This viewpoint is part of Foresight Africa 2024.

In recent decades, the financing for development landscape has changed dramatically, with aid flows declining relative to investment and borrowing on capital markets. This makes the cost of borrowing critical. African countries face some of the highest borrowing costs in the world for sovereign debt, partly due to low credit ratings. Only two African economies are currently rated at investment-grade levels, implying high interest rates and low borrowing volumes for the continent.

In contrast with previous analysis of the reasons for low credit ratings for Africa, a recent UNDP report focuses on the lack of sufficient hard data on African economies and the resulting subjective components included by global rating agencies in assessing the risk of lending to Africa. Compared to credit-scores based solely on macroeconomic and financial indicators, ratings by agencies sometimes overrate, sometimes underrate, and often contradict each other for the same country. In many cases, the ratings analysts of global agencies do not even visit the country in question.

This means that, even without any systemic bias, the sovereign credit ratings of African countries often deviate from what the (limited) data would otherwise suggest. The UNDP analysis quantifies both the financial and development costs of such credit-ratings idiosyncrasies, which reduces the resources available to achieve the Sustainable Development Goals (SDGs).

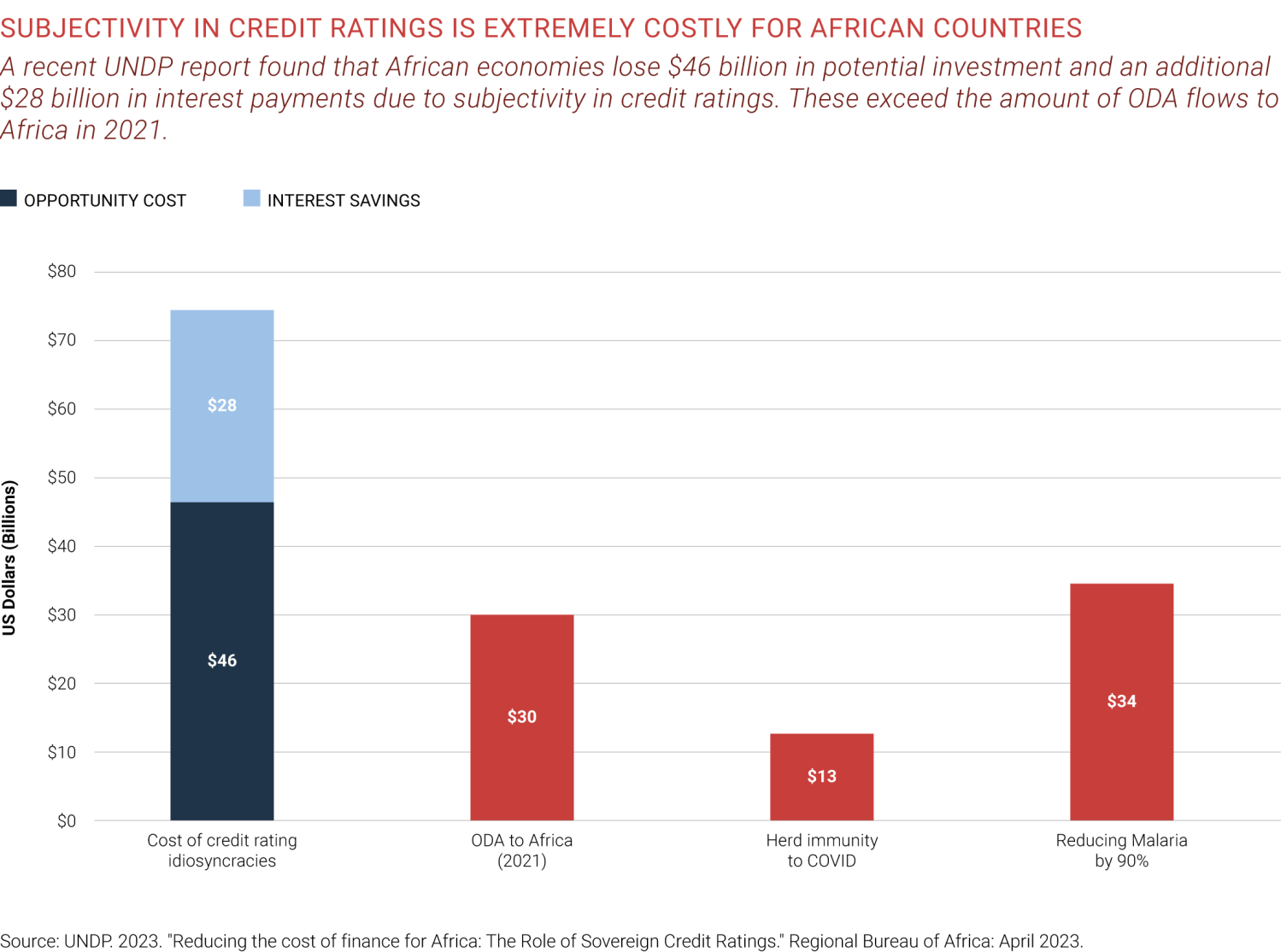

In purely monetary terms, subjectivity in credit ratings costs African countries (for which data was available) over $24 billion in excess interest and more than $46 billion in forgone lending, 20 over the life of various bonds (in both domestic and foreign currencies). This estimate of $75 billion loss is greater than the entire Official Development Assistance (ODA) to Africa in 2021 ($30 billion), more than twice the cost of reducing malaria by 90% (US$34 billion), and six times greater than the cost of vaccinating 70% of Africans (US$12.5 billion) to achieve herd immunity to COVID-19.

Subjectivity in credit ratings costs African countries ... over $24 billion in excess interest and more than $46 billion in forgone lending.

Reducing the cost of borrowing for Africa

What can be done to reduce the subjectivity of Africa’s credit ratings, and thus reduce its borrowing cost and increase the funds available for its development?

On the part of global credit agencies, there is a need for more transparency regarding their ratings process and what portion of it is subjective. UNDP, Brookings Institution, Africatalyst, and the African Union’s African Peer Review Mechanism (APRM) can open a conversation with the three leading agencies on this, as well as on the need for them to take a closer look at African countries, with more in-country presence.

In this context, several African credit rating agencies already operate on the continent and need to be involved in this conversation given their greater familiarity with the regional and country context of African economies and financial markets.

For African governments, there is a need to strengthen the amount and quality of data they submit to rating agencies, as well as their capacity to engage with these agencies more robustly. In response, a UNDP project was launched in the fourth quarter of 2023, which aims to deploy high-level experts and former ratings analysts to work with African government during the ratings process.

Authors

Related Content

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Making Africa’s credit ratings more objective

May 29, 2024