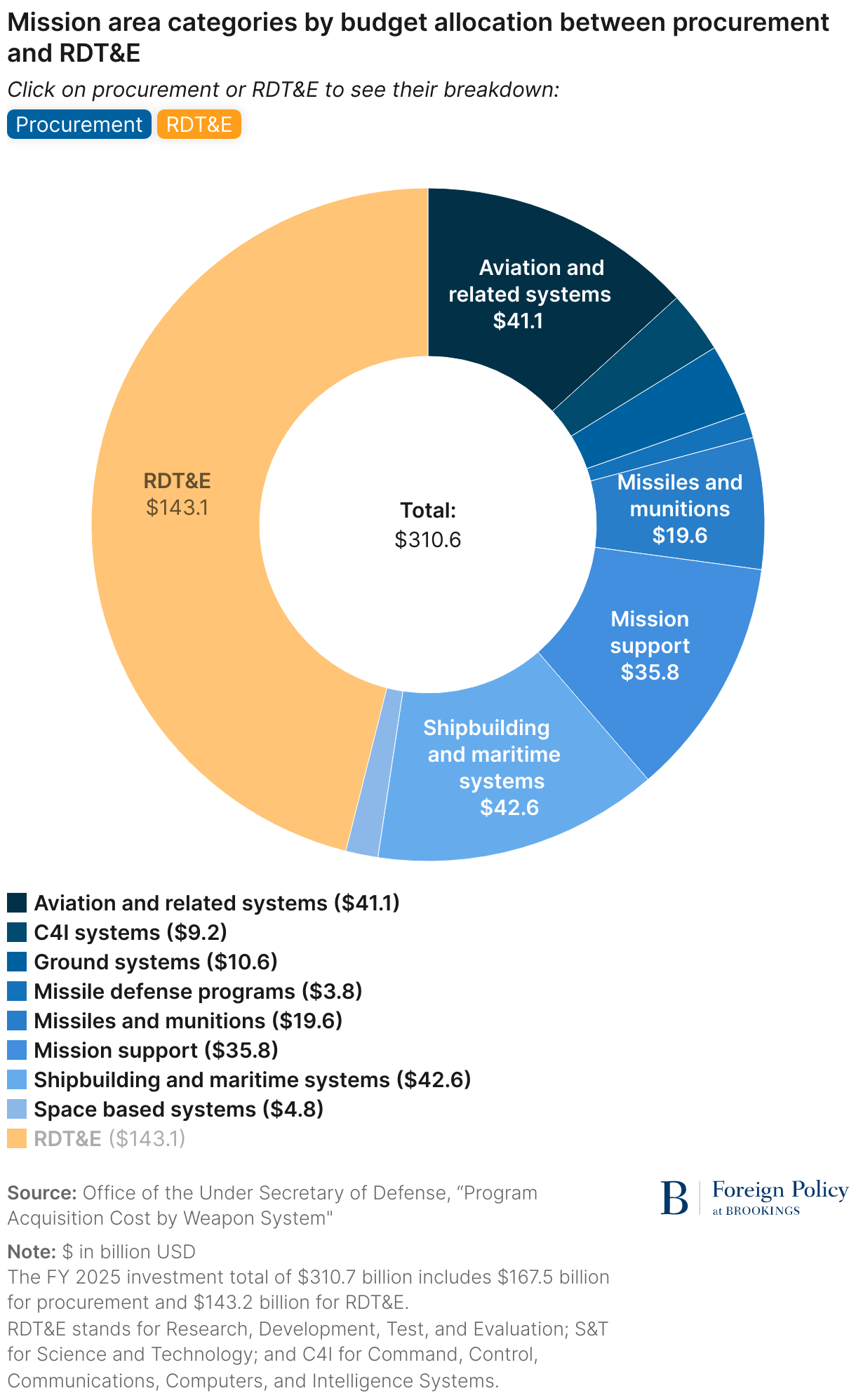

Roughly one-third of the DOD budget is usually devoted to the acquisition of equipment; today, the total exceeds $310 billion. Acquisition includes the research, development, testing, and evaluation (RDT&E) of equipment as well as the actual production process (or procurement). An entire set of organizations and cultures is involved in this effort, including government agencies, defense contractors big and small, federal as well as university research laboratories, and other players. Key elements of each of the military departments, like “NAVAIR” (Naval Air Systems Command) and “NAVSEA” (Naval Sea Systems Command), provide oversight and liaison with industry as well as the DOD laboratory and testing system, for their respective fields of specialization.

The United States does not have a major government-owned system for building armaments—though it does have a depot system that can help maintain them and also build certain niche capabilities. Weapons are generally produced by private defense firms, starting with the “big five” of Lockheed Martin, Boeing, General Dynamics, RTX (formerly Raytheon as well as United Technologies/Pratt & Whitney), and Northrop Grumman. These prime contractors each typically receive $10 billion a year or more in DOD business. Other major players, usually receiving several billion dollars each, include L3Harris Technologies, BAE Systems, Huntington Ingalls Industries, and Humana, among others.1 There are also more than 12,000 small and medium-sized firms that operate as subcontractors to the primes—and whose capacities, sometimes even whose identities, are not well known to the DOD. Of all the dollars spent on acquisition, more than 90% are awarded after a competitive bidding process. Contractors also perform many support functions for DOD outside of the acquisition process. All told, more than half of all defense dollars are spent through contracts with private companies.

The Pentagon does business with these companies through various financial mechanisms that it consistently seeks to adjust and improve. Harvey Sapolsky, Eugene Gholz, and Caitlin Talmadge describe the various tools as “all the imperfect types of contracts,” underscoring that each major type has its advantages and disadvantages.2 It is often difficult to agree to a fixed-price contract, where the contract sets a price that will not change for the project’s duration, for technology that is still being developed when contracts are negotiated. Usually, some method is needed to account for uncertainty and unexpected costs or complications—lest even a well-intentioned and competent company that encounters difficulties in developing new technologies be punished or even driven out of business by a contract that pays it too little. A number of approaches have been attempted and depending on the ripeness of a given type of technology, one or another may be invoked for a given purchase. Cost-plus-percentage contracts (CPPC), for instance, reimburse a contractor for all documented expenses and then add a profit margin of some set percentage on top of that. But because CPPCs incentivize companies to build more expensive weapons (profit is a percentage of total costs), this type of contract can lead to “gold plating,” or adding extra features to weapons beyond their original scope. To mitigate this, other approaches have been developed too, including the cost-plus-fixed-fee (CPFF) contract and the cost-plus-incentive-fee (CPIF) contract. A CPFF contract is self-explanatory—it is an agreement in which the contractor is paid for all costs plus a fixed fee negotiated at the contract’s inception. This is often a good contractual vehicle for well-established technology. A CPIF contract ties a contractor’s profit to achieving less costly weapons. In other words, with such a contract, the company makes more money if the cost goes down, the exact opposite of the incentive system used with the cost-plus-percentage method.3

Although the private sector builds weapons, the DOD directs and supervises the process. Most of this is done through the individual military services. At various stages, decisions are informed by inputs from other DOD entities, such as the offices of Cost Assessment and Program Evaluation (CAPE) and Operational Test and Evaluation (OTE). The Office of the Secretary of Defense and the chairman and vice chairman of the Joint Chiefs of Staff (together with their joint staffs) have roles as well. Programs with multiple service implications are prioritized and coordinated through the Joint Requirements Oversight Council, run by the vice chairman of the Joint Chiefs of Staff. The Government Accountability Office often provides an independent set of eyes from the Capitol Hill side of town; the Congressional Budget Office helps Congress develop possible alternatives for acquiring weapons in situations where options besides the Pentagon’s preferred ideas may seem desirable. For large programs, the under secretary of defense for acquisition and sustainment plays a role as well.

Programs run through what are called Milestones A, B, and C. The first milestone authorizes moving a program into what is called the technology maturation and risk reduction phase, the second into full-bore engineering and manufacturing development, and the third into production and deployment. The process is complex, and the players are numerous—largely because the process must simultaneously develop new weaponry so that America’s military remains the best-armed in the world while doing so affordably and without gold-plating, corruption, or wasting taxpayer dollars. These goals can of course be in tension with each other.4

In recent years, the DOD has sought to encourage new entrants into the defense acquisition space to broaden the industrial base and bring more new ideas and inventions into the American armed forces. It has also encouraged greater use of commercial technologies when readily available. To facilitate these processes, DOD has sought to make it easier to apply for department grants and created offices and outreach programs to assist companies in the application process. In some cases, where subcontractor capabilities are lacking and bottlenecks risk disrupting access to key weaponry, it has even offered direct subsidies to firms under the Defense Production Act (spending roughly $900 million during the Biden administration). Of late, DOD has also sought to provide greater oversight and support to five key domains of manufacturing: castings and forgings, missiles and munitions, energy storage and batteries, strategic and critical materials, and microelectronics. Furthermore, Australia has provided direct cash assistance to help American submarine makers expand their capacity under the Australia-United Kingdom-United States or “AUKUS” arrangement of 2021.

Options for the future

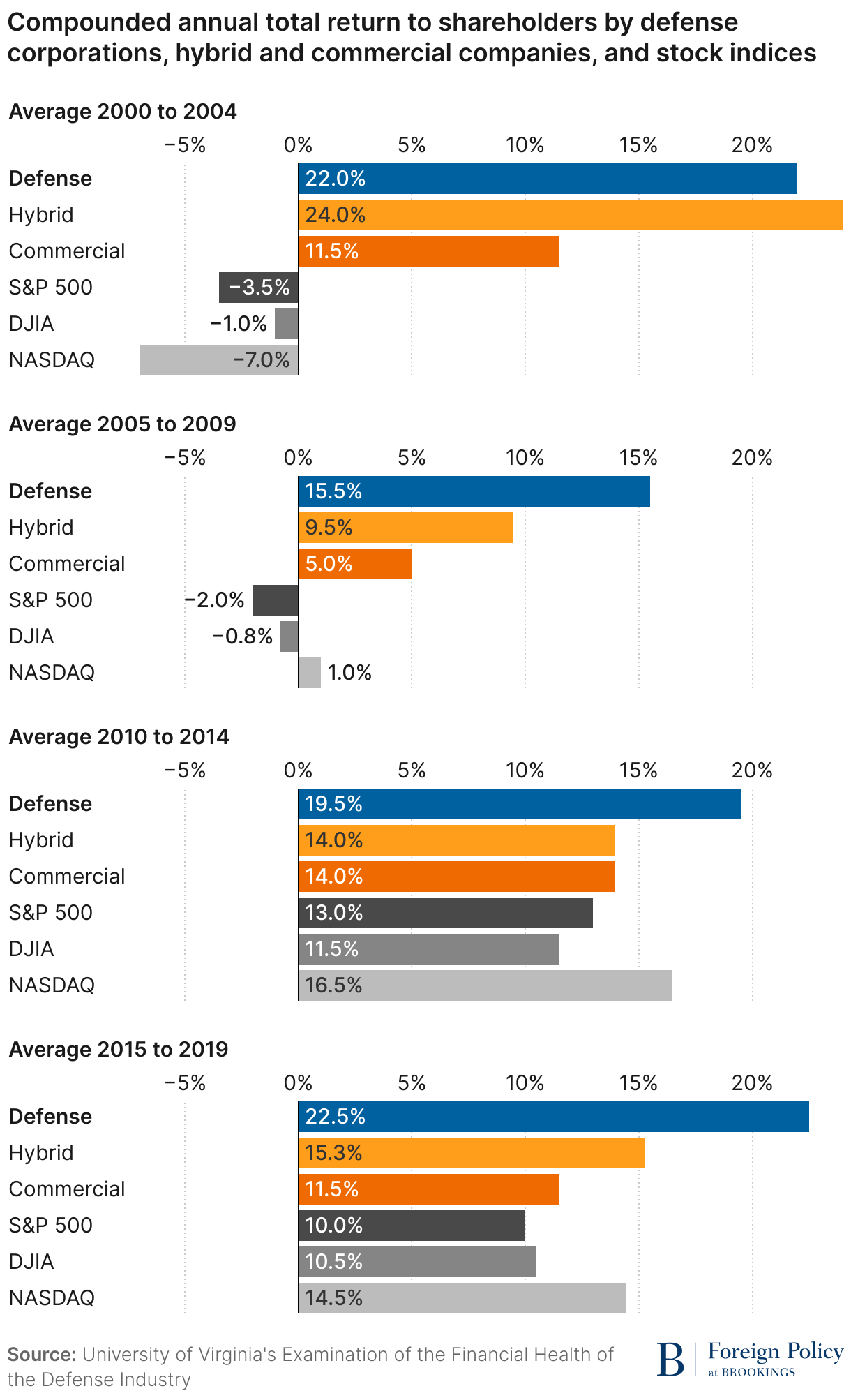

For perspective, it bears noting that, contrary to popular thinking, there is no general crisis in the American defense industrial base today. New technologies are making their way into warfighters’ hands. America has dramatically ramped up artillery production in response to the war in Ukraine, a case in point of how it might do so in other areas as well. Defense companies do not always make big profits, but major American and allied defense firms are certainly not going out of business. In fact, the University of Virginia’s Darden School of Business conducted a study on the financial health of the defense industry and found that overall, the industry is financially healthy and has shown improvement over time. The study examined 124 publicly traded U.S. firms, categorized into defense, hybrid, and commercial firms. Defense firms were defined as those that derived 75% or more of their annual revenue from U.S. defense or foreign military sales customers; hybrid firms as those that derived 25% to 75% of their revenue from U.S. defense or foreign military sales customers; and commercial firms as those that derived less than 25% of their revenue from U.S. defense or foreign military sales customers. The graph below compares the defense firms’ performance against that of hybrid and commercial firms and market indexes over five-year periods. All in all, defense corporations outperform hybrid and commercial companies as well as the S&P 500, Dow Jones Industrial Average, and NASDAQ stock indices.

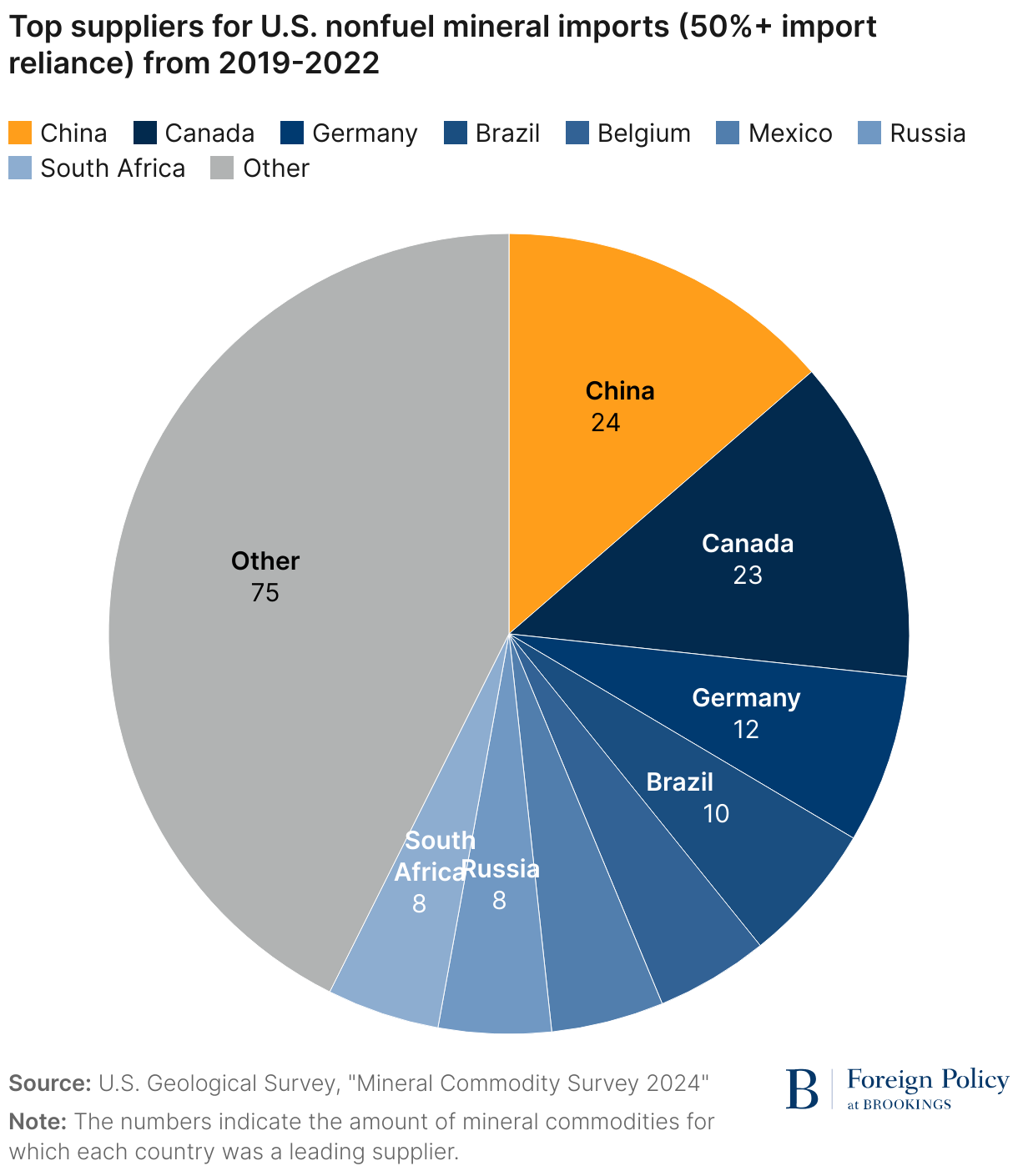

Yet not all is well. The defense industry faces a shortage of skilled workers needed to meet production demands. Artillery is simpler to produce than advanced modern weapons. Certain subcontractor bases are weak. Surge capacity is limited, and bottlenecks, sometimes hidden ones, could seriously constrict the nation’s ability to build lots more weapons quickly in a time of conflict. Physical infrastructure has degraded over time. The United States retains dependencies on certain commodities, raw materials, and intermediate goods that come from nations or regions where access may not be secure during conflict. In fact, from 2019 to 2022, imports accounted for over half of the U.S. apparent consumption for 49 nonfuel mineral commodities, with the United States being 100% import reliant for 15 of them. The figure below shows countries that the United States was over 50% import reliant on for nonfuel mineral commodities. China was the top supplier, providing 24 of these commodities.

Thus, several options for strengthening America’s defense industrial base may be worthy of serious consideration:

- Directly incentivizing or even funding companies to develop spare production capacity and thus accommodate increased demand is key. The scale of the effort to date is quite modest. The Pentagon has only spent $1 billion on such concerns during the Biden years—even as Australia has itself committed to spend $3 billion just on the U.S. submarine shipbuilding sector. That case suggests the United States may need to spend several billion dollars more on a broader effort across a wider swath of the nation’s defense industrial base.

- Expanding the nation’s stockpiles of critical minerals and other inputs to manufacturing, now reduced by about 90% from Cold War norms (and from estimated needs, including for vital domestic infrastructure), may be wise. Today’s list of commodities may be somewhat different than those of earlier eras.

- Closer collaboration with allies needs to be undertaken, such that international capacity can grow in general—sometimes meaning that the United States will not have to ensure resiliency and redundancy in key materials and components all by itself. Again, the AUKUS example is instructive, as a microcosm or initial example of a broader effort.

- Efforts to encourage more entrants into the defense acquisition world must not slow; they are only really beginning to show major results.

- The resilience of the nation’s defense industrial base infrastructure should be treated as a top-tier national security threat, with resources provided to make cyber systems more survivable and to reduce physical vulnerabilities in electricity, energy, transportation, health, and other crucial sectors.

-

DOD should think bigger about developing the future workforce—given that shortfalls into the many tens of thousands of workers are already foreseeable. DOD’s 2023 National Defense Industrial Strategy expresses some of the right sentiments but does not back them up clearly and consistently with concrete programs or with dollars. Consider this language from that report:

“The Department will look for opportunities to assist companies with upskilling and reskilling workers to help better meet national security needs. By providing incentives to companies that do so, the Department can increase the number of enterprises that invest in employee education and thereby prepare them for future technological innovation.” It may be time, however, to move beyond just “looking for opportunities” (and increasing internships and apprenticeships—as the same strategy document proposes) to offer direct financial incentives to individuals who learn relevant skills. If the nation can consider forgiving college debt on a sweeping scale, it can do just as much to help those who wish to pursue manufacturing and engineering careers within the defense industrial base.

In the broadest sense, it seems safe to say that a laissez-faire attitude on the part of the U.S. government toward America’s defense industrial base is no longer enough. The latter is not in fundamental jeopardy, but it has numerous weak points. Its ability to produce high-end weapons and to do so quickly and reliably is not a given. America’s defense industrial base is much more advanced in most ways than was the “arsenal of democracy” in World War II, but it also has challenges and limitations that this nation’s manufacturing base in the 1940s did not—and they are not self-healing by the hidden hand of Adam Smith’s free market or anyone else. Addressing these vulnerabilities and limitations needs to be front and center in future military policymaking and budgeting.

Authors

Related Content

-

Footnotes

- See Michael E. O’Hanlon, Defense 101: Understanding the Military of Today and Tomorrow (Ithaca, NY: Cornell University Press, 2021), 56-58.

- Harvey M. Sapolsky, Eugene Gholz, and Caitlin Talmadge, U.S. Defense Politics: The Origins of Security Policy, third edition (New York: Routledge, 2017), 140-157.

- Ibid.

- Michael E. O’Hanlon, Defense 101, 56-58.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Strengthening America’s defense industrial base

June 20, 2024