This chapter is part of USMCA Forward 2025, which focuses on areas where deepening cooperation between the United States, Mexico, and Canada can help advance key economic and national security goals.

In 2026 the U.S., Mexico, and Canada will undertake an unprecedented review process through which they will decide whether to extend the United States-Mexico-Canada Agreement (USMCA), which went into effect in 2020. The automotive industry is deeply integrated across the three USMCA countries and is a driver of trade and jobs. However, the auto industry has faced many challenges since USMCA came into effect, including a global pandemic and a semiconductor shortage crisis. The industry is also navigating a rapid shift from internal combustion engine (ICE) toward electric vehicles (EVs). EVs are not only a key lever to decarbonize the way we move people and goods, they also represent a major economic opportunity. With countries around the world enacting EV policies and companies pushing the boundaries of innovation to compete in this space, the EV global market size is projected to grow from $437.62 billion in 2024 to $1.1 trillion by 2032. Recognizing this opportunity, players around the world have moved swiftly and decisively to lead the EV transition. As the three governments gear up for review of the USMCA in 2026, a key focus will be on how USMCA supports the auto industry and what more might be needed to enable a more competitive auto sector as it transitions to EVs.

As the three governments gear up for review of the USMCA in 2026, a key focus will be on how USMCA supports the auto industry and what more might be needed to enable a more competitive auto sector as it transitions to electric vehicles.

A highly integrated supply chain … in transition

The role of the North American Free Trade Agreement (NAFTA) and then USMCA in supporting the integration of the automotive supply chain across the region is widely recognized. Building vehicles in North America necessitates multiple border crossings that are perfectly orchestrated to ensure maximum efficiency and involves an integrated supply chain that has been honed over decades. Ford’s CEO Jim Farley explained the just-in-time approach: If there is a problem on the Ambassador Bridge between Detroit and Windsor, Ford will run out of seats from its supplier in Canada to produce the F-150 in Detroit within an hour. Having an integrated supply chain for manufacturing automobiles means that much of the auto content that comes from Canada and Mexico contains high levels of U.S. value added. According to one estimate, vehicles built in Canada have an average of 50% of content from the U.S., and those assembled in Mexico had 35% of U.S. content. The U.S. International Trade Administration estimated that around half of Mexico’s imports of auto parts are from the U.S., and, after further processing, Mexico exported most of its finished auto parts (86.9%) back to the U.S.

New administrations in the U.S., Mexico, and Canada, a quest to decouple from and compete with China, and a push to develop domestic-first and regional-second supply chains to capture the EV opportunity, will be key factors driving decisionmaking for the three partners.

The benefits of this integration, and the areas that need improvement, will be part of the 2026 review process. In doing so, the three countries should consider how the transition to EVs is changing the rules of the game—and how USMCA could serve as a tool to help the three partners take on the electrification challenge more effectively.

State of play

In 2020, USMCA established more rigorous provisions specific to the automotive sector for goods to qualify for duty-free treatment to encourage increased investment in vehicles and automotive parts production (for both ICE vehicles and EVs) in North America. These included Rules of Origin requirements to promote increased regional value content and a new provision related to labor value content to support higher-paying jobs and make U.S. workers more competitive.1 The goal was clear: localize the supply chain as much as possible while ensuring that the economic benefits of this localization are shared by all three countries.

The transition to EVs has made the localization goal more difficult because it involves a substantial reconfiguration of the supply chain around batteries. Developing domestic battery production—along with EV production capacity via the retooling of ICE vehicle plants or by establishing new EV manufacturing plants—has therefore been the north star for the region the past few years. And these actions have borne fruit: Since USMCA came into effect, and thanks to policies and actions undertaken by the three partners, EV and battery-related investments in North America through late 2024 are estimated at $249.6 billion.2 Of these, 78% are in the U.S. ($195.9 billion), 20% in Canada ($46.9 billion), and approximately 3% in Mexico ($6.9 billion) (Figure 1). Still, substantial challenges remain: most of these investments will begin to come online between now and 2030, and lithium-ion battery production relies heavily on materials and components sourced from or processed in China.3 Efforts to reduce the dependency on China will continue and will require collective and decisive action.

|

United States |

Canada |

Mexico |

|

|---|---|---|---|

|

Electric vehicle production |

$54.2 |

$12.2 |

$6.2 |

|

Battery manufacturing |

$141.6 |

$34.7 |

$0.7 |

Source: Data from The Big Green Machine

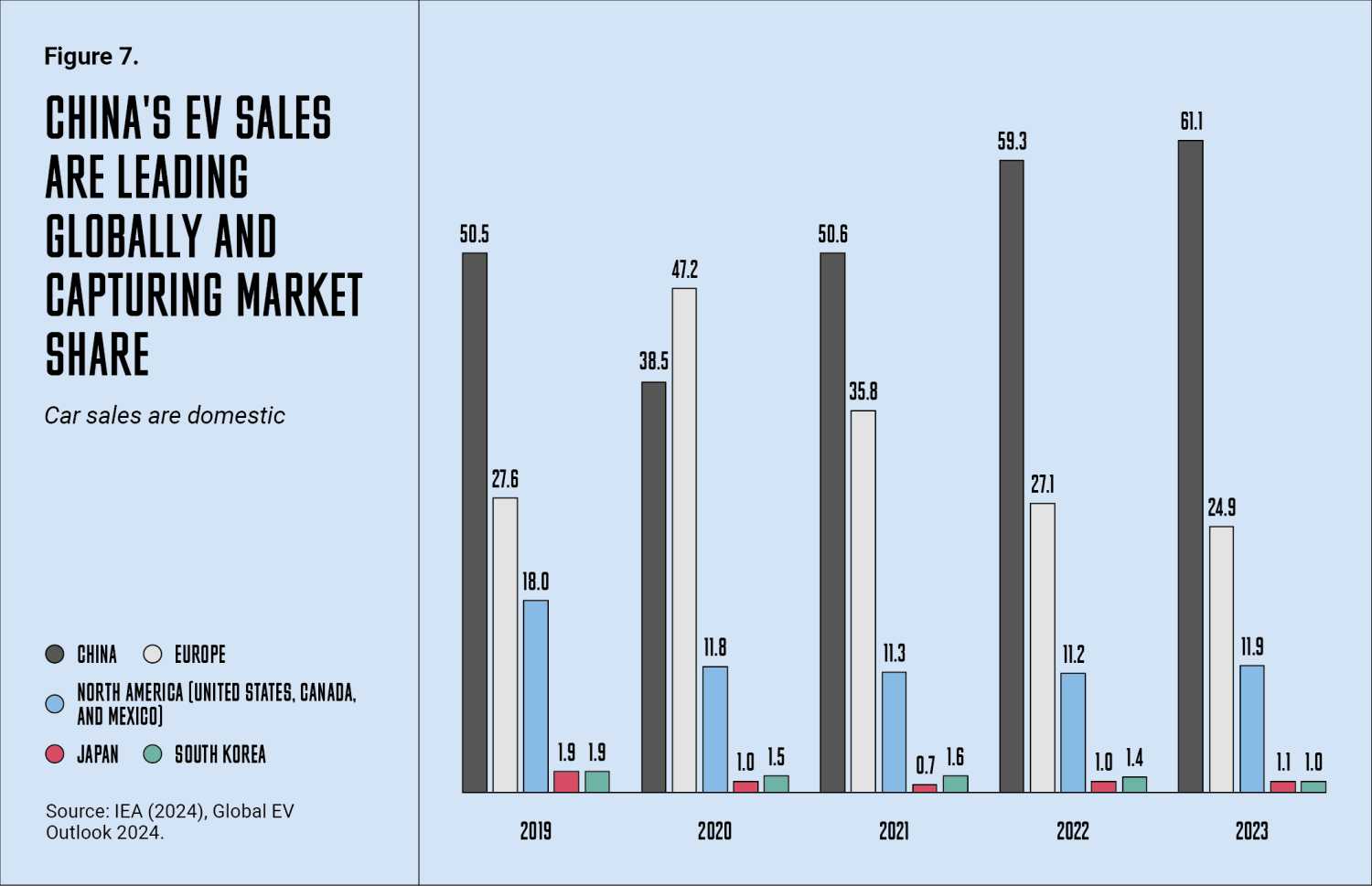

Indeed, China’s early EV leadership and swift expansion into global markets have become thorny issues, impacting each of the partners and their relationship in different ways. Guided by a top-down strategy to target high-growth industries and aided by substantial government subsidies and massive investments in R&D, Chinese companies dominate the EV transition today. China produces two-thirds of the world’s EVs, is responsible for 85% of global battery cell production, and controls the processing and refining of critical minerals. This concentration creates vulnerabilities and risks for the partners and highlights the need to diversify EV supply chains away from China, and fast. It also underscores the need to boost innovation and invest in next-gen battery technologies such as solid-state batteries to carve out competitive advantages in the longer term.

The 2026 review will take place at a delicate time for the region—and the world. New administrations in the U.S., Mexico, and Canada, a quest to decouple from and compete with China, and a push to develop domestic-first and regional-second supply chains to capture the EV opportunity, will be key factors driving decisionmaking for the three partners. In the lead-up to the review, what’s the state of play in each country?

United States

The U.S., the largest center of vehicle production and vehicle market in North America, is experiencing a clean energy manufacturing renaissance following the passage of the Inflation Reduction Act (IRA) in 2022. The IRA has led to over $110 billion in investments in the EV and battery sectors across the country, including many that will benefit Republican states. Among other provisions, the IRA provides tax credits for vehicles and battery components manufactured or assembled in North America, thereby extending some of the benefits related to EV production to Canada and Mexico and encouraging further integration of the supply chain. Other policy tools, such as the Bipartisan Infrastructure Law’s EV charging investment program and the Environmental Protection Agency’s tailpipe emissions standards have also helped accelerate industry action around the EV transition and position the U.S. better vis-à-vis competing with China. Any action aimed at undoing these policies poses significant risks to the progress made thus far and would harm U.S. manufacturing and trade. Sales of battery electric vehicles (BEVs) have increased overall and reached 8.9% market share in late 2024. But these sales were uneven, leading OEMs to hedge their bets and in some cases delay previously announced production of EV models. The lack of affordable models is a key hurdle to increased uptake: The average price paid for an EV in late 2024, at $57,000, is 19% higher than the industry-wide average transaction price. While efforts are underway, no U.S. automaker has yet been able to produce a sub-$30,000 EV, a price point considered crucial for mainstream adoption. Insufficient charging infrastructure to address the “range anxiety” issue and a negative public perception of EVs, given recent politicization, add to the challenges.

Mexico

Lower production costs, proximity to the U.S., and a large supplier base have made Mexico an automotive industry powerhouse. All “Big Three” companies produce EVs in Mexico: GM in Ramos Arizpe, Ford in Cuautitlán, and Stellantis in Toluca, with production expected to expand in 2025 and beyond. The vast majority of these vehicles are exported to the U.S. and other global markets. The nearshoring trend that seeks to relocate supply chains closer to the final consumer market to minimize disruptions has benefited Mexico as more companies establish operations in the country. The supplier ecosystem also continues to grow: There were at least 312 suppliers of EV parts and components in Mexico in Q2 2024, up from 172 in Q2 of 2023. There is momentum for Mexico to fully take advantage of this opportunity while finding ways to create more value add, including President Claudia Sheinbaum’s new national flagship EV project, Olinia. To do so, however, the country will need to address challenges related to infrastructure, the supply and reliability of electricity, and workforce readiness and availability—all while complying with labor and environmental provisions outlined in the USMCA. More broadly, the new Sheinbaum administration has implemented a series of sweeping reforms that are creating uncertainty and unpredictability, none of which are conducive to a thriving business environment. These reforms include the overhaul of Mexico’s judiciary, a measure to reinforce government participation over private investment in the energy sector, and the dissolution of independent regulators such as the Federal Economic Competition Commission (COFECE), the Energy Regulatory Commission (CRE), and the National Institute of Transparency, Access to Information and Data Protection (INAI), among others. Further complicating the picture, Chinese EV brands have entered the Mexican market in recent years, offering affordable, highly competitive products. BYD, the leading Chinese EV company, announced plans to open around 50 dealerships in the country by the end of 2024. The penetration of Chinese EV brands, coupled with BYD’s plans for setting up a plant in Mexico, are widely perceived in the U.S. as a move by Chinese companies to enter the U.S. market tariff-free by leveraging USMCA. To preempt this, the U.S. imposed 100% tariffs on all Chinese-made EVs as of September 27, 2024, and Canada also implemented a 100% tariff on Chinese EVs on October 1, 2024. Mexico, in turn, ended an exemption on the same date that had provided a 15%-20% reduction in import taxes for EVs from countries without free trade agreements since late 2020 and which had benefited Chinese companies. EVs are still a small part of the Mexican market at about 2.5% of total vehicle sales in mid-2024, but sales have grown considerably in the past year (over 50% growth on BEV sales in 2024 relative to 2023), a trend that is expected to continue.

Canada

Canada, for its part, is leveraging its substantial mineral reserves, abundant renewable electricity and strong ESG credentials to position itself as a leader in the battery supply chain. The availability of nickel, cobalt, copper, lithium, and rare earth elements—all critical for EV and battery production—means that Canada has enormous potential to be a key player in this sector. Canada’s 2022 Critical Minerals Strategy earmarked funding support to accelerate the development of the battery supply chain, and dedicated programs such as the Critical Minerals Research, Development, and Demonstration program are designed to support innovative processing technologies to advance Canadian mining projects toward production. The U.S. is also supporting this effort; The Department of Defense provided grants in the amount of $34.7 million to three Canadian companies involved in the cobalt and graphite supply chains in 2024. Still, more investment is needed, and long production timelines involved in developing mining and refining operations for critical minerals has put pressure on Canada to act. Canada has also seen some investments in EV production, largely concentrated in the province of Ontario, which borders Detroit and is connected to the Michigan automotive ecosystem. Driven by strong policy support and incentives since 2019, EV adoption is growing in Canada: Zero-emission vehicle market share, including BEVs and plug-in hybrids (PHEVs), was 13.4% in mid-2024.

The USMCA review: An opportunity for realignment

The actions taken and investments made across the U.S., Canada, and Mexico in the past few years have laid the foundations for North America in the EV transition. These investments across the EV and battery supply chain build on each country’s comparative strengths, with the U.S. leading EV production and R&D across the region, Mexico providing labor-intensive manufacturing capabilities and a strong and resilient auto parts supplier ecosystem, and Canada producing critical minerals that will help to onshore the battery supply chain.

There is too much at stake, and decisive action is needed to fully realize the potential of the investments made so far and ensure a place for North America in this competitive race.

The USMCA review is an opportunity to double-down on the importance of trade and investment across North America in the development of the EV supply chain and to recalibrate the region’s position in the EV race. In the lead-up to the USMCA review, the partners should consider three key opportunities:

- Establish a North American Automotive Dialogue or similar dedicated platform for the three governments to discuss the current state of play, barriers, and opportunities with industry stakeholders. The dialogues should be designed to develop concrete strategies for:

- Increasing competitiveness of North American companies and their products;

- Boosting innovation in the EV space, particularly by making bolder investments in next-gen EV and battery technologies and supporting promising startups; and

- Bolstering EV adoption across the three countries to grow the market for the vehicles made in North America.

- Design flagship projects or initiatives related to EV policy, infrastructure, or workforce that could be collaboratively implemented by the partners. Such projects can help signal the importance of competing in this transition and create new mechanisms for closer collaboration.

- On the policy front, the partners could consider further harmonization of relevant EV standards or regulations and increased support for technology transfer. The experience of the Association of Southeast Asian Nations (ASEAN) countries in this regard could be a helpful reference for USMCA partners.

- In terms of infrastructure, binational charging corridors such as the ones implemented between Michigan and Ontario or San Diego and Tijuana can be replicated in other border crossings to facilitate EV uptake and leverage existing integration.

- Reskilling the current automotive workforce and developing new talent for EVs is an imperative across the region. The joint efforts of the three partners to develop the semiconductor workforce in North America offers a relevant model that can be applied to EVs, tapping into existing – and creating new – industry and academic partnerships.

- Develop a comprehensive blueprint that establishes a common approach with regard to China, and which takes into account implications for individual countries as well as the region. An overly narrow defensive focus based primarily on tariffs should be avoided as it risks reducing North American companies’ global competitiveness in the longer term and boxing the region out of the most important technology transition faced by the automotive industry since its creation.

The U.S, Mexico, and Canada must stay in the fast lane when it comes to the EV transition. There is too much at stake, and decisive action is needed to fully realize the potential of the investments made so far and ensure a place for North America in this competitive race.

Related viewpoint

-

Footnotes

- The LVC rule requires all vehicle manufacturers to use a certain amount (40% for passenger vehicles and 45% for light- and heavy-duty trucks) of content produced with high-wage labor (average greater than $16 per hour) for goods to receive preferential duty treatment.

- The Big Green Machine, a Wellesley College initiative that tracks investments in the North American clean energy supply chain with a focus on the solar, wind, battery, and electric vehicle industries.

- In 2023, Chinese companies accounted for over 80% of global shipments of key lithium-ion battery components, according to Yano Research Institute.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).