Executive summary

In June 2023, U.S. President Joe Biden, Speaker Kevin McCarthy, and the rest of Congress managed to reach a budget deal and evade an unprecedented government default on its financial obligations. But in that deal, U.S. defense spending remains a contentious matter. It was treated more gently than domestic “discretionary” spending (which is effectively frozen in nominal terms by the deal and will thus be eroded by inflation over the next two years—indeed, as of this writing, the possibility exists that it could be cut even more severely). Yet defense budgets could still suffer modest declines in real spending power of perhaps 1–2% a year, depending on the inflation rate and choices of Congress. At a time of considerable international peril, is this wise?

Clearly, any serious plan for fiscal prudence and good U.S. economic health needs to address the growth of entitlement spending, which accounts for nearly two-thirds of the almost $7 trillion federal budget being proposed for 2024. There are ways to reform entitlements without cutting real dollar benefits for most beneficiaries per se — for example, by curbing rates of growth, using different adjustments for inflation, or asking more of higher-income earners in one way or another. But none of that will apparently happen anytime soon. Meanwhile, a large deficit and debt, as well as underfunded domestic investments in areas such as science, technology, education, and infrastructure, could weaken the U.S. economy and thus the economic foundations of U.S. security over the longer term. These considerations call for some degree of shared sacrifice across the whole government, including the Pentagon.1

To balance these various realities, the most sensible path forward is to provide very modest real growth in the defense budget — about 1% a year above inflation for the next two years and perhaps beyond. For the current year, with inflation running up to 4%, that implies a 5% increase in nominal terms from 2023 to 2024. By contrast, the Biden budget request for 2024 implies zero real growth or even a 1% real cut in base defense dollars (leaving supplementals for Ukraine and other potential needs out of the respective tallies for each year). In other words, the 2024 base budget would increase by about 3% relative to 2023, which could be slightly less than the inflation rate.

In broad terms, real growth of about 1% constitutes a compromise of sorts. It is less than what recent independent commissions and many scholars have advocated when calling for sustained increases of 3–5% a year above the rate of inflation.2 It would also see defense spending decline slightly as a percent of GDP over time. But it is more than a nominal or real freeze, more than what is being proposed for domestic discretionary accounts, and more than what is in the Biden proposal for 2024. It also gives the Pentagon some room for new initiatives, provided that the Pentagon curtails its overall appetite while instituting additional reforms. Moreover, it signals to the world that America is not pulling back or shirking its sense of global duty.

Given the Congressional Budget Office’s (CBO) calculations that national defense budgets might need to grow 1% a year in real terms over the next decade to fund the Pentagon’s current plans, such a funding path should roughly suffice for what the Pentagon now proposes by way of force structure, pay, readiness, and modernization. However, perhaps not every aspect of those plans should be endorsed and, instead, new initiatives such as those proposed in this paper should be considered. The net effect of the proposed increases and new additional cuts that I identify here would be roughly zero. In other words, in budget terms, the increases and cuts would balance each other out. By tightening collective belts and making tough choices, the DOD could get by with 1% real growth and still have some money for new and worthy plans.

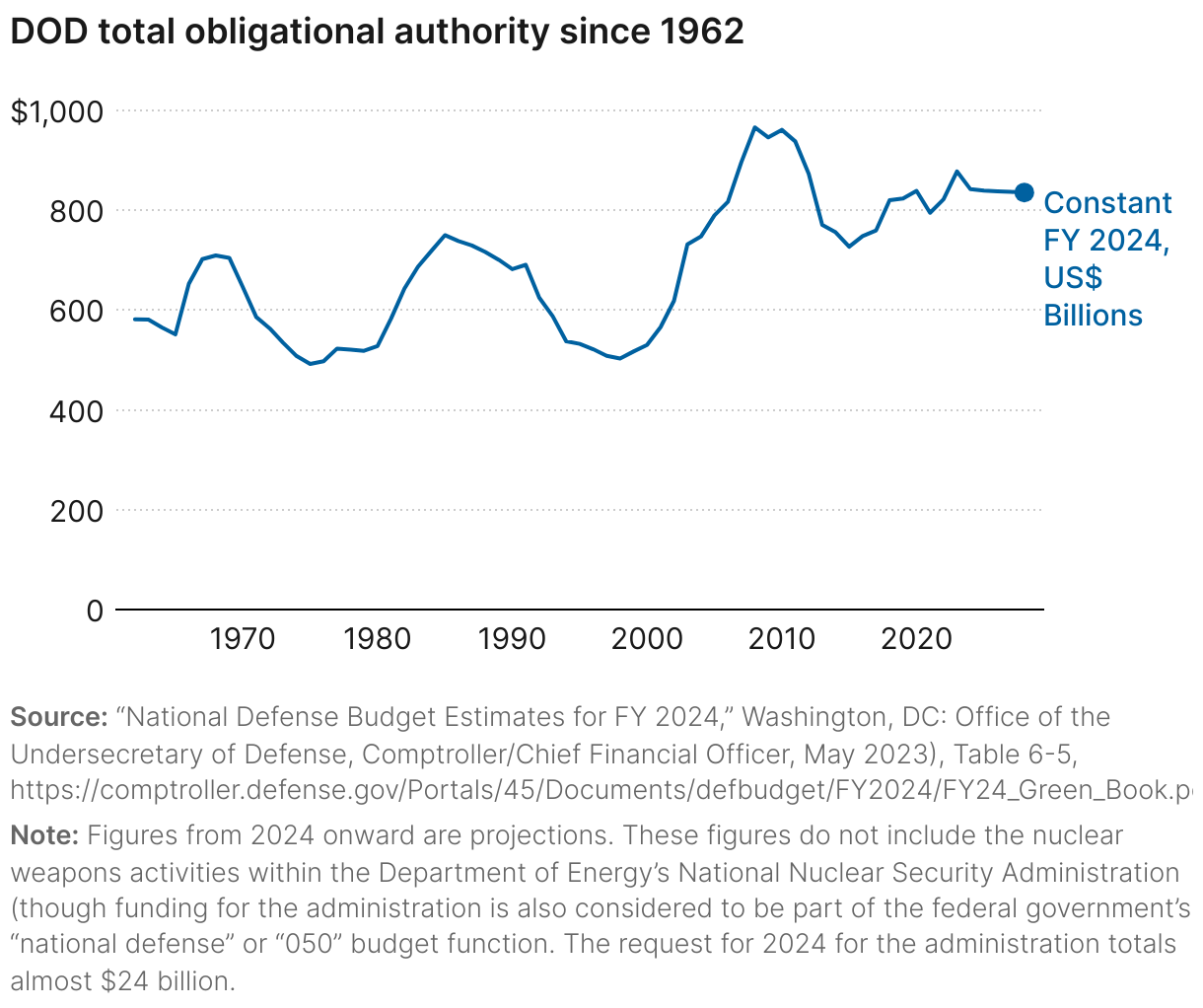

With this approach, the national defense budget would initially remain near its current level of 3.3% of the country’s gross domestic product (GDP) — around half of the level it was during the Cold War. At just under $900 billion each for the next two years, including Department of Energy nuclear weapons costs, it would continue to exceed even peak levels of Cold War spending in real or absolute dollar terms (that is, adjusted for inflation). It would, however, remain about 10% less than peak levels during the George W. Bush and early Barack Obama presidencies. It would continue to be about three times China’s estimated spending and many times that of Russia’s.

To paraphrase former House speaker Newt Gingrich as he put it back in the 1990s, this paper argues that we should be “cheap hawks.” Cheap should be understood to mean limiting the rate of Pentagon budgetary growth, not actually cutting it, especially at this juncture when the world is significantly more dangerous than when Gingrich coined his memorable phrase.

Author

Related Content

Related Books

-

Acknowledgements and disclosures

The author would like to thank Alejandra Rocha for research assistance and Rachel Slattery for design and layout. The author would also like to thank Caitlin Talmadge, Melanie Sisson, Bruce Jones, other members of the Brookings Talbott Center and Foreign Policy program, Sara Chiaravalle, and anonymous reviewers for their constructive suggestions and collegial assistance, as well as Suzanne Maloney for leadership of the Foreign Policy program.

-

Footnotes

- See “How Would You Fix the Budget?,” (Washington, DC: Committee for a Responsible Federal Budget, 2022), https://www.futurebudget.org; Alice M. Rivlin, Sheri Rivlin, and Allan Rivlin, Divided We Fall: Why Consensus Matters (Washington, DC: Brookings Institution Press, 2022); William Gale, Fiscal Therapy: Curing America’s Debt Addiction and Investing in the Future (Oxford: Oxford University Press, 2019).

- National Defense Strategy Commission, “Providing for the Common Defense,’ U.S. Institute of Peace, Washington, D.C., November 2018, p. xii, https://www.usip.org/publications/2018/11/providing-common-defense.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).